Fidelity Roth Conversion: Why, and Step-by-Step Instructions

One of the advantages of reduced income due to leaving my full-time career is the opportunity to execute a Fidelity Roth conversion.

One of the advantages of reduced income due to leaving my full-time career is the opportunity to execute a Fidelity Roth conversion.

Roth conversions allow investors to transfer money from a 401(k), traditional IRA, or other tax-deferred retirement account into a Roth IRA account.

Traditional 401(k)s and IRAs let us invest pre-tax dollars into retirement accounts, reducing our current-year taxable income. The invested funds grow tax-deferred.

But when we eventually withdraw the money, we pay income tax on the withdrawals.

Roth IRA contributions do not reduce our taxable income, but contributions grow tax-free, and withdrawals are tax-free. Conversions let us get more money into the Roth for long-term growth.

Furthermore, required minimum distributions (RMDs) kick in at age 73 (now) or 75 (staring in 2033) for traditional retirement accounts, forcing us to withdraw money and create a taxable event.

Roth IRAs have no RMDs. This makes Roth IRAs useful long-term planning tools for DIY investors.

This month, I executed my first Fidelity Roth conversion to take advantage of the lower income and tax bracket.

I’ll share more details on why and how in today’s article.

Table of Contents

Why do a Roth Conversion?

I’ve invested money into traditional and Roth IRAs over the years for both me and Mrs. RBD.

Our traditional retirement accounts hold about 9 times the dollar amounts in our Roth accounts because we accumulated much of our assets in employer 401(k) plans and transferred them into IRAs.

The Roth accounts are far less bountiful. We contributed when eligible, but our income was too high for the past several years. Instead, we focused on contributing to traditional accounts to lower our taxable income.

Our active income has been much lower this year since leaving my career.

We still earn money from investment income, Mrs. RBD’s modest salary, and my online business, but we have significant deductions — especially COBRA health care premiums — that will lower our overall taxable income.

Therefore, this year is an opportunity to beef up my Roth IRA to set aside more assets for tax-free withdrawals decades from now.

Here’s what the IRS says about converting from any traditional IRA into a Roth IRA:

You can withdraw all or part of the assets from a traditional IRA and reinvest them (within 60 days) in a Roth IRA. The amount that you withdraw and timely contribute (convert) to the Roth IRA is called a “conversion contribution.” If properly (and timely) rolled over, the 10% additional tax on early distributions won’t apply. However, a part or all of the distribution from your traditional IRA may be included in gross income and subjected to ordinary income tax.

This transaction will increase our taxable income this year. We’ll receive a form 1099-R in the mail this tax season for the entire amount.

There’s no 10% penalty if we wait five years before withdrawing the money. That’s fine, as we don’t plan on touching this money for decades, and we have other cash sources if needed.

This move should save us tens of thousands over the next 20-30 years and give us more flexibility when we withdraw retirement funds later in life. It will reduce RMDs when they inevitably arrive.

Since this is my first Roth conversion and to avoid causing too large of a tax consequence, I’m converting just $15,000 this year.

Here Goes

Follow the screen captures below and/or watch the video.

