Boldin Review: DIY Planning for Financial Confidence

Boldin is an online financial confidence and retirement planning tool. It’s the most comprehensive financial tool I’ve ever used — miles better than any elaborate spreadsheet. This Boldin review takes a deep dive into its capabilities.

Boldin is an online financial confidence and retirement planning tool. It’s the most comprehensive financial tool I’ve ever used — miles better than any elaborate spreadsheet. This Boldin review takes a deep dive into its capabilities.

I’ve been tinkering with Boldin since 2017, when I met the Founder, Stephen Chen, and explored the tool for some articles I was writing at the time.

I used the tool (and shared results) in August 2019 to help determine if I was on track to retire at 55.

It’s come a long way since then. Steve and the team have refined the user interface and visualizations to provide insight into users’ long-term financial picture.

Boldin was previous known as NewRetirement. The company rebranded to better reflect its capabilities to help everyone, not just retirees. It aims to help 100 million people improve their financial lives.

The PlannerPlus product takes it a big step beyond legacy tools, enabling more than 250 manual inputs and customizations to visualize the financial picture of the next 50 years of your life.

Boldin answers the questions:

- Can I retire yet?

- How much money do I need to retire?

- Will I run out of money in retirement?

- What will my net worth be when I’m 90?

- Will I run out of money if you buy a lake house?

- What are the tax implications of moving to Arizona?

- What happens to my retirement security if I change investment strategies or jobs?

Boldin helps to account for big expenses (e.g., college), changing healthcare and spending needs, and Social Security, among many other variables.

For example, you can add a $50,000 annual college expense from 2030-2034 and see that on a graph.

Users can adjust investment returns for rosy and not-so-rosy scenarios, plan for future real estate purchases, and run probability models on the viability of their retirement plan.

This Boldin review examines tool capabilities and includes screenshots and examples from my tinkering.

I’ll focus on the PlannerPlus tool, a subscription-based service that includes the full functionality of the calculator. This tool has so many nifty features I can’t possibly write about them all in this Boldin review. I’ll highlight what’s most valuable.

New users get a 14-day free trial of the complete PlannerPlus solution.

If you decide not to subscribe, users still get a ton of planning capacity and calculation for free. There’s also an advanced “Academy” program that includes classes and priority support.

Please note: I’ve recommended this tool for many years. RBD is an affiliate partner with Boldin. If a reader uses links on this page to sign up for a PlannerPlus subscription, RBD will be compensated.

Table of Contents

My Take

Boldin PlannerPlus is a premium, comprehensive web-based retirement calculator and DIY financial planning service.

The product provides deep insights into your finances, including long-term projections and what-if scenarios based on life events and decisions.

When I say comprehensive, I mean it. Boldin is an over-the-top complete financial planning tool. No spreadsheet can compare.

The tool can import data from your financial accounts and takes around 250 manual inputs to customize your plan.

It offers several charts and visualizations that update when you tweak your plan.

If you’re someone who creates elaborate spreadsheets to customize your retirement plan, this product is far superior.

I suspect this software is on par or better with the software used by financial advisors. This user-friendly tool allows DIY financial aficionados to achieve similar results as financial planners.

The annual price point ($144) is well below what a financial planner would charge, and the person inputting the data cares best about the outcome.

Nobody cares about your financial future more than you. If you’re apprehensive about financial planners but still want a complete picture of the future, Boldin may be for you.

Please note: All screenshots in this Boldin review are taken from a dummy account for illustrative purposes.

Who is PlannerPlus For?

Boldin PlannerPlus is for DIY financial planners — people with moderately complicated to complex financial situations who do not want to pay for a financial advisor.

Spreadsheet wizards who are overdue for an upgrade will also benefit.

It also caters to people who like automation and continuous monitoring. Once you link to your bank and financial accounts, the tool updates data daily, always giving you the freshest data possible.

And for planner personalities who want to understand their options and how various scenarios will play out.

From their website:

Boldin is for people who want clarity about their choices today and their financial security tomorrow. Boldin is a financial planning platform that gives people the ability to discover, design, and manage personalized paths to a secure future.

Video Review

You can view my 35-minute video Boldin review and tutorial on YouTube or below.

Overview

New users will be prompted to input data and connect accounts to build your baseline scenario. Set aside 30-45 minutes to get your foundational information into the system.

