Four Fintech Obituaries

I’ve come across hundreds of fintech startups and financial products over the years blogging.

Founders and CEOs pitch me over email and in person at conferences. Marketing firms looking to drum up exposure for their clients email me constantly, hoping for a guest post or mention on RBD.

I decline most pitches and never hear about the companies again.

Occasionally, those rejected founders and companies show up in my news feed a year later, having raised multi-million dollar venture capital rounds.

Exposure to startups is one of the perks and annoyances (constant email pitches) of being a mid-tier part-time personal finance blogger.

Most product pitches don’t interest me or have little to do with my blog topic. But every so often, very interesting and innovative fintech companies want to partner with me and my modest website.

Maybe 2% are a good fit. Some go on to build thriving businesses, such as Fundrise.

Other fold.

The four fintech startups in this post demonstrated extraordinary innovation and significant success and notoriety for a time but still ended up folding the service or being acquired.

I was a customer at all four, utilizing the platforms in their glory days of growth. Then had to deal with the administrative headaches when they closed doors.

Having evaluated and sampled so many companies and products, I have a decent grasp of what attributes increase the chances of success for investing and personal finance products.

I’ll go over some lessons learned in the fintech mortuary at the end.

But first, here are four fintech obituaries.

Table of Contents

1. LOYAL3

Some of you learned about LOYAL3 from me. I loved this company while it lasted.

LOYAL3 was a commission-free online broker that empowered investors to own stock in companies they love with zero commissions (before Robinhood existed).

Founder Barry Schneider believed the company, the customer, and the shareholders (the ‘3’ in LOYAL3) were stronger together.

The company partnered with consumer-facing companies to offer investors commission-free investing. The benefit was that investors make good customers because they choose brands and services of companies they own over ones they don’t.

Another exciting perk of investing with LOYAL3 was free access to IPOs. IPOing companies gave their customers access to the IPO via LOYAL3, and all LOYAL3 customers were eligible for upcoming IPOs.

LOYAL3 conducted at least 19 IPOs and secondary offerings on the platform.

Check out this list of IPOs from 2013 to 2016. A few are up more than 1,000% since their IPOs!

Robinhood built a more robust commission-free brokerage but included what LOYAL3 omitted.

Not all stocks were available on LOYAL3. Only about 75 stocks were available on the platform.

Also, you could only buy stocks during a once-a-day trading window (a limitation many long-term investors don’t mind).

Robinhood offered all securities with unlimited trading and a mobile-first customer-friendly user interface. And in 2021, added free access to select IPOs.

Throw in incentives for Robinhood customers to invite their friends, and you have the juggernaut that upended the brokerage industry.

So if you love your commission-free trading at Charles Schwab, TD Ameritrade, M1 Finance, and Robinhood accounts, you have LOYAL3 to thank.

The rise of Robinhood and the impact of Barry Schneider’s early exit in late 2015 likely led to shutting down the company. LOYAL3 sent an email to customers with news on April 18th, 2017.

A McLean, VA-based company called Folio Investing purchased about 200,000 LOYAL3 customers and created a new platform specifically for them but charged $5 a month.

Goldman Sachs bought Folio Investing in May 2020, then sold the customers to Interactive Brokers later the same year.

Barry Schneider played an important role in moving the industry toward commission-free trade, which has saved investors billion in fees.

He’s now the Chairman & CEO of Parkside Technologies, a startup aiming to simplify global access to US stocks.

Read more: The Death of LOYAL3

2. LendingClub Peer-to-Peer Investing Platform

LendingClub disrupted the fintech world by popularizing peer-to-peer investing. The company empowered ordinary investors to earn solid interest rates by making loans to retail borrowers.

As an online lender, LendingClub could offer competitive loan rates to borrowers for up to $35,000 without going through the lengthy bank approval process.

Instead of a bank lending the money, LendingClub allowed individual investors to put up the money, earning a solid rate of return. By offering a $25 minimum note investment, investors could diversify their risk among thousands of notes, reducing default risk.

The whole peer-to-peer platform required SEC approval and an innovative technology stack. But once both hurdles were clear, the platform ramped up, and savvy investors created statistical tools such as LendingRobot and NSR Invest to optimize loan selection.

However, it was all complicated. Investors needed to understand statistical probabilities to invest effectively (or hire a service to help). It also complicated investors’ tax returns, especially when borrowers defaulted.

The SEC was friendly to this innovation early on, approving both LendingClub and Prosper. Prosper continues to operate their platform. But no other peer-to-peer platforms for individual loans were approved.

When Founder Renaud Laplanche left abruptly in 2016 for an internal transparency issue, the company seemed to lose its innovative shimmer.

LendingClub is now a public company that trades under the symbol LC. It bought an online bank called Radius and still offers online personal loans.

However, it now funnels loans to its bank and institutional investors instead of retail investors.

