The Noise We Don’t Ignore

Inflation is destroying wealth and making food so expensive.

Inflation is destroying wealth and making food so expensive.

The Fed keeps raising interest rates — how can the housing market survive it?

The 16th largest U.S. bank failed a few months back. Then the 14th largest bank failed!

The COVID-19 pandemic happened. That sucked. Now there’s a stupid war in Eastern Europe.

The stock market hates all of it.

Let’s not forget the crypto-crash and that Sam Bankman-Fried guy (aka Scam Bankrun-Fraud). And that other Sam guy and his A.I. robot are going to take away all of our jobs!

Now Congress is on the verge of defaulting on the national debt — again. YIKES!

We can’t catch a break.

Table of Contents

Short and Shallow

The way we consume information has changed over the past few decades. The evening news, newspapers, and magazines were our primary sources of information about the world around us.

But the evening news lost viewership to 24-hour cable news. As internet access expanded, we shifted to reading newspaper articles on our computers, hitting refresh every five minutes when bored at work.

Cable news stories became three-minute video clips on websites. Magazine articles became blog posts. Letters became emails. Phone calls became text messages.

Soon, social media became a competing news source. What our high school friends had for dinner became more interesting than the latest international conflict.

Social media moved to mobile devices when the iPhone arrived.

Blog posts became Facebook posts and tweet threads.

Reasonable-length videos became shorts, TikToks, and reels, of which we only watch the first five seconds.

A more significant portion of news and content we consume these days is shorter and shallower, swiftly swiping past headlines, silly memes, dancing cats, and dating prospects.

Remember when someone mentioned something, and you said, “Yeah, I heard about that. I saw the headline but didn’t read the article.”

The shallow consumption of so much information puts more negative news fresh in our minds. What we see lacks the context and critical thinking required to comprehend it.

We make critical decisions based on this shallow information.

The Availability Bias

A man recently committed a violent crime in the parking lot of a big box store near my home. A bystander shared a video of the ordeal online.

I talked about it with some neighbors, and everyone agreed we wouldn’t go to that store anymore — for now.

This week, we might be sensitive about going to that store because of the violent crime.

But when I need my Bran Buds in a few weeks, I’m not paying $7 per box at Safeway. I’m going to the place that sells it for $4, even after that atrocious crime happened in the parking lot.

Bad things always happen in our communities and in business news. We hear about them more now because our eyeballs collect such a wide net of information.

We make decisions based on this information because it’s at the tip of our brain, not because it’s logical.

Psychologists call this availability bias.

In psychology, the availability bias is the human tendency to rely on information that comes readily to mind when evaluating situations or making decisions.

Because of this bias, people believe that the readily available information is more representative of fact than is the case. The availability bias — also known as the availability heuristic — is just one of a number of cognitive biases that hamper critical thinking and, as a result, the validity of our decisions. Relying on this information helps people avoid laborious fact-checking and analysis, but it increases the likelihood that their decisions will be flawed.

Steven Pinker, author, cognitive psychologist, and Harvard professor, had this to say about availability bias:

Another quirk of human nature is called “the availability bias”: Our assessment of risk and danger is driven by available episodes from memory, not representative data. If you ask people if we are living in an increasingly dangerous or increasingly safe environment, they will think of the latest terrorist attack and conclude that life has been getting more dangerous — rather than going to FBI data on violent crime, which in fact, has shown a decline over 25 years.

Availability bias is particularly poisonous when it comes to investing.

Zoom Out

There was a time when I’d sit at my office desk and listen to CNBC on satellite radio all day long.

Not surprisingly, I bought and sold stocks a lot more back then.

I think a lot less about the stock market these days because as the duration of my investment horizon increases, so do my chances of success.

Conversely, short-term thinking increases the chances of mistakes.

By simply zooming out to view a longer timeline and avoiding noise in our investment decisions, we can mitigate the probability of lousy returns relative to the market.

