Here’s How I’m Investing Each Month

I’ve maintained a long-term buy-and-hold investing strategy since about 1995. The month-to-month details have changed quite a lot over the years, but the basic principles are mostly the same:

- Invest first, spend second

- Max out tax-advantaged accounts first

- Invest in taxable accounts second

- Keep transaction costs and stock sales to a minimum

- Diversify income streams

- Always be investing

This blog began as a chronicle of my monthly investment selections when I started writing back in 2013.

A few years back, I stopped monthly and quarterly investment updates, but I continue to share semi-annual updates on my Portfolio page.

That page is a good snapshot of my total investment portfolio.

But it doesn’t share where I’m investing new money each month.

My current strategy includes monthly investments into stock and bond funds, individual stocks, and real estate crowdfunding REITs.

With every new brick I lay, my wall of financial security and financial independence grows taller and stronger. There are no shortcuts.

Here are the details of my month-to-month investing activity (or skip to the summary).

Table of Contents

Employer-Sponsored Accounts (Fidelity)

I work for a high-quality employer that invests heavily in the well-being of its employees. The company has about 10,000 workers.

Golden handcuffs bind me.

Our health and wellness benefits are incredibly generous, and the retirement investment plan is the best I’ve ever seen.

My employer uses Fidelity to administer a combined 403(b) and 401(a) retirement plan, enabling me to contribute about 17% of my salary toward retirement every year.

The combined account structure and 17% maximum (vs. a normal 15% limit) are confusing — I explain what I can here.

They also provide an employer match at about 10% of salary — awesome.

I’ve always taken a hands-off approach in workplace retirement accounts. Once I pick my funds, I let them ride.

I still own two funds from my very first job. FOCPX is up more the 1,300% since 2002. FCNTX is up 675%.

My employ provides several low-cost index fund options for investments. But last year, they removed FSKAX (total US stock market index) akin to the Vanguard VTSAX and VTI.

Employees complained about its removal, but we did not prevail.

So to get similar index coverage as FSKAX, I invest a portion of each paycheck into three separate US Fidelity stock index funds plus an international stock fund.

- FXAIX — Fidelity S&P 500 Index (25%)

- FXMDX — Fidelity Mid Cap Index (25%)

- FSSNX — Fidelity Small Cap Index (25%)

- FTIHX — Fidelity Total International Stock Index (25%)

I don’t buy bond funds in this account because I own them in a traditional IRA.

There’s a lot to love about my employer’s retirement plan. As long as I’m employed, the contributions are automatically invested without thinking about it — more than $2,000+ per month.

M1 Finance Account

I opened an M1 Finance taxable investment account when the company was just a baby in 2017.

Now it’s one of the fastest-growing fintech companies with more than $5 billion in client assets.

M1 also provides banking services like checking accounts and, soon, an ownership rewards credit card that pays you cash when you spend at companies where you own the stock.

My goal with this M1 Finance account is to create a passive dividend income stream that grows and compounds automatically. I own 25 stocks and ETFs in the portfolio, up from 10 when I first started it.

Every two weeks, I contribute $750 to this portfolio. I’ve fully automated the bank transfers.

The platform automatically puts my new money toward the pie that is most underfunded.

M1 Finance works differently than traditional brokers. You build your ideal portfolio first using pies, then fund it over time.

You can have unlimited investments and buy fractional shares of each instead of buying one stock or ETF at a time.

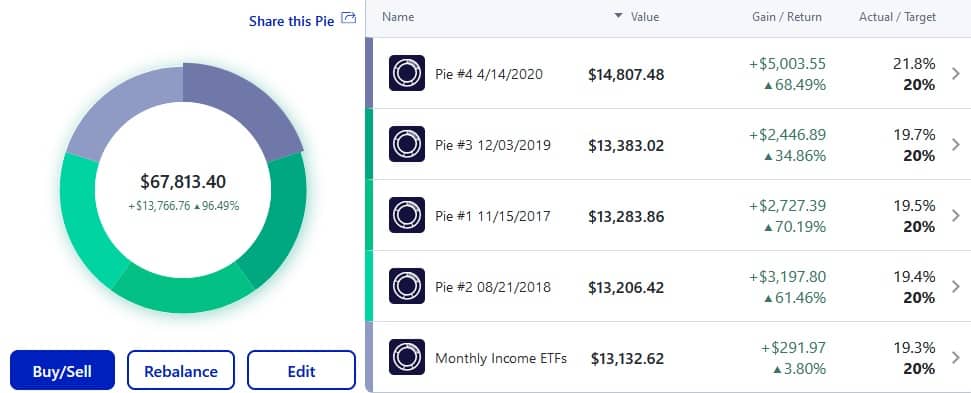

My M1 Finance portfolio consists of five separate pies, each with five stocks or ETFs.