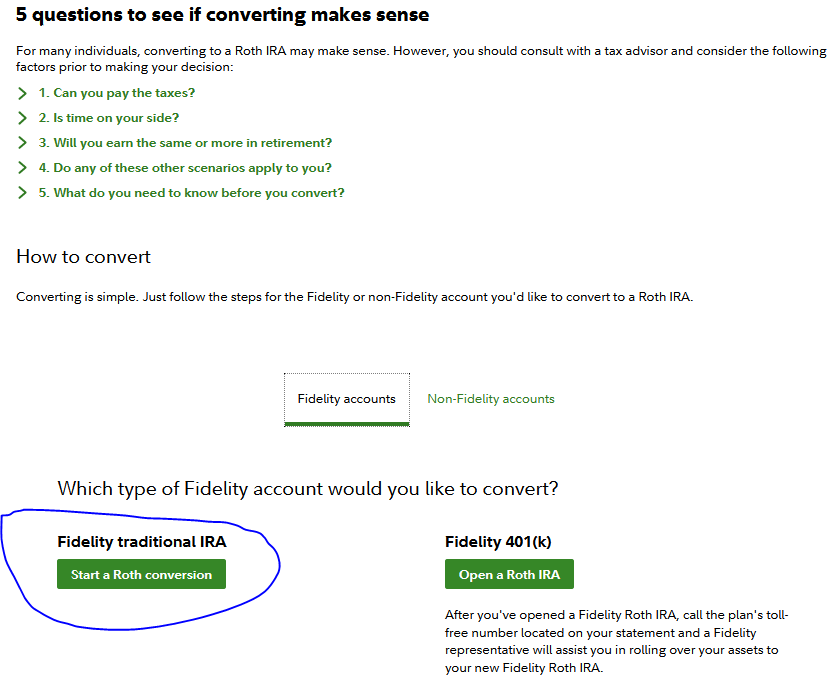

Fidelity has a dedicated page to help investors decide when to do a Fidelity Roth conversion.

This is a good place to initiate the conversion. You can also do it from the Transfers tab if you have a Fidelity account.

The process seemed straightforward since I already have Fidelity traditional and Roth IRAs, but I still called Fidelity to ensure I wasn’t missing anything. Fidelity customer support is always top-notch.

A representative confirmed how to do it online and said I’d automatically receive a tax Form 1099-R in late January or early February to show the distribution.

I’ll be required to file a Form 8606 with my tax return (only Part II).

Step 1: Initiate the Transfer

Get started by clicking the Start a Roth Conversion button (or use the Transfer tab in the menu).

Two important things to note:

- The Roth conversion deadline is December 31st (normal IRA and Roth contributions can be completed before April 15th, but this is a conversion).

- Conversion calculator — Fidelity has a useful conversion calculator to help you understand the tax consequences; Boldin has one that’s even better.

Once you’ve started the conversion process, Fidelity takes you through a clean set of steps to complete the transfer.

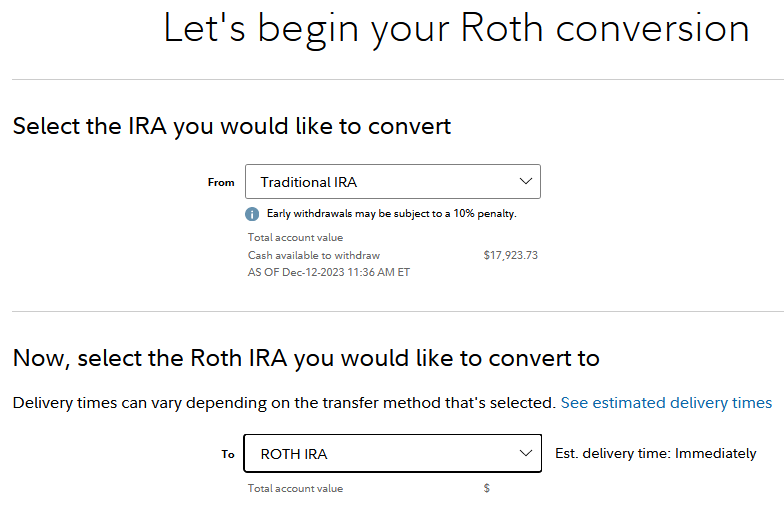

Step 2: Select Accounts

I have six accounts at Fidelity. So, the first step is to select the traditional IRA and Roth IRA I’m transferring from and to.

