Long-Term Investing in an Impatient World

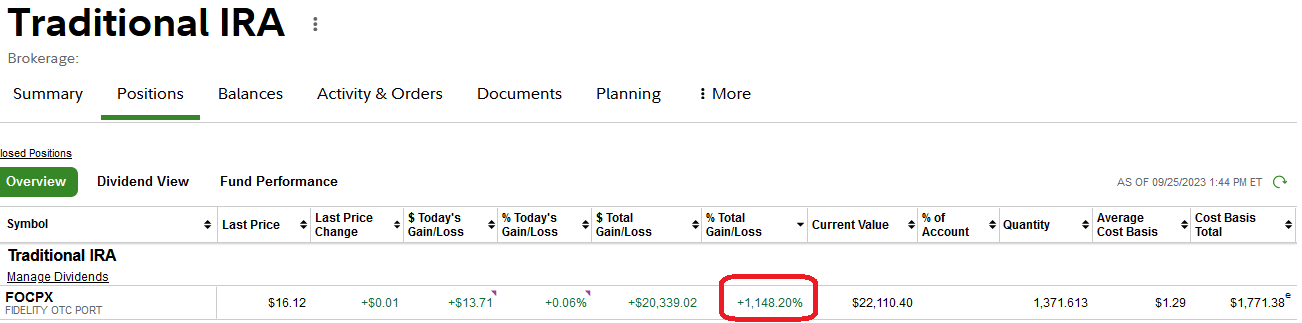

My best-performing investment ever is a managed mutual fund called the Fidelity OTC Portfolio (FOCPX). It’s up more than 1,100% since I’ve owned it.

My best-performing investment ever is a managed mutual fund called the Fidelity OTC Portfolio (FOCPX). It’s up more than 1,100% since I’ve owned it.

I wish I could say I’m brilliant at evaluating mutual fund managers and picking funds. But I only own this fund because my first employer, back in 1998, offered it as one of a few growth stock mutual funds in the 401(k) plan with Fidelity.

It’s been a successful investment for me because:

- I reinvested the dividends and capital gains for 25 years

- I never sold a penny, and

- luck would have it, it turned out to be an excellent fund

I rarely think about it.

Even with a hefty expense ratio of 0.81%, the Fidelity OTC Portfolio fund beat the S&P 500 over the past 25 years when accounting for reinvested dividends and capital gains.

Had I paid more attention to the fund fees over the past decade or two, I might have swapped it out for an index fund.

But back when I invested this money, I told myself I’d never touch it.

So I never did.

Table of Contents

Patience is our Superpower

Technology and modern living are making us more impatient. We expect next-day delivery, 5-second news briefs, commercial-free entertainment, and immediate responses when we write two-word messages to our friends.

Impatience is the opposite skill we need for investing.

The day-to-day stock market is unpredictable.

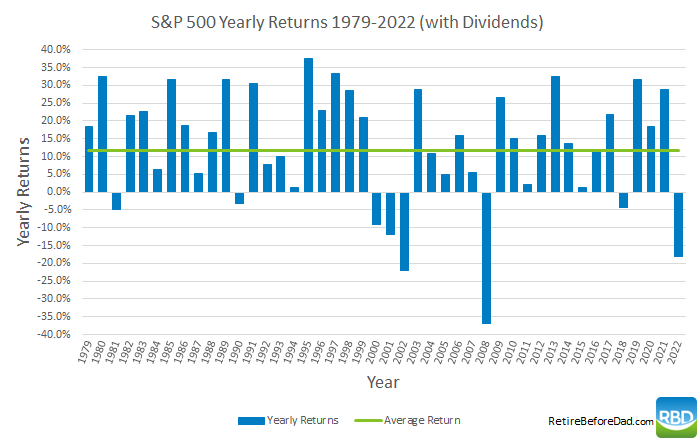

Year-to-year stock market returns fluctuate quite a lot, but they’re mostly positive. Here’s a look at the yearly S&P 500 returns since 1979.

Zoom out and look at longer-term averages; investors can match market returns by buying index funds and waiting.