Each pie makes up 20% of my portfolio, and each stock is 20% of each pie.

Four pies contain high-quality dividend growth stocks. The fifth pie has five monthly-paying tax-efficient dividend ETFs (←more info on that pie).

The whole portfolio looks like this:

The system will fund the Monthly Income ETFs portfolio first when I make the next deposit. Then Pie #2 and so on until all $750 is invested and the pies are closer to 20% of the total portfolio.

Then within each pie, the money is invested in the most underfunded stocks.

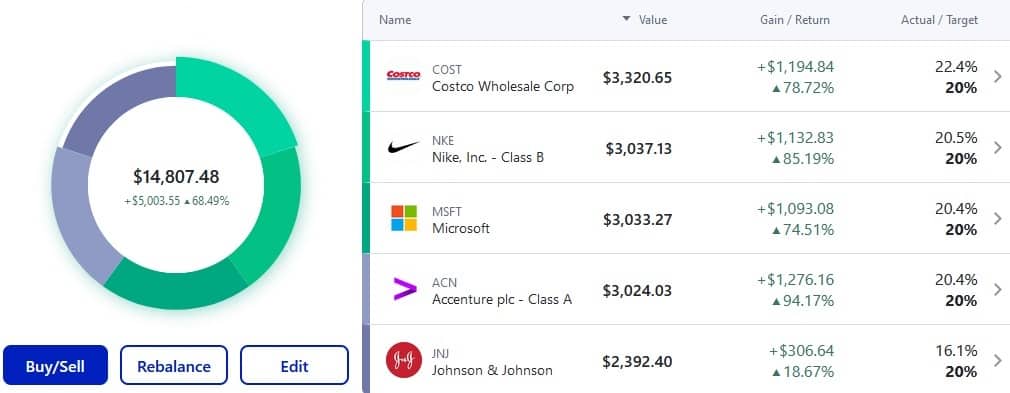

Below is a look inside my top-performing pie, Pie #4. Since this pie is way ahead of the other four, it won’t get any new funds until the others catch up.

If I were investing directly into this pie (which you can do), money would first go to JNJ because its actual percentage is far below its target.

Dividends reinvest right back into the portfolio once the cash balance hits $25 or more.

The $750 investment is made at the same time twice a month, making it easy to dollar cost average funds into the portfolio.

The JNJ actual vs. target percent illustrates one minor issue with the way I have it set up.

JNJ will not get new funds until the other pies catch up. When they do, the algorithm will fund JNJ first in Pie #4.

There are workarounds to combine pies. But I’m waiting for the functionality to be implemented.

Once the “merge pies” functionality is added, I’ll combine the four stock pies and make that 80% of my portfolio. Then keep the muni-bond monthly income pie at 20%.

I’m always weighing adding more stocks, ETFs, and pies, but I’m comfortable with 25 holdings for now. If needed, I’ll swap out lousy stocks for better ones.

Read my full M1 Finance review here.

Fidelity Individual Investment Account (Dividend Growth)

My Fidelity dividend growth portfolio has been in the making since 1995.

I transferred all previous DRIP accounts into a TD Ameritrade account a few years back, then transferred my TD Ameritrade account into Fidelity in 2018 to have most of my money with one broker.

This account holds the majority of my non-retirement investment money.

I’m not currently adding new funds to the account, but it generates close to $1,000 in dividends every month. Once my cash gets to about $1,500, I invest funds into one stock or ETF. But I’m considering adding $1,000 per month in the future.

Usually, I buy what I deem to be an undervalued dividend growth stock at the time of purchase, often using my Dividend Aristocrats ranking system.

Since the portfolio holds about 50 stocks, I aim to add to my existing holdings instead of buying new ones.

This helps to maintain a reasonable number of stocks to follow. I’d rather own more shares of stocks I already like at this stage.

There is some overlap between my M1 Finance and Fidelity accounts. Many of my M1 stocks are perpetually overvalued (best of breed), so I dollar-cost average instead of waiting for a pullback that never happens.

This portfolio is the core of my dividend growth strategy, building a dividend income stream to fund retirement spending.

Recent buys: PFE, BMY, VZ

Fundrise Real Estate Crowdfunding

I started investing on the Fundrise real estate crowdfunding platform back in 2017 when I became aware of it.

Fundrise enables ordinary investors to buy high-quality commercial and multi-family residential properties for as little as $10.

Just sign up, pick an investment strategy, and connect your bank account. Fundrise allocates your deposits automatically.

