With FIRE in My Hands

Our family spent the dog days of COVID at home. No travels, no visitors, and zero breaks from each other.

By the end of 2020, we’d had it with school and working at home.

So we booked a beach house for Spring Break in the Outer Banks of North Carolina.

And to treat ourselves, we made it a two-week retreat — one for work and school and the other for leisure.

We splurged a little, renting a five-bedroom house, third door from the beach entrance in a quiet neighborhood.

I’m too cheap for the beachfront.

We had an unobstructed view of the ocean and a nature preserve from our deck.

The neighbors were all out of town.

I took the kids down to the beach the first morning. We were alone.

It was sunny, but only about 60 degrees outside. A stiff breeze pelted sand into our lower legs.

The water was rough and choppy — certainly not safe or warm enough for swimming.

But it was a perfect day for the kids to run through the ankle-high shore break, discover seashells, and make “snow angels” in the sand.

I watched the kids with joy and gratitude.

A song from the late 1990s came to mind, and I started singing aloud.

But how many corners do I have to turn?

How many times do I have to learn?

All the love I have is in my mind

Well, I’m a lucky man

With FIRE in my hands

I Know Just Where I Am

Last year around this time, my wife and I reached our financial independence number.

For personal finance enthusiasts, financial independence is the holy grail — the “FI” in FIRE and the essential step before retiring early (the “RE”).

I prefer the acronym F.I.B.E.R. which is hopefully more agreeable to FIRE critics and bathroom humor aficionados alike. But I don’t know a song about that.

FI is the point when your savings and investments are significant enough to cover annual expenses for the next 30+ years.

In other words, we’ve saved enough (within an acceptable margin of safety) to stop earning active income and live off savings and investments.

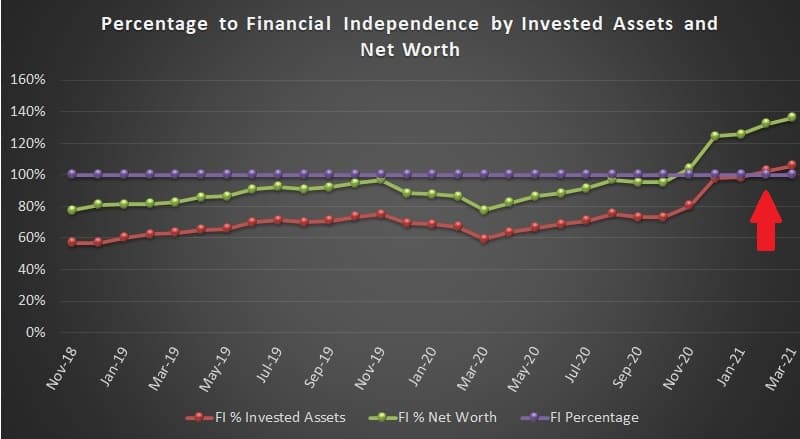

Here’s a chart I’ve been using to measure progress toward financial independence. The crossover point happened in February 2021.

The financial independence number is a generally accepted rule of thumb, not a mathematical certainty.

The financial independence number is a generally accepted rule of thumb, not a mathematical certainty.

It’s when invested assets (not including home equity or 529 savings, in our case) equals 25x annual spending.

For example, if someone spends $60,000 per year, their financial independence number is $1.5 million.

Some people hate the financial independence number, believing it’s not enough money to cover life’s future unknowns.

Others think the number is too conservative.

I care enough about the FI number that I measure it, but it’s not my gospel.

However, it is a significant spreadsheet milestone in route to a goal set in 2003, to retire at age 55, one year before my Dad retired from his teaching career.

More than that, I consider FI to be an enabler, giving me more options.

With FIRE in my hands, I can ease off the gas pedal and transition to a lifestyle with fewer constraints.

Happiness, More or Less

Yes, we hit our FI number last year.

But nothing changed.

I stayed at my day job, continued saving and investing, and I kept blogging.

There was no celebration or triumphant resignation letter.

I’m certainly not retiring any time soon.

The significance didn’t even hit me until that day on the beach.