Turns out, the whole peer-to-peer platform aspect of the online loan business was a headache, and the technology stack didn’t age well, making new products difficult to launch.

It was easier to feed profitable loans to deeper pockets instead of retail investors.

I learned about LendingClub when Google announced a minority stake in 2013.

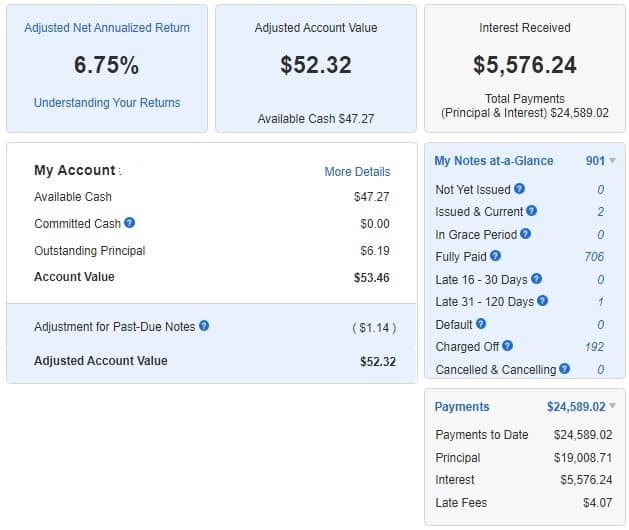

The idea that I could lend money to borrowers and earn passive income was intriguing. I signed up immediately and invested almost $20,000 over the next few years before halting new investments due to a surge in defaults.

As a LendingClub investor, I was invited to participate in the LendinClub IPO, which was an exciting time and led to a spinoff blog.

I made my last investment in March of 2017. All but three of my investment notes are either paid off or defaulted. Borrowers will pay off the last three notes by early next year.

The overall annualized rate of return on my account is about 6.75% since inception. Not bad!

But LendingClub ended the peer-to-peer investing platform in December 2020, so it remains an intriguing blip on the fintech history timeline.

Three months after his ouster, Renaud LaPlanche started Upgrade, an online lending platform and banking platform. Taking the lessons learned at LendingClub, he started essentially the same kind of business with a better technology stack and eliminated the peer-to-peer investing complications.

3. RealtyShares

Real estate crowdfunding was relatively new when I learned about RealtyShares.

After the passing of the JOBS Act of 2012, RealtyShares was a first-mover in the space, building a technology platform for accredited investors to buy partial ownership of commercial and residential properties.

There were debt, equity, and preferred equity (mezzanine debt) deals available.

These crowdsourced investments were placed into an LLC and managed by RealtyShares.

Dubbed “the LendingClub” of real estate, investors could invest as low as $2,000 to own a piece of high-quality real estate.

I bought into two debt deals for a total of $4,000 and made about 8% annualized on each deal. Both deals closed by the time RealtyShares shut its doors.

So what happened?

RealtyShares was successful at first. It managed to close $870 million worth of real estate deals across more than 1,100 projects.

However, Founder Nav Athwal left the company in late 2017, perhaps foretelling the company’s demise.

A year later, on November 7th, 2018, RealtyShares stopped offering new investments on the platform and moved toward shutting down. The company sent this explanation in an email:

As an early-stage company, we have relied upon venture capital to fund our operations. Over the past six months, RealtyShares aggressively pursued a number of financing options to continue growing the business. Unfortunately, despite our best efforts, we were unable to secure additional capital. As a result, we will not offer new investments or accept new investors on the RealtyShares platform.

The company burned through too much money too fast and failed to demonstrate a path to profitability, losing the confidence of venture capital investors.

RealtyShares invested heavily in customer acquisition but struggled to list enough loans to satisfy investor demand.

Venture capital investors demanded faster growth, but deals still needed manual work, and RealtyShares couldn’t keep up the deal flow while maintaining high standards.

Employees and office space in San Francisco are expensive, which didn’t help.

RealtyShares continued to service its outstanding deals until the following May, when it contracted IIRR Management Services, LLC to manage the remaining investments.

Rival first-mover, Fundrise, chose a slower growth model, expanded its customer base to non-accredited investors with eREITs, and remains in business today.

Crowdstreet, RealtyMogul, and EquityMultiple now offer similar investments to what RealtyShares offered before it shut down.

According to LinkedIn, Nav Athwal is now a Managing Director at TerraAg Ventures, where he manages a portfolio of sustainable farmland investments.

4. Motif Investing

Founded in 2010, Motif Investing popularized thematic investing. Motif encouraged its customers to invest in themes, or motifs, to benefit from trends in business and technology.

Its innovative online brokerage platform offered investors the ability to invest in various investment themes with just a few clicks.

For example, if investors wanted to invest in 3D printing, they could find a 3D printing motif with 2-30 stocks and invest money into each company with one investment.