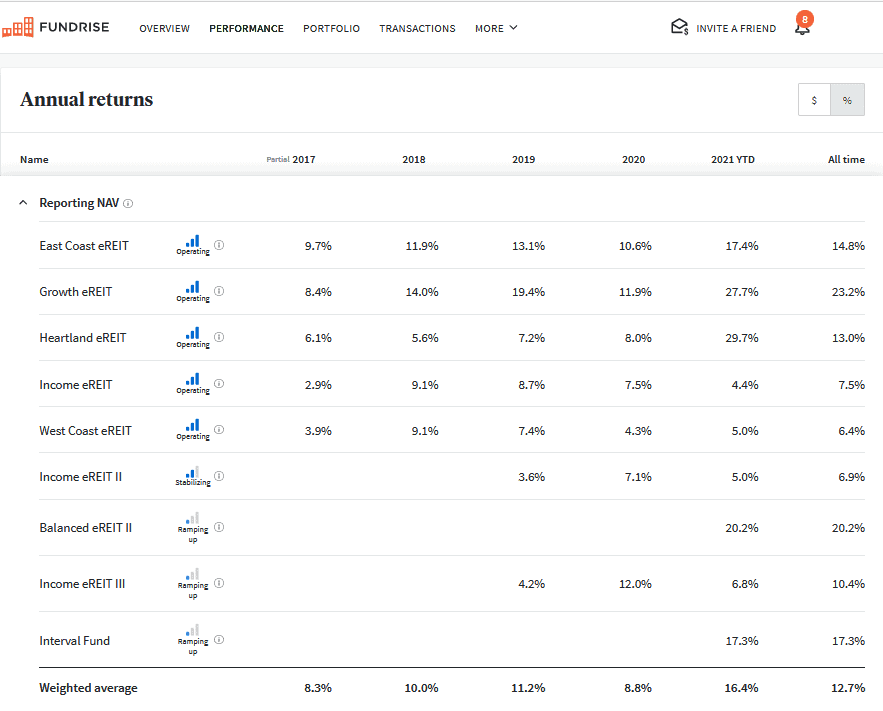

Since 2017, I’ve earned annualized returns of 12.7% (weighted average).

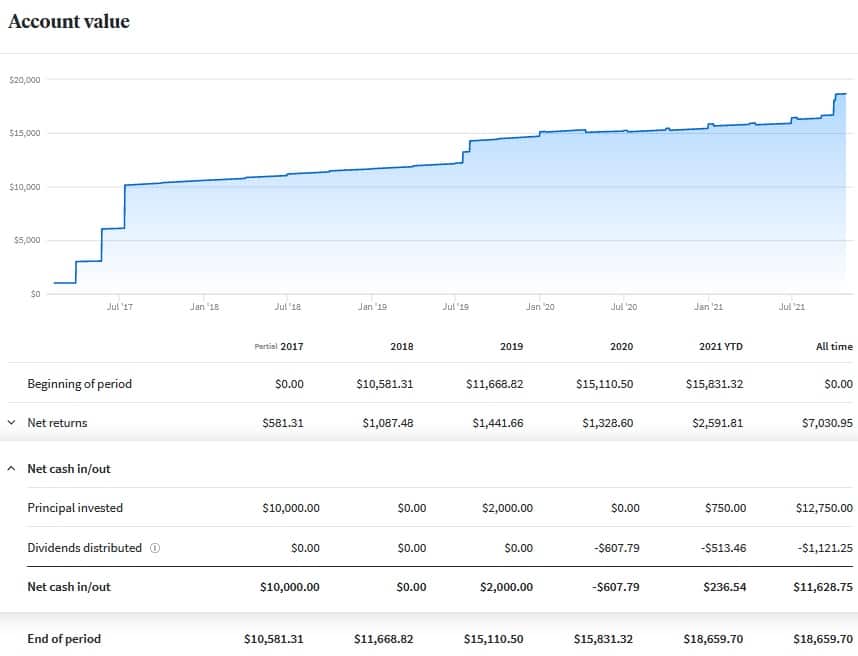

I’ve invested almost $13,000 into the platform. My account is now worth more than $18,000.

My only regret is I didn’t invest more in the early days. I stopped investing when I hit $10,000 and let that ride for a while. Then added more in 2019 and again this year.

I’ve decided to add $500 per month to my Fundrise portfolio from now on using automated deposits and investment allocations.

My account is set to the Balanced Portfolio, so when I add money or receive dividends, Fundrise automatically allocates my funds into the suggested eREITs. My portfolio of eREITs gives me a slice of ownership in almost 100 different real estate investments.

Fundrise has moved away from self-directed eREIT investing. I can still do it, but it’s more efficient for the company to allocate funds for me.

Regulations have always hindered Fundrise’s capacity to innovate. But a new fund called the Interval Fund (an eREIT) is not limited in size by the SEC. All of the older funds were capped at $50 million.