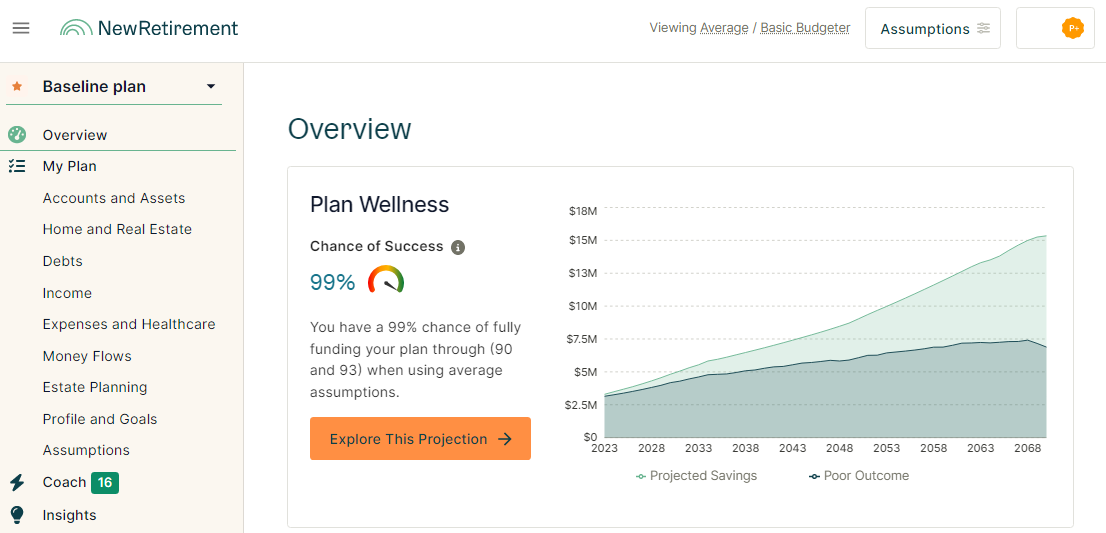

As you input data, you’ll get updated charts and visualizations. Once complete, the main picture of your long-term plan is the Overview section.

The Overview is a home base.

The left side shows which plan you’re working on. It defaults to the Baseline plan. But you can also add different scenarios.

The right side is the Overview Plan Wellness view.

The Overview updates as you input data. But consider it one of the finished products. It informs users of the retirement plan’s feasibility based on hundreds of data points and assumptions.

There is also an income and expenses view, a real-time net worth view, and a net worth projection.

The Plan Wellness changes quite dramatically with minor tweaks. The view above is a particularly rosy picture, showing this account has a likely outcome of a $15 million net worth upon death in 2070.

Though I’m sharing the happy view, various optimistic and pessimistic settings and assumptions will show great wealth or tragic bankruptcy based on minor changes.

That’s because when you plan out 40 years or so, income and investment return variation, compound interest, inflation, and other macro assumptions skew the math.

The more accurate and realistic you make your inputs, the more helpful the plan.

Much refinement and tinkering are necessary to get to a “final product”. But the final product changes as the market and situations change.

Boldin is your long-term comprehensive financial planning sidekick.

Inputs

Next, we’ll look at the inputs one section at a time. Users input data or connect accounts (via Plaid) until all financial data is entered.

The software uses the data to visualize your financial future (see Outputs).

Here’s a closer look at the left side.

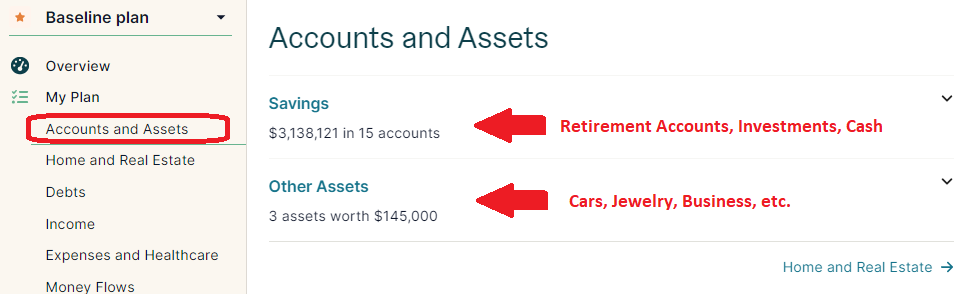

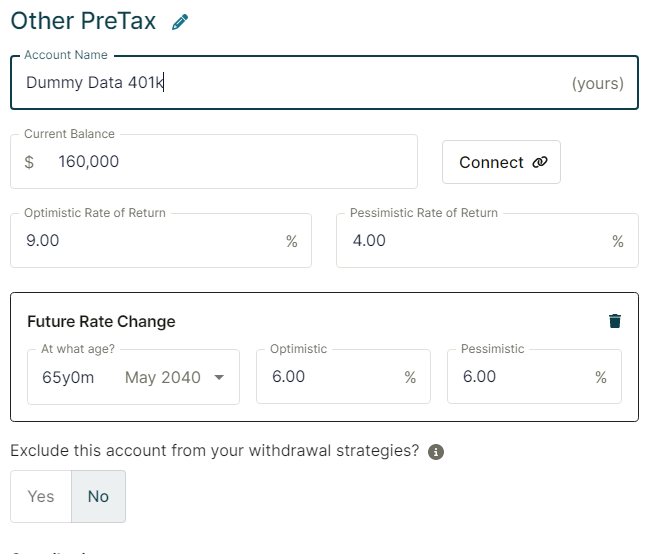

Accounts and Assets

This is where you connect most of your financial accounts, including retirement, banking, college savings, HSAs, and crowdfunding. Plus, you can add the value of real assets such as cars, jewelry, or the estimated value of a business.

Each account has an optimistic and pessimistic rate of return setting. I used 9% for optimistic conditions and 4% for pessimistic conditions throughout. You can also change the rate of return estimates after a certain age. I’ve reduced investment returns after age 65 for this example.

The software uses these numbers to calculate different scenarios.