Users could also create personalized motifs and share them with the community.

It was like creating and investing in your own mini-ETF.

Trades cost money at the time, but Motif was efficient by allowing you to own fractional shares of multiple stocks for just $9.99.

As the platform matured, it also started offering IPO access akin to LOYAL3.

It offered customers more than 180 IPOs and secondary offerings on the platform, including big winners such as Novavax, up 10,000% since its IPO (see a full list of Motif IPOs here).

Then Motif added Blue, which was an attempt at creating a robo-advisor type of recurring revenue model.

The company later went down the path of ESG investing (environmental, social, governance) with Motif Impact, but Impact never seemed to garner much attention.

Swell Investing was another ESG platform that closed shortly before Motif (Swell was meant to be #5 on this list, but I ran out of time).

These products came out while the brokerage industry and retail investors were headed in another direction (commission-free trades).

Motif’s fancy product offerings were not compelling enough to attract droves of new investors, so the company focused attention on its institutional/advisor platform.

On April 17th, 2020, Motif Investing customers received an email informing them the company was ceasing operations.

All individual customers and registered investment advisor (RIA) accounts transferred to Folio Financial, the same McLean, VA-based boutique wealth management custodian, fintech, and online broker that previously purchased the customer accounts from LOYAL3 and BuyandHold.com.

A few weeks after the Motif and Folio announcement, Charles Schwab announced its acquisition of Motif Investing’s technology, including source code, patents, and algorithms.

Schwab also hired most of Motif Investing’s San Francisco-based engineering team and its founder, Hardeep Walia.

A press release suggested the ESG and “direct indexing” capabilities were of most interest. But it’s not clear how much of Motif’s technology is being used today.

Goldman then bought former Motif customers from Folio Investing (along with the LOYAL3 customers) and later sold them to Interactive Brokers (IB).

Despite Motif’s inability to continue, it was a great run and successful exit.

Motif reimagined how retail investors invest in stocks, built a solid customer base, and its legacy continues to add value to Schwab and IB.

Lessons Learned in the Fintech Mortuary

It’s important to acknowledge that these four platforms were more successful than most fintech startups.

They raised money, conducted business, attracted thousands of customers, and completed millions of transactions on their systems.

So we can learn from their successes even though they didn’t last.

Create one extraordinary product first

Do one thing, and do it better than anyone. — Orville Redenbacher

I attend a conference called FinCon every year.

And every single year, there’s a different new personal finance app that will “simplify and streamline your entire financial life and SAVE YOU MONEY!”. Budgeting, planning, retirement, lending, goal-setting, estates, blah blah blah.

Nobody wants to abandon their entire financial life and jump on a buggy new app with a dozen users.

Consumers, investors, and small business owners want their financial products to do one thing really well.

The success stories I’ve seen follow this pattern.

Fintechs must earn their customers’ trust before upselling and becoming their go-to one-stop financial product. It can be done, but it takes years, not months.

An early startup can’t do everything better than everyone else on day one.

Focus on one pain point that other companies haven’t figured out yet.

Do one thing, and do it better than anyone first. Then expand. But don’t stop improving your core offering.

Founders matter

In the first three obituaries above, the founders all left before the businesses closed.

Losing a visionary and primary innovator makes it harder to adapt to the future. Seasoned executives struggle to replicate the success of visionary founders.

Research some of the top-performing growths stocks, and you’ll notice that founder-led companies are a common attribute of great growth stories.

When a founder leaves a startup, future success is less certain.

Live and die by venture capital

Startups that pursue multi-million venture capital funding become accountable to their investors.

If a company chooses venture funding, they are on the hook to deliver, perhaps not on their own terms.

Failing to meet someone else’s expectations can mean the end.

Don’t solve a problem that doesn’t exist

Fintech startup founders should always ask themselves this question: What problem does the product solve?

Many new startups try to insert themselves into the middle of an existing process to take a slice of the profits.

Or, their product’s incremental improvement on the status quo isn’t significant enough to convince a customer to buy into their idea.

If there isn’t a real problem to solve, there may not be a viable product.

Investors were losing billions to trading fees. LOYAL3 and Robinhood fixed that.

Retail investors were missing out on solid returns and diversification via high-quality real estate. RealtyShares and Fundrise empowered investors to profit.

Connecting your bank account to a financial service app used to require 1-3 business days and two micro-deposits. Plaid APIs fixed that problem.

Aspiring entrepreneurs should conduct extensive market research (current companies and those that failed) before launching the next fintech startup. There’s a good chance somebody has tried the idea already.

Featured photo via DepositPhotos used under license.

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

- Dividend Kings — 50+ stocks that have increased dividends for 50+ years.

- Monthly Dividend Stocks — List of 70+ stocks that pay a dividend every month.

- Dividend Champions — 140+ stocks that have increased dividends for 25+ years.