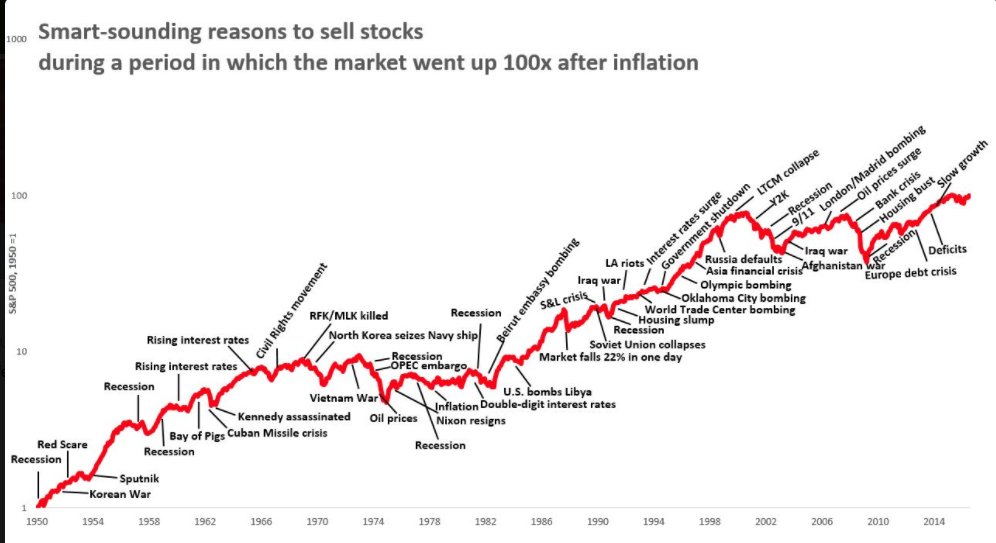

The U.S. stock market is a consistent performer over the long term, provided investors don’t try to time it.

There is always noise compelling investors to sell stocks. When your investment horizon is years, not weeks, the noise is irrelevant to investing.

Financial advisors might say to temporarily increase the ratio of bonds to stocks when the market shows signs of fragility.

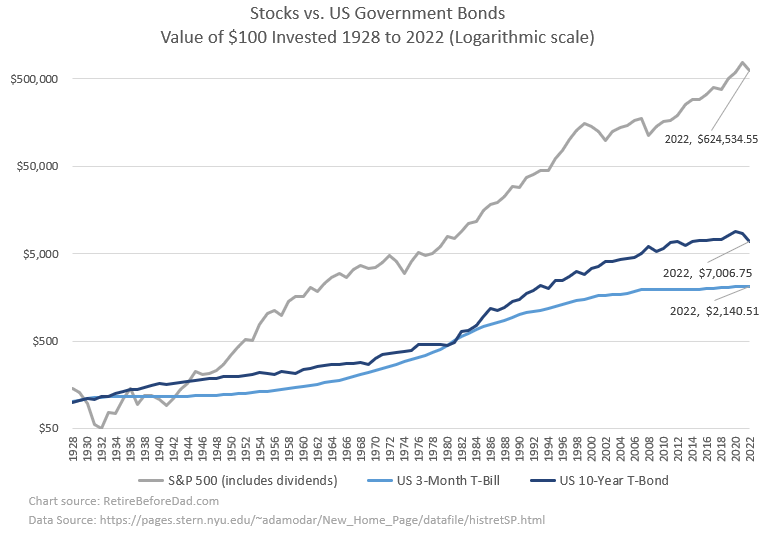

Despite the recent popularity of short-term Treasury yields, stocks still outperform government bonds over the long term.

So if your investment horizon is longer than five-to-seven years, there’s no need to make temporary adjustments. Keep your pre-determined stock-to-bond portfolio ratio and keep adding new funds.