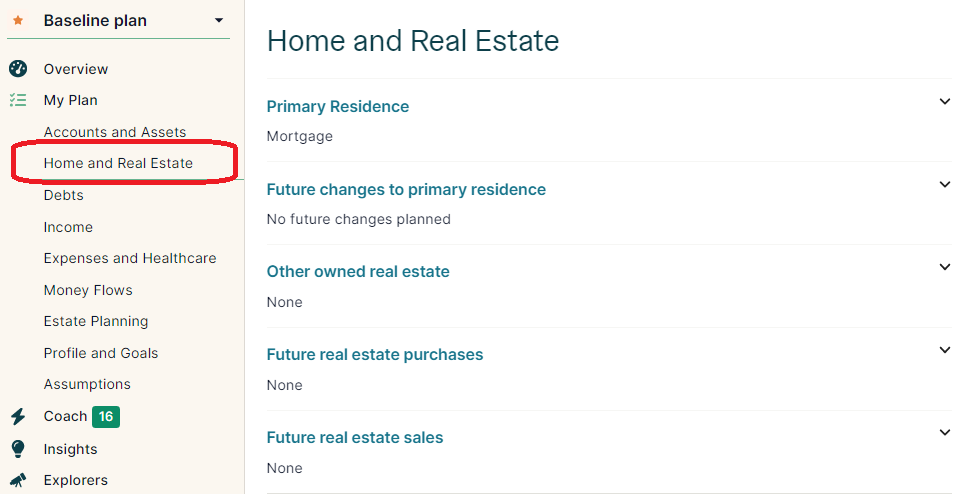

Home and Real Estate

The Home and Real Estate section lets you enter your primary home, including the estimated value, mortgage rate, balance, and payment amount. It estimates your payoff date and factors that into future cash flows.

It also provides options for future changes to your property if you plan to remodel, sell, refinance, or do a reverse mortgage.

There’s a place for other properties and future real estate purchases.

This flexibility gives you options to plan future investments or vacation homes.

Debts

The Debts sections provide a simple input for non-mortgage debt, including credit cards, cars, college, and medical debt. It enables connectivity to debt accounts.

For example, you can import data from your credit card accounts.

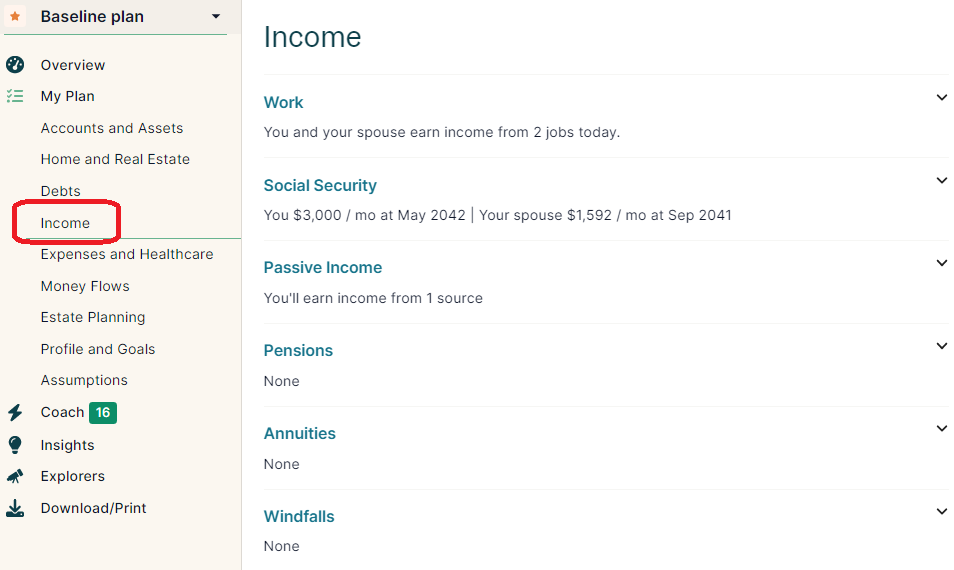

Income

The Income section provides inputs for whatever income you currently receive, expect to receive, and timeline and growth options.

For example, if you make $80,000 today and expect to get 5% increases until 2030 when you retire, it will factor that into your plan.

The tool provides inputs for Social Security (and a link to find what you’ll earn), passive income, pensions, annuities, and windfalls (e.g., inheritance).

You have a choice between manual entry or a connected account. This is where the tool connects to your accounts through Plaid APIs. Most modern fintech companies use Plaid to make it easy to connect your bank accounts to view data.

These are one-way connections, so Boldin can’t change anything in your accounts.

It’s convenient. Connect once, and the system monitors and updates the data onward. So your plan is always up to date. These kinds of connections can have issues. The more frequently you log in, the better. You may need to occasionally reconnect.

Manual entry works, too, if you don’t like or trust API connectivity. But you’ll need to change the input data frequently to maintain accuracy.