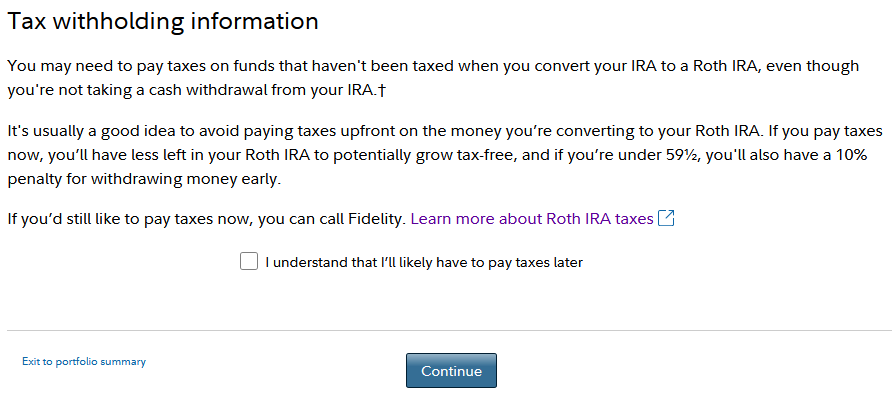

Step 3: Acknowledge Tax Implications

The next step is to acknowledge the tax implications. I’ll pay taxes out of pocket on the conversion amount on my 2023 tax return.

Fidelity gives you the option to have money withheld from the conversion, but that would reduce the amount that stays in the Roth account, and it is not recommended.

My combined Federal and State effective tax rate should be somewhere around 15% to 20% after deductions. This $15,000 conversion should cost me $2,250-$3,000 in additional tax.

I was expecting a tax refund before doing this. So we’ll see how this balances out at tax time. Either way, I have cash available to pay the additional tax if needed.

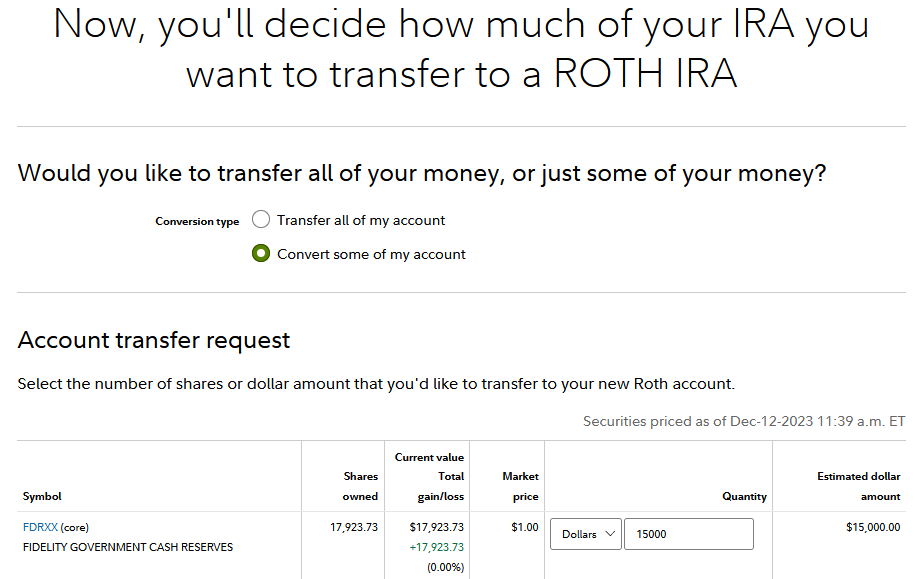

Step 4: Convert All or Some

I’m only converting $15,000 from a large account. People with smaller accounts may convert the whole thing if it makes sense.

I liquidated some assets to make cash available for this conversion. But I could have transferred any assets in the account, including individual stocks, ETFs, and mutual funds.

