2 High-Yield Alternatives to Savings Accounts

Inflation is eating away at our wealth quarter-by-quarter.

Inflation is eating away at our wealth quarter-by-quarter.

It appears to have peaked in May 2022, thanks to the Federal Reserve’s aggressive rate increases.

But the chart below shows how the products we consume have recently become more expensive.

Source: https://tradingeconomics.com/united-states/inflation-cpi

The Federal Reserve is mandated to target 2% annual inflation as measured by the year-over-year change in the consumer price index (CPI).

Here’s why:

When households and businesses can reasonably expect inflation to remain low and stable, they are able to make sound decisions regarding saving, borrowing, and investment, which contributes to a well-functioning economy.

Long-term stock market returns have averaged around 10% since 1928. That puts real stock returns, adjusted for inflation (when tamed), at roughly 8%, which is why the stock market is so compelling for buy-and-hold investors.

But when inflation is higher, like now, real returns shrink quickly.

In 2022, the S&P 500 is down close to 20%. If you adjust for inflation, which could average 7% this year, that’s no good.

To alleviate the effects of market volatility, asset price variability, and inflation, it’s best to diversify your investments among various assets, including bonds, real estate, cash, and alternative investments.

High-yield savings account interest rates have risen significantly in 2022 due to the Fed rate increases. But even the highest FDIC-insured savings rates are still below inflation.

That has investors searching for high-yield alternatives to keep up.

I’ve moved some money out of high-yield savings to enjoy better yields with minimal additional risk. These higher yields come with slightly reduced liquidity (quarterly to annual, usually).

But since I don’t need these dollars in the next year, I’m OK with that.

To be 100% clear, none of these high-yield alternatives are FDIC-insured. They are not bank accounts. The first option on the list requires investors to be accredited, while the other three do not.

Since the options below are not FDIC-insured, a slightly higher risk tolerance is necessary (except #2).

You’ll also need to weigh the hassle of moving money from a savings account to an alternative to gain an extra few percentage points. Higher dollar amounts make it worth your while.

If you decide to invest in one of these products, please perform due diligence in alignment with your investment objectives.

1. EquityMultiple Alpine Notes

EquityMultiple is a real estate crowdfunding platform that connects accredited investors to high-quality, pre-vetted commercial real estate investment opportunities.

The company partners with experienced lenders and real estate companies around the United States to source deals for its platform investors.

It has recently added a new product called Alpine Notes, which typically yield 5.5% to 6.5%.

Alpine Notes offer the opportunity to earn interest for specific terms, usually 90-270 days. EquityMultiple uses the money to pre-fund investment opportunities on the EquityMultiple platform.

EquityMultiple’s primary real estate investments are individual commercial and residential properties with an excellent track record of 18% annual returns on more than $4 billion of real estate transactions.

But those investments require higher minimum investments (>$10,000), single property risk, and more complicated tax reporting (Schedule K-1).

Alpine Notes offer $5,000 investment minimum investments, shorter durations, simple 1099-INT tax forms, and monthly interest payments. They are available on a rolling basis (about every 15 days), so investors can reinvest the principle into another fund when the current note matures.

Since Alpine Notes are not savings accounts and EquityMultiple is not a bank, these notes are not FDIC-insured. However, EquityMultiple offers first-loss protection on these notes, whereby EquityMultiple holds a portion of the notes issued in a first-loss position.

If something catastrophic happened to EquityMultiple, you could lose all of your money. However, EquityMultiple is in the real estate business, owning real assets — not funny money, magic crypto coins.

I’ve moved $10,000 out of cash savings into a six-month Alpine Note yielding 6.5%, more than double what my high-yield savings account yields. This is my second EquityMultiple investment to complement a May 2022 $20,000 purchase into a mix-use retail/residential property.

Read my EquityMultiple Review to learn more about the investing platform. Learn more about real estate crowdfunding.

2. I Bonds and Treasuries

The U.S. Government issues a savings bond called Series I. It’s a risk-free savings product that pays interest to fight against inflation.

The interest rate is derived from a fixed rate that doesn’t change and an inflation rate set twice a year.

For bonds issued from November 1st, 2022, through April 30th, 2022, the combined rate is 6.89%. Here is the latest information from TreasuryDirect.gov.

The variable rate fluctuates with inflation.

Bond buyers get a guaranteed six months of that yield before the rate changes again. So if you buy the bond on April 30th, the 6.89% yield will continue for the next 180 days.

Since the U.S. Government issues and backs these bonds, these are essentially risk-free investments.

Here are a few things to keep in mind:

- Investors can only buy I bonds at TreasuryDirect.gov (terrible user experience, confusing as hell)

- There’s a $10,000 maximum investment per person per year.