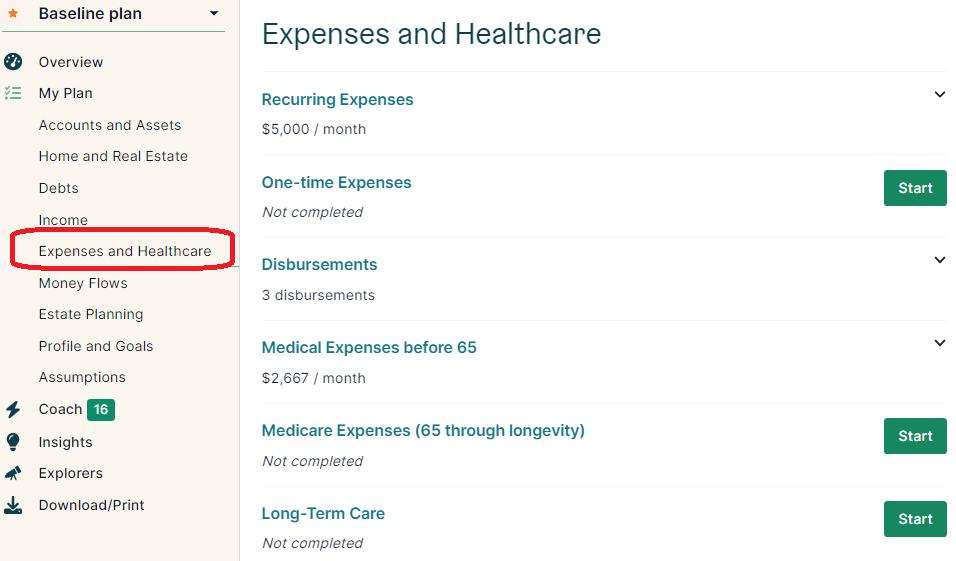

Expenses and Healthcare

After income, there’s a detailed input section for expenses, including basic living, one-expenses, disbursements (e.g., college expenses), and specific medical expenses.

I found it helpful to separate each expense. For example, I could separate a mortgage payment from general expenditures. By connecting the mortgage, the system factors in the change in cash flow after it is paid off.

Then you can model a spending amount for a few years, then increase or decrease for another period.

So you could say you expect to spend $6,000 per month from age 60 to 65 and $7,000 from age 66 to 70.

When you get to longer-term projections, you must start guessing about medical expenses past 65. The younger you are, the more difficult this becomes. It’s wise to overestimate.

Money Flows

The Money Flows section lets you detail where to direct your money. For example, if you want to move $1,000 per month from cash to an investment account, you indicate that here.

It’s also where you declare a withdrawal strategy, evoking the 4% rule or another withdrawal strategy. You can direct “excess income” and start down the road of Roth conversions (note: Boldin has a robust Roth conversion explorer for estimating the benefits of such financial maneuvers).

The tool automatically factors in minimum required distributions (RMDs) based on current laws.

Outputs

Boldin takes all 250+ inputs and models a long-term outlook for your money using easy-to-interpret visualizations.

The output visualizations update automatically when your connected accounts update or you tweak data. Outputs show on the same screen on the right side. The screen captures below are on the right screen side.

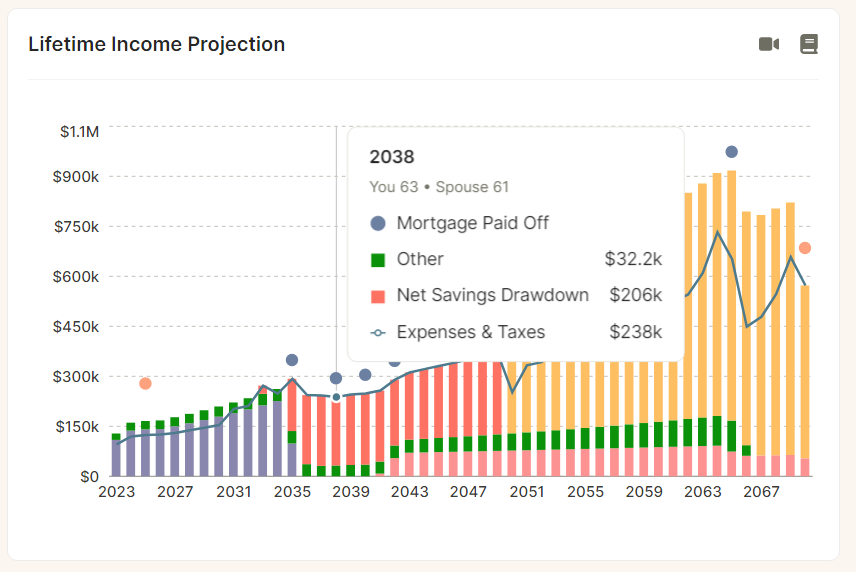

Lifetime Income Projection

The first and primary output is the Lifetime Income Projection chart.

- Bars represent income streams

- Dots represent key milestones in your plan

- The blue line represents projected expenses

Hover over a column or dot to get details.

This chart helps to determine if you’ll have enough income and asset availability to cover expenses until your “longevity age” (estimated death date).

In the example below, work (purple) and passive income (green) combine to cover expenses until about 2030, when asset drawdowns kick in (pinkish orange). I’ve highlighted the dot at 2038, a key milestone for mortgage payoff.

Asset drawdowns (or “Net Savings Drawdown”) take over until Social Security kicks in (pink). Eventually, minimum required distributions (yellow) gives the retiree an income surplus until longevity age.