That’s because I’ve seen wealth grow, only to be destroyed.

The 2000 dot com bust, the 2008 real estate bubble, the COVID plunge in 2020 — and the next one we don’t know yet.

I waited a year to mention it here because financial independence is fragile at first.

Sustained increased spending or a significant decrease in asset values can impact financial security down the line.

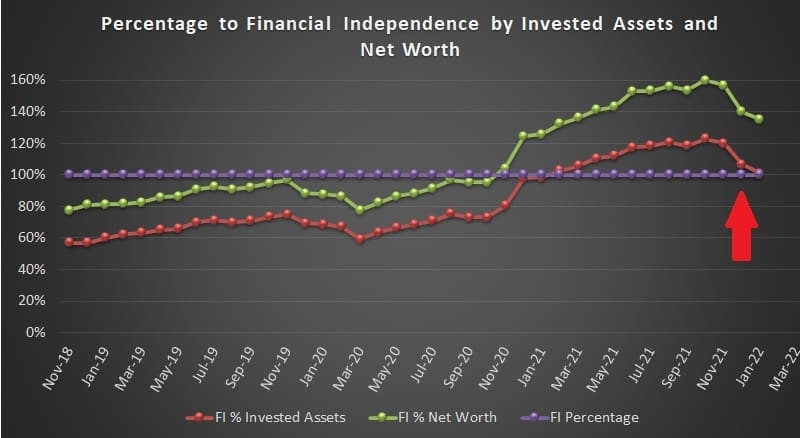

Just last month, we came close to losing our FI status.

Our wealth is closely tied to the stock markets. So when stocks fell in January, the chart lines went down.

Even more significant, we spent close to $10,000 more in 2021 than in 2020. That increase means we need more passive income and invested assets to stay financially independent.

I adjusted the annual spending amount in the chart at the end of December.

Here’s where we are today:

Moreover, I haven’t hit the point in life when I’ve acquired “enough” wealth. The ten-years-ago me would think our net worth is enough.

But today, it’s not — and I don’t know what is.

With inflation and so many unknowns expected in the coming decades, it’s best to keep earning.

However, our current wealth may be enough for me to shift priorities and earn differently.

Something In My Liberty

So what does this mean?

The financial independence number is only a rule of thumb.

Hitting FI doesn’t mean I’ve lost the desire to continue building wealth.

I’m not ready to flip a switch and start living off of dividends and savings. I want to fortify our financial footings.

We may choose to increase our annual spending. Or we may build extra wealth to travel more comfortably, anticipate medical issues, give to charities, or leave an inheritance to our children.

I like earning money and intend to continue to earn for years to come, maybe even past age 55.

But my primary income source may change.

Reaching financial independence brings clarity, confidence, and the potential to reclaim some of my time and pursue more meaningful work.

That’s my focus today — leveraging our financial independence to transition away from an unremarkable professional career toward something more rewarding and flexible. The transition has been on my mind for a while.

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services right now:

Sure Dividend — A reliable stock newsletter for DIY retirement investors. (review)

Fundrise — Simple real estate and venture capital investing for as little as $10. (review)

NewRetirement — Spreadsheets are insufficient. Get serious about planning for retirement. (review)

M1 Finance — A top online broker for long-term investors and dividend reinvestment. (review)

I love reading about your evolving understanding of FIRE. I resonate with your thinking. We are clearly coast FI, but love our jobs. We take a great deal of time off (about 5 weeks a year) and don’t work every other Friday. Our current status also allows us to be much more charitable to others. It’s a good life and one we are proud to have built. Keep up the good work. Enjoy these articles.

Thanks. Over the years, I think I’ve made it clear that I’ve never loved my job or career. There are highs and lows, for sure. Certain aspects I do like about my career right now. But it’s become clear that I shouldn’t be doing something I don’t enjoy so many hours every week. And now that our financial security is pretty well in place, I’m more comfortable making the leap.