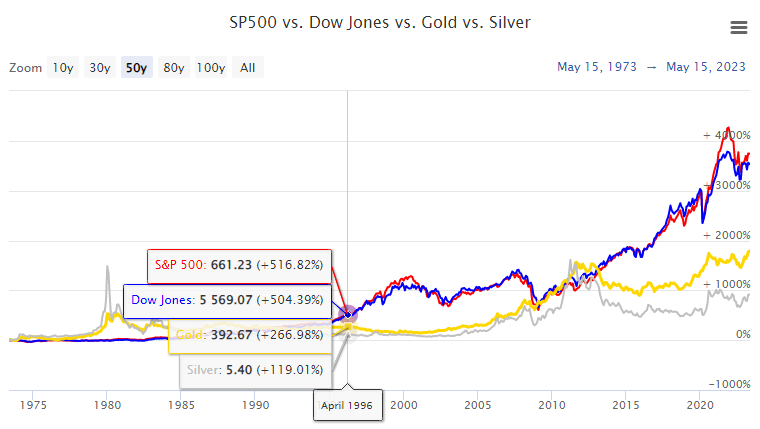

Contrary to what investing gurus and internet doomsayers contaminate your social media and online advertising feeds with, U.S. stocks outperform gold and silver.

Contrary to what investing gurus and internet doomsayers contaminate your social media and online advertising feeds with, U.S. stocks outperform gold and silver.

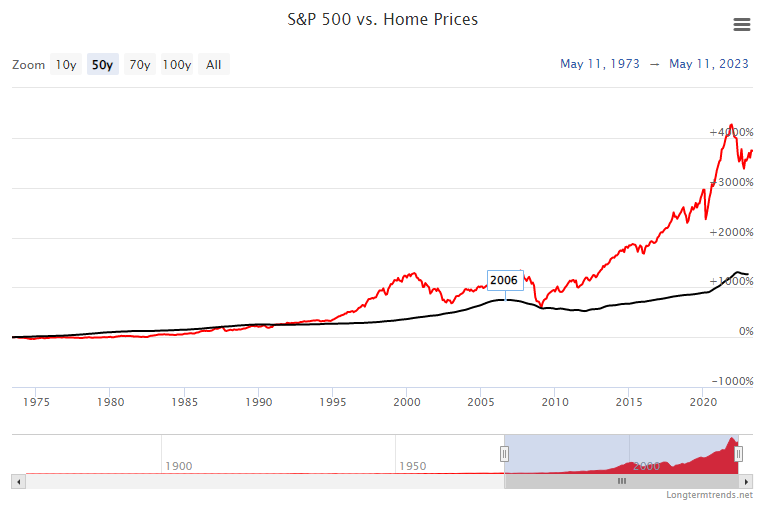

And even though housing has gotten so expensive everywhere, stocks still outperform the value of home prices.

The stock returns in these charts would have only been realized for individual investors if they owned a broad and diverse section of the stock market through the years and didn’t sell, regardless of the noise.

That means having the fortitude to hold stocks after the October 1987 crash, the dot-com boom and bust, the banking crisis of 2008-2009, and COVID 2020.

Big down periods are always followed by bigger up periods. If you aren’t holding stocks on those big up days, you’re missing out on the market returns.

Since the market is unpredictable, we cannot anticipate the big moves up or down. Successful market timing requires luck; eventually, we all run out of it.

Consistent investing throughout periods of fluctuation means buying at both the highs and the lows.

Dollar-cost averaging has us buying more shares when prices are relatively low and fewer shares when prices are relatively high.

Doing this over several years consistently is a widely accessible and reliable formula for building wealth.

Conclusion

The era of short and shallow information consumption isn’t reversing. Headlines and social media snippets dominate our attention, putting us at risk of decision distortion.

The tendency to rely on readily available information can lead us astray, as it often fails to represent the complete picture.

This bias can extend to our investment decisions, where short-term thinking increases the likelihood of mistakes.

We can avoid the noise by zooming out and investing with a long-term perspective. The consistent performance of the U.S. stock market over decades highlights the importance of holding onto investments and resisting the temptation to time the market.

Featured photo via DepositPhotos used under license.

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

- Dividend Kings — 50+ stocks that have increased dividends for 50+ years.

- Monthly Dividend Stocks — List of 70+ stocks that pay a dividend every month.

- Dividend Champions — 140+ stocks that have increased dividends for 25+ years.