Remember, this model goes out 50 years, so the actual results would obviously vary from this example. It’s a snapshot from today forward based on assumptions and the current numbers, making it an effective planning tool.

The graphic changes as the user tweaks the assumptions, income, or expected expenses.

Here’s a video from Boldin explaining the Lifetime Income Projection chart:

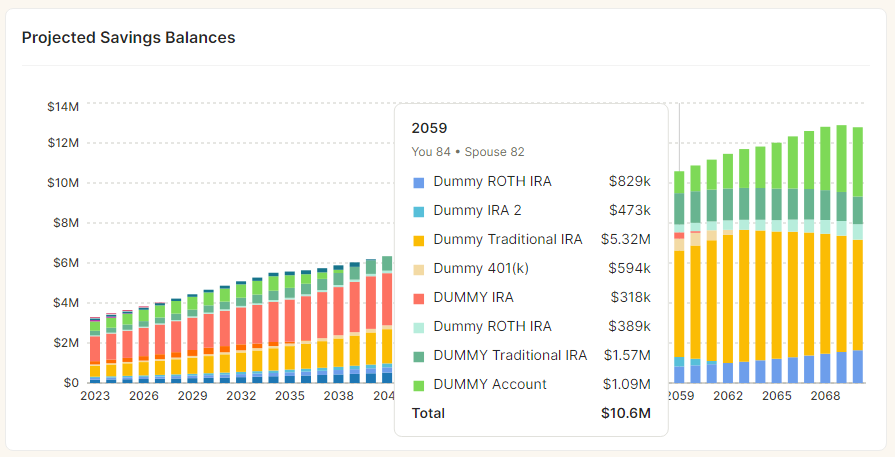

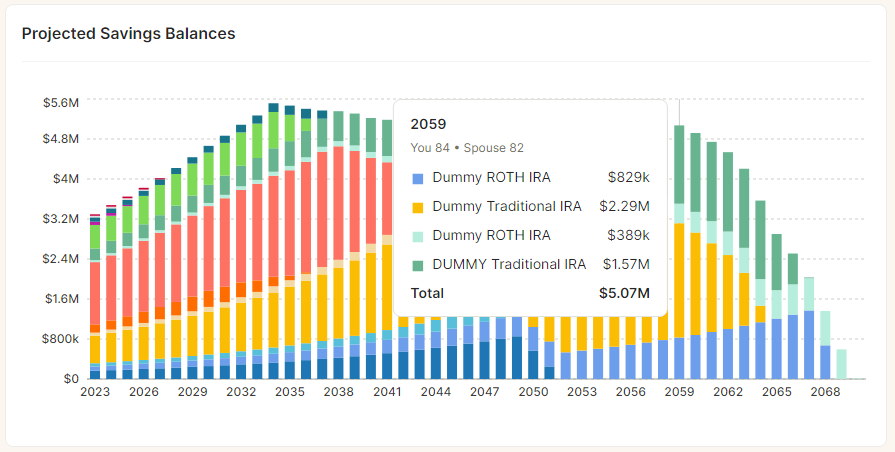

Projected Savings Balances

The next output is the Projected Savings Balances. This chart shows the estimated value of each individual account at every age.

The example below is based on a fixed spending assumption. But you can change assumptions to say “max spending” and get another view where the plan runs out of money.

In this example, the couple has total invested assets of about $10.6 million in 2059. Their spending surplus allows their next egg to grow and leave a financial legacy.

The software automatically optimizes the drawn-down strategy based on inputs and types of accounts. It draws down smaller taxable accounts and lets the tax-advantaged retirement accounts grow.

The next view uses the same input data but increases the spending assumptions to model the happy couple living it up a bit more. By longevity age, they’ve officially died broke!

Taxes

There are a few views dedicated to taxes. The tool estimates lifelong federal and state taxes, breaking them out by income, capital gains, FICA, and amounts by different tax brackets.

Tax data is displayed on a similar chart as the one above.

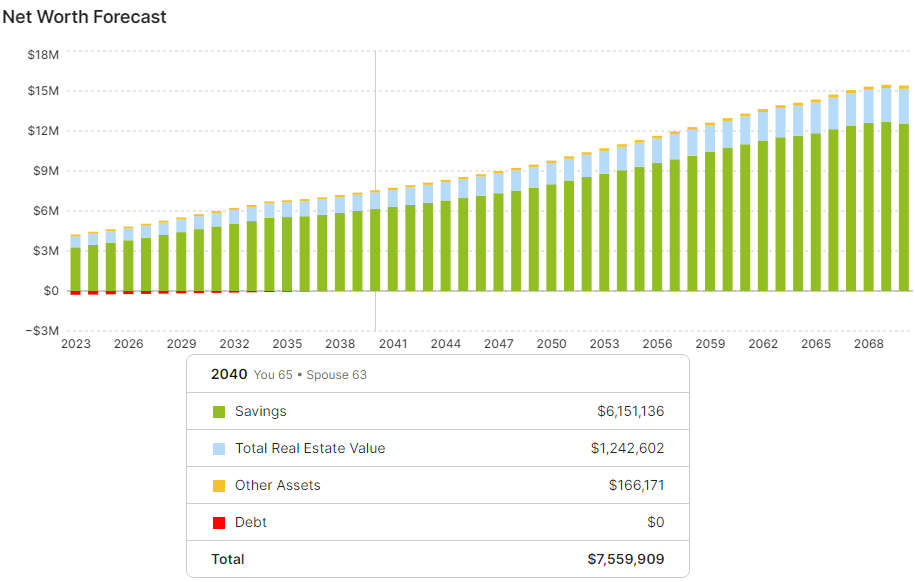

Net Worth Statement and Projected Net Worth

Connecting your various financial accounts to Boldin gives you a real-time view of your net worth every time you log in.