To learn more about Fundrise, read my comprehensive Fundrise review.

Please note: This is a testimonial in partnership with Fundrise. We earn a commission from partner links on RetireBeforeDad.com. All opinions are my own.

Notable Other Investments

I want to mention two other notable investment areas that I don’t invest new money into every month but are still a significant part of my investment activities.

IRAs

Between myself and Mrs. RBD, we have five separate IRA accounts.

She has a traditional IRA rolled over from a previous employer and a Roth IRA we started years ago.

I also have a traditional IRA and Roth IRA, plus a SEP IRA for business profits.

Four of these IRA accounts are on automation mode, with simple allocations into index stock and bond mutual funds. We invest new money into existing holdings, and all distributions are reinvested.

The fifth IRA, my traditional IRA that was a rollover from a former employer, is where I do a bit of speculative investing.

As detailed in a post called Growth Stocks vs. Dividend Stocks, I invest a small portion of my overall net worth into speculative growth stocks.

These are disruptive companies in high-growth phases. Many appear to be overvalued and are often volatile. So it takes some fortitude to buy-and-hold — but the returns are worth it.

I’m still primarily invested in index mutual funds this IRA, but every month I buy one or two speculative investments with about $2,000 to $5,000. I own about 20 speculative growth stocks and don’t plan to go higher than 25.

Some of these investment ideas come from The Motley Fool Stock Advisor and Rule Breakers newsletter services, and others come from my own research and finding investable trends.

I don’t add new money into this IRA every month, but I occasionally sell mutual fund holdings to free up cash to invest in growth stocks.

My growth stock portfolio is outperforming my index funds, so individual stocks are becoming a larger portion of my portfolio than I originally intended.

Recent buys: DXCM, HOOD, BYND

Virginia 529 College Savings

My oldest child is nine. I invested $300 per month into his Virginia 529 account for the first eight years of his life.

But in January 2021, I decided to start front-loading all of our college savings investment funds.

So instead of investing $300 per month per kid (three kids), I invest the maximum for each kid in early January.

That’s $12,000 total.

There are a few Vanguard stock index funds available, so I just invest in those to keep it simple.

Why front-load? Two reasons.

- Consistent January investing is more likely to outperform monthly investing (money invested earlier will rise and compound more over time).

- It simplifies my finances. One investment per kid instead of twelve is just easier to transact.

That said, I “put $1,000 aside” every month in a spreadsheet tab where I plan for future expenses. So come January, the money is available.

Summary

Employer-Sponsored (403(b), 401(a))

Total Monthly Amount: $2,000+

Investments: FXAIX, FXMDX, FSSNX, FTIHX

Frequency: Every other Friday

M1 Finance Dividend Growth Portfolio

![]()

Total Monthly Amount: $1,500 + dividends

Investments: 20 stocks, 5 ETFs (muni bonds, preferred stock)

Frequency: Every other Wednesday

Fidelity Dividend Growth Portfolio

Total Monthly Amount: ~$1,000 (dividend income)

Investments: Undervalued dividend growth stocks

Frequency: One stock per month

Fundrise Real Estate Crowdfunding

Total Monthly Amount: ~$500 + quarterly dividends

Investments: Diversified eREITs

Frequency: Once a month

Conclusion

Total up all of those investments, and it’s more than $5,000 of investments per month. Most of the money goes into the stock market.

That number surprised me!

A few things to keep in mind.

- When the stock market falls, my net worth will tumble. But my investment horizon is more than ten years, so I will hold through turmoil and buy more.

- I max out my workplace retirement plan. I could take home more money but opt to invest for my future and reduce my tax burden. There’s also an incredibly generous employer match, which is a major reason why I still work there.

- I’m not cash-flowing $5,000+ each month (salary minus spending). My salary isn’t that high, and kids and housing are expensive. A portion of investment dollars come from dividends resulting from decades of investing. I also tap savings and proceeds from my condo sale to invest alongside excess cash flow.

- Two months per year have three pay periods. Those months are bigger.

- This is what I do. It’s probably not what you should do since you have a different financial situation than me. Evaluate your situation decide what specific investment strategy is best for you.

And that’s all. I’ve reduced sharing these kinds of updates over the years for various reasons. But readers still seem most interested where I share details of my investing and portfolio.

I’m not a professional investor — just a guy who writes words on the internet and does not give investment advice.

Photo credit: iStock.com/Bogdanhoda used under license.

Disclosure: The author is long all stocks mentioned in this article.

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

- Dividend Kings — 50+ stocks that have increased dividends for 50+ years.

- Monthly Dividend Stocks — List of 70+ stocks that pay a dividend every month.

- Dividend Champions — 140+ stocks that have increased dividends for 25+ years.