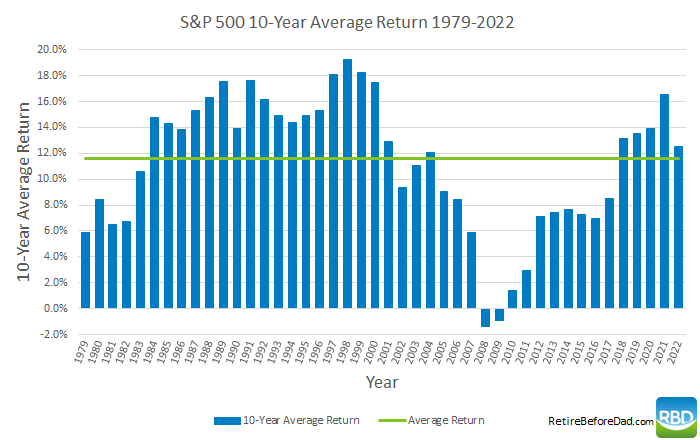

Here’s a look at the 10-year annualized average returns of the S&P 500 (e.g., the 2022 data point is the average return for 2013-2022).

Nearly every ten-year timeframe over the past 43 years has delivered positive returns to investors. The only exceptions being 2008 and 2009.

A few years later, returns moved back toward the long-term average (the green line is 11.56%, the S&P 500 average from 1979-2022).

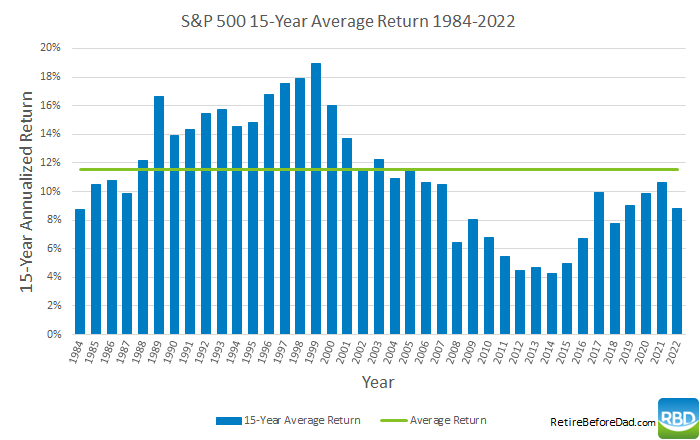

Zoom out further to 15 years, and the negative results go away.

As our investment time horizon increases, returns approach long-term averages.

Long-term stock market risk is minimal. Patience is the DIY investor’s superpower.

How to be a More Patient Investor

Since patience is our superpower, how do we invest more patiently?

Investing was a daydream paradise during most of my 20-year career.

I wasn’t all that passionate about my IT job, so during breaks, I’d escape to business radio, elaborate spreadsheets, and Yahoo Finance to monitor my investments.

The time I put into stock research and money management was fun, and it filled a professional-ish fulfillment gap where my career fell short.

But, immersing myself in business radio and stock research made me more susceptible to knee-jerk decisions and frequent and unnecessary money moves.

I thought more about investing day-to-day instead of year-to-year or decade-to-decade.

Now that I’ve left my previous career, I’m not looking for an escape and think much less frequently about my investment portfolio.

I’ve had many investment successes and failures. But the most successful investments are the ones for which I did the least and was the most patient. The biggest mistakes were my lack of patience (selling winning stocks too early).

Here are some ways to be a more patient investor.

1. Double-Down on your Career

I admire people who love their corporate or professional careers. Focusing 100% on a career is a more powerful wealth-building tool than investing, especially for younger workers.

Our ability to create personal wealth is less about portfolio fine-tuning and more about how good we are at earning and saving money.

Most DIY investors don’t need to overthink investing.

Choose a simple baseline retirement portfolio of index funds or ETFs, then supplement it with alternatives, income-producing assets, and a small percentage of speculative investments if you’re adventurous.

Do overthink earning.

Part of why my career was rather unremarkable was that any surplus brainpower at the end of the day went toward investing (and eventually blogging). Had I found a more compelling profession early on, I might have been more engaged, leading to a higher income.

Work harder, earn more, and invest the proceeds in hands-free investments.

2. Buy Illiquid Assets

Stocks — and commission-free trades at our fingertips — are the perfect liquid investments to screw up by micromanaging.

One way to avoid the temptation of frequent buying and selling is to own illiquid assets.

Rental real estate properties can earn similar returns than stocks and have more tax advantages. Managing a property requires different skill sets, but it can be outsourced.

If you’re not the landlording type, platforms like Fundrise and Arrived Homes let us own real estate without borrowing money and buying properties ourselves. These services and other crowdfunding platforms discourage liquidity and encourage long-term investment horizons to maximize real estate investment returns.