The net worth statement gives you a basic breakdown of your assets and debts on a line chart and with two donut/pie charts for assets and liabilities.

The projected net worth view is displayed in the overview section, but you can look deeper in the Insights section. The chart shows the estimated net worth every year between today and the longevity age. Highlight any year to get details.

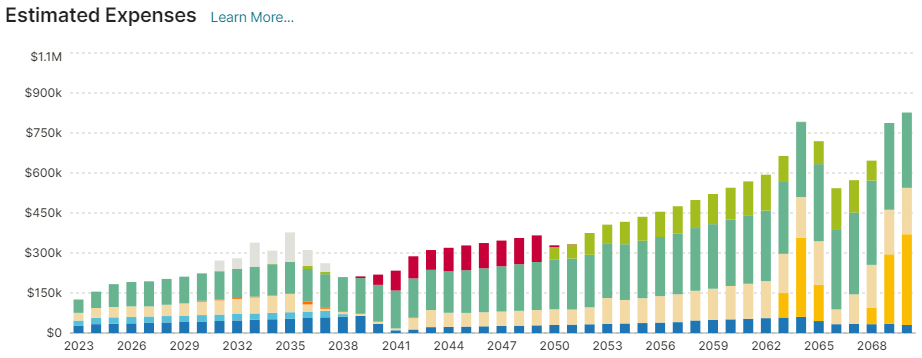

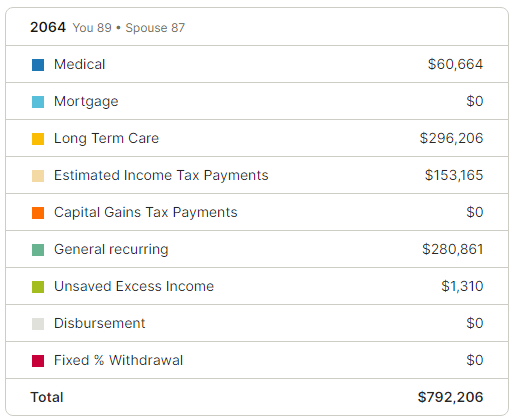

Estimated Expenses

Estimating expenses 30-50 years from now is nearly impossible. However, Boldin offers a framework to make estimates digestible for planning purposes.

The Estimated Expenses view takes inputs and places the anticipated expenses on a timeline, much like the income and savings views.

This feature would be beneficial for long-term care, healthcare, and debts. It automatically assumes health expenses will rise dramatically in the years before death.

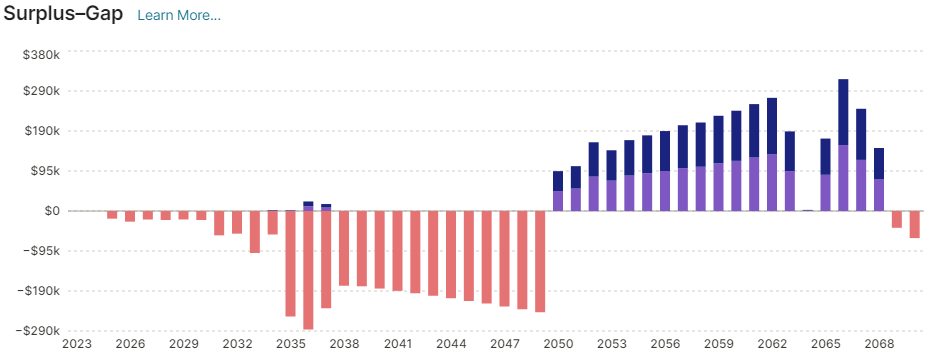

Surplus-Gap

This toll analyzes when surpluses (ability to add to savings) and gaps (times when you need savings to cover expenses) occur by year.

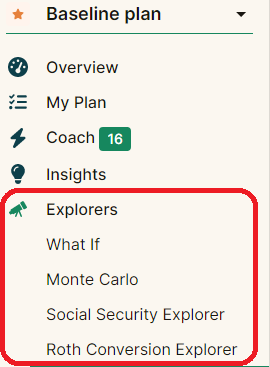

Explorers

The Explorers section empowers users to dive deeper into what is already created. Below is a brief overview of each.

