I’m a 24-Year-Old YouTuber with 500,000 Followers — Here are 4 Reasons Why Young Investors are Struggling

I’m excited to present a guest post this week from a prolific YouTuber named Ryan Scribner.

I’m excited to present a guest post this week from a prolific YouTuber named Ryan Scribner.

Ryan talks about investing and personal finance on his YouTube channel, where he’s amassed a following of nearly 500,000 subscribers.

He also runs the blog Investing Simple where he shares reviews and investing tips for beginner investors.

When he reached out to do a guest post, I thought it would be interesting to learn about what’s on the minds of his audience. In particular, what’s troubling younger investors, many of whom feel they’ve missed out on the past decade of market gains.

Here’s what he has to say.

Back in 2016, I started my own YouTube channel. While most people saw YouTube as a place to share funny prank videos or vlog about their daily life, I had a different plan with my channel.

I decided to create a personal finance and investing channel, primarily geared towards millennials.

Over the last three years of running my channel, two years as a full-time gig, I’ve heard the same things over and over again.

The truth is, most young people are not participating in the stock market. Many of those participating find themselves struggling. There are common misconceptions about investing or barriers that I hear day in and day out from the young investors on my channel.

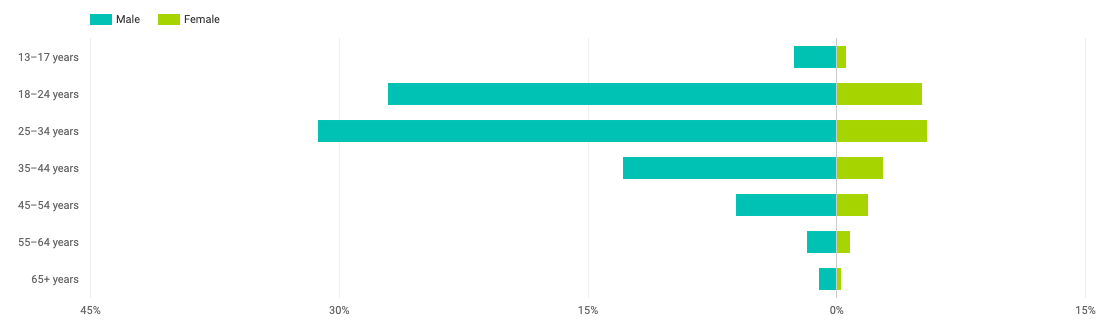

For context, my audience is primarily men (83%) age 25 to 34 living in the United States. The second largest group viewing my channel is US men age 18 to 24.

So, what are these young investors struggling with?

Table of Contents

1. Fear of getting SCAMMED

A lot of young investors are staying on the sidelines, and I believe this is primarily because of what the older generation experienced. A few years back, I was on a family vacation with an ex-girlfriend, and I was reading a copy of The Intelligent Investor by Benjamin Graham.

One of her uncles came up to me and asked what I was reading. When I told him about the book, he responded with, “don’t bother kid, the stock market is a total scam.”

Now you will always get the occasional naysayer that is totally against investing in the stock market. What’s interesting to me is that once I started my channel, I began seeing this comment pop up frequently.

The funny thing was, most of these comments on my channel were coming from young people. I remember thinking to myself, why do these young people believe investing is a scam? Where are they learning this?

Well, here’s the answer. I believe all of these young people have that uncle or parent in their life who is telling them the stock market is a scam, and that investing is a guaranteed way to lose money. The reason why these older influences think this is because of what they saw and experienced in 2008.

The stock market crash of 2008 was the second-worst financial crisis in history, and a lot of people lost massive amounts of wealth in this period.

Those who are financially savvy know the best thing to do during a crash is to stay the course. However, this is not common knowledge for the general public.

Many people, maybe including my ex’s uncle, decided to pull their money out of the market at the worst possible time. During a crash, people become so fearful of a more substantial potential loss that they would rather just pull their money out.

For the most part, the people who left their money alone fared well. Over time, the market corrected, and now they have grown their accounts massively. Unfortunately, the group who pulled their money out, or owned significant positions in companies that went bankrupt lost a lot.

From firsthand experience, I firmly believe the older generation is perpetuating the falsehood that the stock market is a scam. Unfortunately, a lot of young people believe it.

2. Analysis Paralysis

If you have never scrolled through the comment section of a YouTube video, you should do it sometime. It’s a blend between Reddit and a forum. Some have even referred to it as a “war zone.”

People often get very heated and opinionated in the comment section online, and I believe the main reason for this is because you are not the face behind the words.

This isn’t Facebook, where your name and face are attached to whatever you say. On YouTube, you can make up whatever name you want and use whatever picture you want. You’re totally anonymous.

I have been very public about the personal investments I have made on my channel, and I talk about both the wins and the losses. Without failure, every time I make videos talking about particular stocks or investments, I always get two types of comments from people.

The first goes something like this: “The stock market will crash in _____, I will invest after.”

The second goes something like this: “Don’t invest right now because _____ indicated the next recession is coming.”

Here’s a video I did on my channel specifically to address these comments:

People who say things like this are experiencing analysis paralysis. Back when I started this channel (in 2016), I was getting comments from people saying, “I’ll wait until the market crashes in 2017 to invest.”