Another illiquid asset newly available to non-accredited retail investors is venture capital. Venture capital investing requires a 5-to10-year investment horizon to fully benefit from the growth of early-stage startups.

More illiquid investments include fine art and other diversified alternatives.

3. Limit Your Social Media Vices

Scrolling through social media is a superficial way to consume information — just headlines, one-sentence quips, and 10-second video clips, feeding our impatience.

If we’re not careful, the habits we’ve formed consuming information on social media can spill over into our real-life behaviors, like investment decisions.

Twitter/X has been my weakness over the years. I crave it when I’m bored and before bed.

My X feed features a lot of commentary on investing. Anytime I’m on there, a single tweet can trigger a question about my investment portfolio or strategy.

Some content can be helpful and make me smarter. I’ll find news stories on X that I would have missed otherwise.

But social media content is increasingly dubious (often chosen by ‘the algorithms’).

To limit usage, I hide the app at the back of my phone and set a usage time limit.

I also subscribe to a local newspaper and weekly news magazine and place those apps prominently on my phone’s home screen. With the X app hidden, I more often choose long-form content.

Long-form content gives us the big picture versus somebody’s brief thoughts.

Social media is still evolving and provides some valid utility. But consume it for entertainment instead of investment advice.

4. Don’t Watch or Listen to Business News

I used to listen to CNBC on XM Radio as a software tester in the office five days a week (circa 2007-2013).

CNBC is like a subconscious voice telling us we should be more active with our money. But, much of the commentary is biased toward institutional and professional investors.

Guests provide actionable advice because they’d otherwise be boring to watch.

Investing tips from CNBC guests won’t make us rich. It’s entertainment.

I still have a weak spot for daily business news, but I consume articles online instead of the constant drone of radio or TV.

For audio entertainment, I choose long-form podcasts that dig deeper into global economics. I’m currently listening to the Catalyst podcast, which highlights technologies and startups working to solve complicated climate and global supply challenges.

5. Start a Business

Now that I’m self-employed, I spend less time on my investment portfolio.

Business ownership offers me greater fulfillment than W-2 employment. There are more ups and downs as a solopreneur, but the tradeoff is worth it.

Running a business trains your brain to think long-term because long-term investments pay the most significant dividends.

There’s often an overlap between my business (investing blogs) and the market’s daily moves. But running a business takes up most of the brainpower I used to reserve for stock research.

Now, the daily stock market moves distract me from writing, so I don’t pay attention like I used to.

Business ownership has the side benefit of upside earning potential, like doubling down on your career.

6. Buy Boring, Set, and Forget

More than 90% of my net worth is in traditional assets like stocks, bonds, cash, and home equity. I reserve less than 10% of my portfolio for alternative investments and speculation (e.g., real estate crowdfunding, venture capital, and IPOs).

But that 10% of assets takes up most of my investment research time. That partly stems from my general curiosity for alternative investments — which are also popular blog topics.

I still monitor the individual stocks in my portfolio and don’t regret buying them.

But I have a long-term outlook for the portfolio and rarely act upon it because of news or earnings reports.

Diversified boring investments like index funds and ETFs require occasional rebalancing. But otherwise, you can set and forget them.

Portfolio fluctuations become more tied to market fluctuations instead of specific investments. So you can relax knowing that long-term patience will eventually overpower day-to-day and year-to-year movements.

Boring investing is a more attractive value proposition for me these days as my kids take up more of my time. I’m also gradually becoming more conservative as I approach my 50s.

Conclusion

Investing is a passion and hobby for many of us. That can lead to over-analysis and frequent and unnecessary activity.

Youthful investors are particularly susceptible to overthinking investing because they are eager to earn returns today that ultimately take decades. In my youth, I believed that being more actively engaged in investing would accelerate returns.

Older and wiser investors eventually realize that doesn’t happen. Patience and time increase our returns, not activity.

The most efficient way to fuel the compounding effect is to earn more money from a career or business and keep investing new funds into boring investments.

The more boring the investments, the less likely we will act upon them, reducing opportunities to make mistakes.

Featured photo via DepositPhotos used under license.

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

- Dividend Kings — 50+ stocks that have increased dividends for 50+ years.

- Monthly Dividend Stocks — List of 70+ stocks that pay a dividend every month.

- Dividend Champions — 140+ stocks that have increased dividends for 25+ years.