Kudos on the milestone and on keeping such a nice spreadsheet! Mine needs some work. 33x annual spending is more of a target for me…but even then, i suspect like you…once I get there…it won’t feel like enough. Transitioning towards lifestyle improvements/enjoying your wealth seems appropriate. I’ve spent a little more freely on photography hobby gear lately, not because I have more time, but because it gives me great joy and will be around for quite a while once I do have the time to enjoy the hobby more fully….but didn’t get the beachfront latest and greatest…aiming for the value gear from a few years ago. Keep up the great work enjoying your family and continuing to provide a stable future for you and them.

33x vs 35x vs 40x, yeah I’m not sure any of those will feel like “enough” either. That’s why I’ve always focused on building income streams, to live off of dividends and interest and keep the principle for security. I’ve added online income to the mix from the work I do here, which can cover the gap between career departure and more formal retirement.

Smart to reconsider. If today is near the top, then it may feel very jolting as things continue to decline.

Your post does make me realize something though. When people say they have reached a Financial independence number, if they don’t change anything about their life, maybe the number isn’t very meaningful?

When I hit my number in 2012, I decided to take a leap of faith and leave finance behind for good. It was scary, but I figured what the heck. Can always go back to work if things don’t work out.

The reality is often less scary than the fear in our head.

Sam

Sam,

As I’ve been over the threshold for the past year, taking a ‘leap’ does seem less scary than it used to, even after my son’s diagnosis. It’s scarier to look five years ahead see myself in the same place I am today.

-RBD

Can you remind me how old you are and when you planned to retire?

I’m 46 today. 55 was the goal I set back in 2003. But lot has changed since then, especially my view of an ideal retirement. My Dad was my primary role model when it came to retirement. He stopped working at age 56 and hasn’t worked a day since. I expect I may continue to earn after 55 as long as I enjoy what I’m doing (e.g. writing, blogging). I don’t enjoy my IT career today. FI is a pathway out.

Gotcha. You have plenty of time! And your net worth could grow by another 50% in 9 years.

Can you clarify when you say: I enjoy what I’m doing, I don’t enjoy my career. Which is it? And what do you do?

Congrats on reaching FI !!!!

Is the 25x based on pre-tax or post-tax? I’m speaking primarily about Income Tax.

In your example of $60,000 per year x 25 years = $1.5 mil, I kept wondering if that really needs to be $80,000 x 25 years = $2.0 mil if the majority of a person’s retirement portfolio is sitting in a 401k account?

I’ve often wondered the same about several models out there on the internet. Heck even living in FL or TX vs CA or NJ could have a profound difference.

Thanks so much. I always enjoy your articles and appreciate your common sense approach and alternative thinking because it’s not just about investing, but as you often point out, it’s also about controlling your spending, understanding the pros and cons of life choices, as well as happiness too!

Yes, there are a lot of variables. That’s why it’s a rule of thumb and not a mathematical certainty. I don’t distinguish between taxable and tax-deferred in my charts. I suspect if you go back to the original Trinity Study or one of the many re-analyses done since then, you’d find an answer or more context. I recommend checking out the work done by Michael Kitces and Karsten at Early Retirement Now.

I too hit my FI Number around the same time as you. It was a day that I so look forward to, but there was no big party upon crossing that mark. I just had an internal light shine and moved on to the next thing.

It was a goal accomplished and one that I’m glad to have behind me, but my mind was focused on the next goal (i.e. how can I make my dollars work harder? or how can I increase the gap?) This makes me beg the question, How much is enough?

All good, thanks for sharing your thoughts!

Congrats on hitting your number, Cottonbelly. The work doesn’t end here 🙂

First of all, congrats and thanks for the link. 🙂

I think the FI number evolves as we get closer to that number and eventually hitting it. Also, many people realize that having a job that they enjoy ain’t so bad, so the RE part isn’t as important anymore.

Congratulations! My biggest concern is what to do when I reach FI. Heck, I may be there now. I think it is a moving number. I am not in a field that I could stop and then re-enter the work force if I started to eat into my principal. However, I also enjoy my job so my goal was never to retire early. I think the freedom to walk away from a career that is not fulfilling is the whole point of FI. I don’t want to regret not retiring earlier when I could have versus working longer for no other purpose but to “pad” my FI number.