Then, 2017 came around, and we had a roaring bull market. The same thing happened, I had hundreds of people saying they were waiting on the sidelines for the market to crash so they could invest.

Here we are in late 2019, going into 2020, and I am still seeing those same comments every single day.

The people who leave these comments have very detailed reasons for why they are sitting on the sidelines. They’ve studied different ratios and listened to the doomsday prophecies about the impending crash.

There will always be bull markets and bear markets, and sitting on the sidelines in an attempt to time the market is a losing strategy. The people who commented back in 2016 could still be sitting there in all cash for all I know!

3. Student Debt

One of the most common barriers to investing I hear from my audience is that they simply cannot afford to invest. Now, in some cases, it is because of the Starbucks coffee and avocado toast.

However, there have been numerous cases when I have talked to young people who are struggling to invest because they are burdened with student debt and underemployed.

College has become significantly more expensive over the last few decades. According to College Board, tuition plus fees at four-year public schools have increased 35% over the last decade.

The overall problem looks like this — rising tuition costs result in massive student loans. After these students graduate, many of them struggle to find employment or end up underemployed.

Between paying down student loans and not earning very much money, there is little to nothing left over to begin investing.

Now the good news is it’s easier than ever to begin investing. There are investing apps out there today specifically geared toward young people who are notoriously bad at saving and investing.

Take Acorns, for example. The online broker rounds up any purchases you’ve made on your credit or debit card and invests the spare change. This pain-free investing approach is very popular among young people.

I see a lot of videos and articles naming the spending habits of young people as the reason why they struggle financially. And while this is the case for some people, it isn’t for everyone.

I have heard from young people firsthand in the comments of my videos who don’t have any wiggle room left in their budget to begin investing. On the other side of the coin, I also see many comments from young people who are working skilled trades and maxing out their 401k’s.

I think the overall answer to this problem is to acknowledge that college isn’t what it used to be, and it may not necessarily be the best path for everyone out there.

As someone who was pressured to go to a four-year college by my parents and grandparents, I understand the frustration. I didn’t do what my family wanted me to do.

I ended up going to community college and getting an associate’s degree in electrical construction, which I used to get a job at the local power utility.

When I worked there, I was debt-free, making close to $70,000 per year at the age of 20. Because of my situation, I could participate in my 401k and invest excess cash flow surplus into the stock market.

4. Lack of Patience

The final struggle I see all the time stems from a lack of patience. I completely understand where young people are coming from with this because I experienced the same thing when I began investing.

Back when I got started, I decided that I was going to be a swing trader. I envisioned myself turning $1,000 into $1,000,000 in instead of waiting for index funds or blue-chip stocks.

I wanted to become a millionaire through trading.

So I spent months reading book after book on trading, studying candlestick patterns, and learning about different order types. When I finally began trading, I took $500 out of my savings and put it in my recently opened Scottrade account for trading.

Over the next few weeks, I attempted to swing trade.

What I found after doing this for a few weeks was that I was not predictably profitable. Sometimes I was right, and I would end up making 5 or 10% while other times I would cut losses and then stress out over getting back to break-even with my account.

Overall, I didn’t lose or make much of anything with my swing trading. I did, however, learn many valuable lessons.

For me, this is when it clicked for me that investing is a long-term game. Money is made more reliably through dividends and long-term asset appreciation, not trading patterns, and betting on earnings reports.

The funny thing is, almost all young investors go through a very similar experience. They are not interested in long-term investing at first because they are not patient enough. If you talk about 8% to 10% returns, you will put them to sleep.

They have the same mentality as I did early on, where they are looking to become the next millionaire by picking a hot penny stock or being an active trader.

I see comments like this all the time talking about crypto-currency, options trading, futures, and other speculative investment vehicles.

The truth is, these types of investments are far more seductive to young people.

On my channel, I’ve tried to take my own experience with swing trading and use it as a lesson to show young people. However, there are many lessons out there that need to be learned instead of taught.

I talk to young people every single day who tell me about how they lost a few hundred or even a few thousand dollars getting involved in some type of speculative investment.

The real struggle is getting young people to see the bigger picture and to understand the power of compound interest. But the unfortunate truth is that the next hot crypto-currency or IPO will always be more exciting than passive ETF investing in a Roth IRA.

Closing Thoughts

It’s easy to point fingers at young people and blame spending habits as the reason why we struggle with investing.

However, from what I have experienced firsthand and seen from my audience, I can tell you it goes a lot deeper than this.

Whether it is an irrational fear of the stock market instilled in us from the older generation, perpetually sitting on the sidelines, or something else entirely, these are real struggles young people face when it comes to investing.

The goal of my channel and blog is to get young people excited about investing and teach them the power of patient long-term investing. Hopefully, with ease of investing access and better education, more young people will start participating in the stock market at an earlier age.

Thanks to Ryan Scribner of Investing Simple for today’s guest post.

Photo via DepositPhotos used under license

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

- Dividend Kings — 50+ stocks that have increased dividends for 50+ years.

- Monthly Dividend Stocks — List of 70+ stocks that pay a dividend every month.

- Dividend Champions — 140+ stocks that have increased dividends for 25+ years.