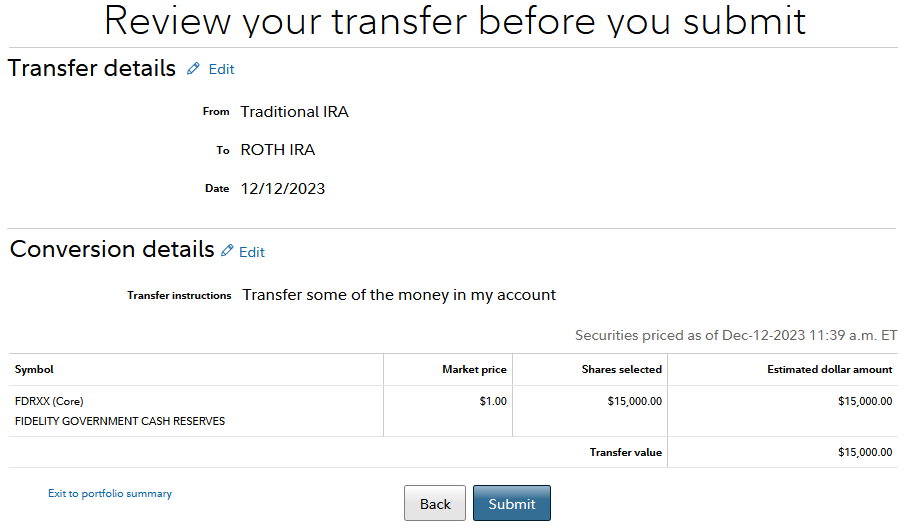

Step 5: Review and Submit

The last step is to verify the transfer details and click the submit button.

And that’s it.

This is Not a “Backdoor” Fidelity Roth Conversion

As you’re reading around the internet or researching Roth conversions, you’ll come across the term “backdoor Roth conversion”. This is a strategy for high-income individuals and couples to sidestep the Roth income limits legally.

A backdoor Roth conversion typically involves executing an after-tax contribution to an IRA or employer 401(K). That money can then be converted to a Roth without paying taxes (because it’s after-tax money).

The contribution and conversion are completed within a few days. A few complications, like the “pro-rata rule,” make it an advanced maneuver.

Now that I’m self-employed, I don’t have the luxury of having too much income to contribute to a Roth IRA, requiring a backdoor contribution. We can contribute to a Roth the old-fashioned way and convert some as well.

Conclusion

2023 may be the first of many Roth IRA conversions for us. I’ll plan to convert more money each of the next several years to keep adding our Roth IRAs.

However, 2023 was an anomaly with my decreased income and paying high premiums for COBRA health insurance.

In 2024, we’re using the ACA healthcare marketplaces for insurance, which could make us eligible for premium subsidies.

If we earn too much, or if a Roth conversion would push us over the ACA premium eligibility threshold, it may not make sense to do it.

The tax laws can also change. Multiple tax provisions will expire in the coming years, which could impact things.

Politicians could throw a curveball at us, too. But we have to make decisions on what we know today and adjust if the rules change. Major changes to IRA rules would cause an uproar, but it’s certainly possible.

I want to highlight the writing of fellow blogger Fritz from Retirement Manifesto, who has repeatedly reminded his readers about Roth conversions as part of a comprehensive retirement strategy.

He calls right now The Golden Age of Roth Conversions because the window to execute this maneuver may not last. His posts provide more background, tactics, and data to justify why Roth IRA conversions are an effective retirement planning tool.

Is a Roth conversion right for you this year? That depends on several factors. I recommend stepping through Fidelity’s 5 questions to see if converting makes sense — available here.

The additional tax bill may be unpalatable if you’re still earning a healthy salary. But those who are early in their retirement or have a decreased income this year may find the Roth conversion to be a savvy long-term move.

The Roth conversion deadline for 2023 is December 31st.

Featured photo via DepositPhotos used under license.

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

- Dividend Kings — 50+ stocks that have increased dividends for 50+ years.

- Monthly Dividend Stocks — List of 70+ stocks that pay a dividend every month.

- Dividend Champions — 140+ stocks that have increased dividends for 25+ years.