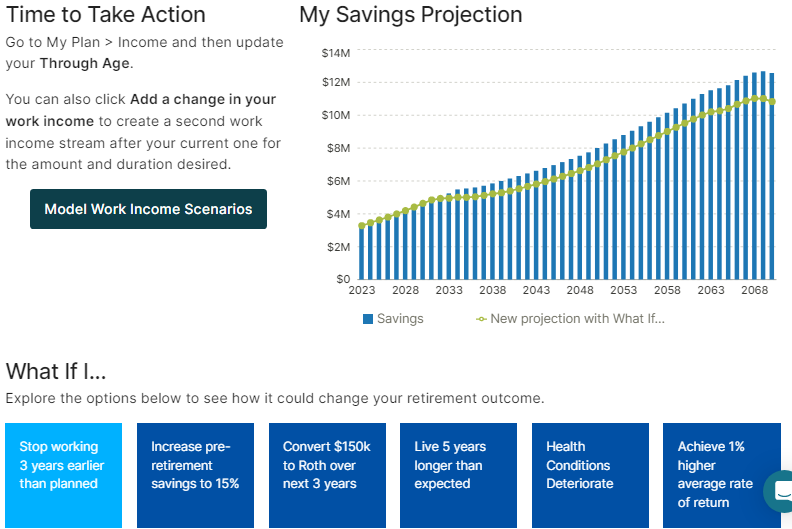

What If

What If

The What If explorer guides users through testing common “what-if” scenarios to see the impact on your savings over time. What if you work longer? What if you cut expenses? These options offer a few quick ways to see the impact.

I’ve moved up the planned retirement date by three years in this example. Click on a blue box to see the impact on savings, then take action or create a new scenario based on the refined assumptions.

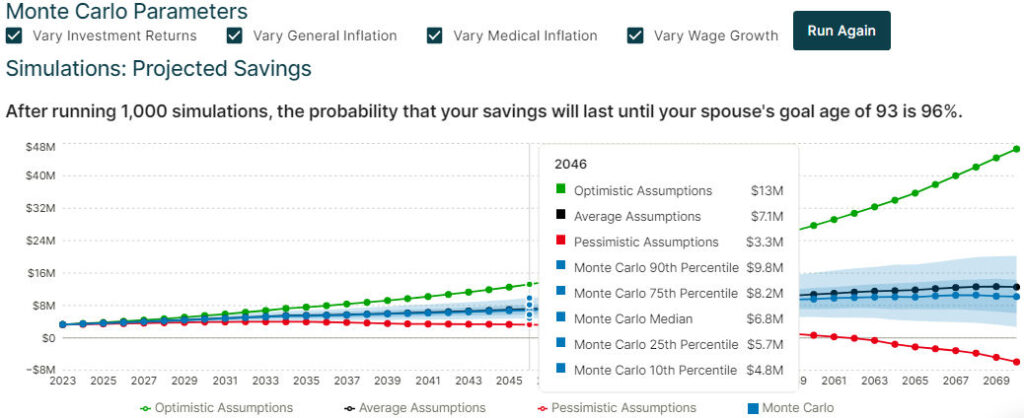

Monte Carlo Analysis

Monte Carlo simulations run thousands of scenarios using randomized and varying values to mimic market ups and downs based on historical data.

Boldin runs 1,000 scenarios to calculate the probability of savings lasting until the longevity age.

Social Security Explorer

The Social Security Explorer is a tool for looking at how to calculate and optimize a user’s Social Security income. If you don’t know your benefit amount, the tool sends you to the Social Security website to open an account to understand how much you will receive.

Input the Social Security data. Then the tool will model the Current Plan, Desired Plan, and Maximum Life Benefit in a chart.

The tool looks at your benefit and longevity to determine Maximum Life Benefit. The basic logic is if you expect to live longer, say into your 90s, it makes more sense to wait until age 70 to collect Social Security.

Social Security benefits decrease by about 8% every year beneficiaries claim before full retirement age and increase by about 8% every year beneficiaries delay. At 70, the benefit stops increasing.

Roth Conversion Explorer

Roth conversions are a tax strategy to convert pre-tax retirement contributions (into 401(k)s or traditional IRAs) into Roth IRAs.

Traditional IRA withdrawals are taxed, whereas Roth IRA withdrawals are tax-free.

The idea with a Roth conversion is you move money from pre-tax accounts into a Roth, incurring a tax liability sooner, thereby making withdrawals tax-free years down the line. Roth IRAs do not need required minimum distributions (RMDs) and can be passed tax-free to beneficiaries.

There are restrictions, primarily that you cannot withdraw the converted Roth IRA money for five years after the conversion. The strategy is to make the conversion while tax rates are low in anticipation that tax rates will be higher later on.

The Boldin Roth conversion calculator models this decision into charts and estimates how much users can potentially save.

PlannerPlus Academy

PlannerPlus Academy includes the full functionality of PlannerPlus, plus:

- Access to intro course on financial planning

- Access to 16+ in-depth classes, live and pre-recorded

- Live Q&A Sessions

- Priority product support

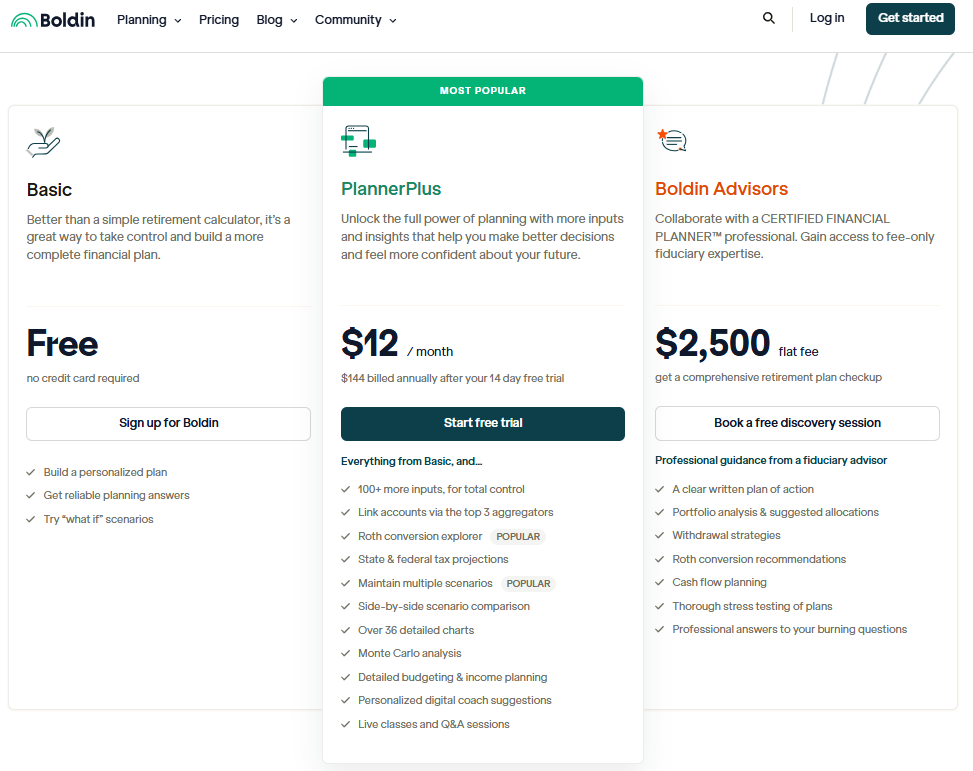

Pricing

Go to the pricing tab on the Boldin homepage to see what’s included in the free plan.

Note that pricing is subject to change. Click on the image below to be taken to the pricing page for the latest rates.

Boldin vs. ProjectionLab

ProjectionLab is a similar online DIY planning tool. I wrote a comprehensive ProjectionLab review and made a video comparing Bolding and ProjectionLab (watch below).

Overall, ProjectionLab has more of a freestyle feel to it, while Boldin is more linear, designing your plan from top to bottom.

People closer to retirement will prefer the mature tools and calculators that Boldin provides. Younger savers still in the wealth-building phase of life may prefer the sleek user experience and net worth tracking feature.

Here’s the comparison video:

Conclusion

Boldin is a robust and comprehensive tool. It can be complicated, but the user experience has improved over the past few years.

If you start a free trial, be prepared to spend at least an hour inputting your information and tinkering with the settings.

After the 14-day free trial, the tool’s functionality will decrease unless you pay for a PlannerPlus subscription.

If you’re serious about your planning and want to maintain the work you completed under the free trial, PlannerPlus is an outstanding value compared to hiring a financial planner. Those comfortable with DIY investing will be more than comfortable maintaining your plan.

Boldin is also helpful with big financial decisions, such as buying real estate, Roth conversions, and tax planning. Used effectively, the cost of the tool can easily pay for itself with savvy financial maneuvers.

That said, the tool is not for novices. There’s a learning curve, and the builders often change the user interface. So there may be some relearning from time to time.

But changes to the user interface have made the tool better over time, and leadership and developers at Boldin are constantly adding new functionality for a most comprehensive product.

Other tools are trying to catch up, such ProjectionLab, but there’s a long way to go.

The founder is still in charge, so we can expect continuous improvements. If the product were to be acquired, a la, Mint or Empower, I’d expect the improvements to wane.

Until then, Boldin is the gold standard in retirement calculators.

Boldin Review

-

Ease of Use - 9/10

9/10

-

Features - 9.5/10

9.5/10

-

Cost - 9/10

9/10

-

Value - 9.5/10

9.5/10

-

Mobile Experience - 9/10

9/10

-

Transparency - 10/10

10/10

Summary

Boldin is a comprehensive retirement and financial planning tool for DIY types. The ability to create complex plans makes the tool a bit overwhelming to start. But comfort comes about after a few minutes of tinkering. The user interface has changed several times over the years, and this could happen again, requiring users to relearn the user experience. This should not deter potential users, who would have the tools of a professional financial planner at their fingertips. Pricing is straightforward and reasonable, and the product offers excellent value compared to compiling data in a custom spreadsheet or hiring a financial advisor. Boldin is best experienced on a desktop computer. The bigger the screen, the better. But the mobile experience is surprisingly palatable and fully functional.

Disclosure: RBD is a long-term affiliate partner with NewRetirement and Boldin. RBD may receive a commission for readers who sign up for Boldin and subscribe to PlannerPlus. Content on RBD is free. Partnerships like this one help to support this website. RBD generally only reviews products and services that are recommended. The opinions expressed in this Boldin review are solely of the author.

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

- Dividend Kings — 50+ stocks that have increased dividends for 50+ years.

- Monthly Dividend Stocks — List of 70+ stocks that pay a dividend every month.

- Dividend Champions — 140+ stocks that have increased dividends for 25+ years.