- The rate fluctuates as inflation rises and falls, potentially making these more or less desirable in the future.

- The bonds pay semi-annual interest payments (paid 6 and 12 months after purchase).

- This investment is taxable as ordinary income, but not until you cash out the bonds (making them tax-deferred). Interest automatically reinvests.

- These are Illiquid for one year. If you redeem I-bonds before five years, you will forfeit three months of interest.

I intend to let the investment ride for as long as the interest remains competitive compared to bank savings.

We’ve been trained for years to hate Treasuries because the rates were so low. Now that the Fed is increasing rates again, short-term yields (T-bills) are better than savings rates.

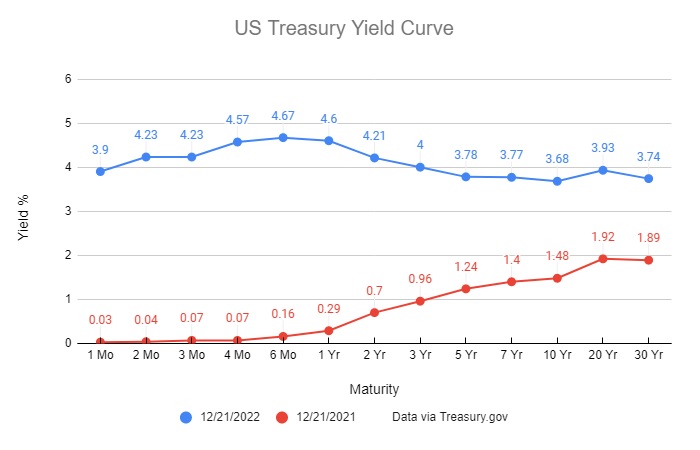

Here’s the December 21st yield curve compared to a year ago.

Investors can buy T-bills with maturities in the four months to one-year range (4.57% to 4.67% at the time of writing) and beat the yield on the best high-yield savings accounts.

There’s a $1,000 minimum and virtually no maximum. Investors can easily purchase individual Treasuries through full-service online brokerage accounts or TreasuryDirect.gov.

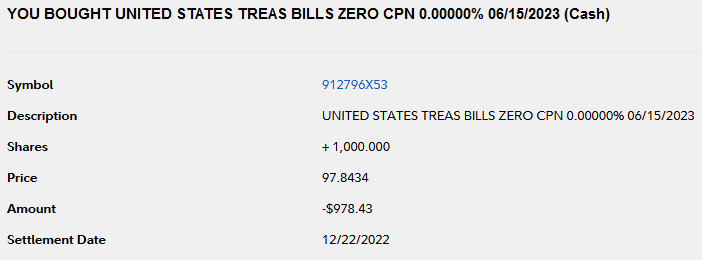

I bought a June 2023 T-bill yielding about 4.6% in my Fidelity IRA as I was writing this post just for fun.

T-bills don’t pay interest, per se. They are sold at a discount to face value (par value). When it reaches maturity, it pays back the face value. Longer-duration bonds can be used for passive income.

In this transaction, I paid $978.43 on December 21st and will receive $1,000 on June 15th. That equates to a roughly 4.6% yield.

The blue line in the yield curve above is inverted, meaning the long-end yields are below the short-end yields. The spread between the 2 and 10-year yields is the most important.

Yield curve inversion is a classic economic indicator that a recession is likely on the horizon.

Conclusion — High-Yield Alternatives to Savings

The more money investors have in cash savings, the more they can benefit from moving money into higher-yielding savings account alternatives.

If your cash is earning less than 2% in savings right now, start by moving money to an FDIC-insured high-yield savings account at a minimum.

Then consider these alternatives if you’re looking to bump the yield even more.

Though it’s still hard to beat inflation with low-risk investments, we can get close. And as year-over-year inflation moves lower, the Fed Funds rate may remain high — unless a recession pummels our economy.

We can’t predict the future, so it’s best to adjust today based on what we know and modify as appropriate.

Please note: The original version of this article included a reference and links to a company called Tellus. I stand by my research and vetting of the company, its business model, and practices. However, the company miscommunicated its relationships with banking partners which may have misled consumers to believe accounts are FDIC-insured. They are not. We disclosed the risks clearly on this website, indicating the accounts are not FDIC-insured. But I’ve chosen to remove references to the company due to a pending FDIC investigation into its communication practices.

Featured photo by Ankush Minda via Unsplash

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

- Dividend Kings — 50+ stocks that have increased dividends for 50+ years.

- Monthly Dividend Stocks — List of 70+ stocks that pay a dividend every month.

- Dividend Champions — 140+ stocks that have increased dividends for 25+ years.