12 Ways to Build Confidence to Change Careers

After 20 years in information technology (IT), I decided to change careers to be a full-time blogger in early December.

It’s an exciting milestone I’d been planning for about five years.

Monday morning, after my last day at work, I sat down at a different computer without the looming threat of Microsoft Teams meetings.

I didn’t hate my 20-year IT career. But I didn’t love it either.

A big challenge for people looking to change careers is finding something else to do.

That wasn’t hard for me. I already knew I wanted to be a full-time blogger.

But switching from full-time employee to full-time self-employment is still a big step.

If you’ve got a runway, there are several ways to plan and reduce risk before taking the plunge.

Here are 12 things that gave me the confidence to change careers.

Table of Contents

1. Know Where to Land

It’s better to run toward a new career than from a job you don’t like.

Find where to land before jumping.

People tend to dislike their careers before knowing what to do next.

Leaving a career because you don’t like it could be a bad idea.

Tolerate your unsatisfying job until you have a desired destination, like a new employer or a side business ready for the next level.

I ran my side business for nine years before taking it full-time.

In internet years, that’s nearly a lifetime. My second website is six-years-old.

I wrote new blog posts every week for about six years to build my online business.

My websites are established and profitable. I have business bank accounts, an entity (LLC), several partnerships, and monetization strategies already in place.

The landing pad made my career change possible.

2. Secure Spousal Support

If you’re married, having a supportive spouse is the most crucial prerequisite before taking the plunge into a career change.

But you will only earn the support if you’ve established a landing pad or produced a convincing plan.

Mrs. RBD had a full-time career before we had kids ten years ago. But she has mostly stayed home since 2013.

Only recently, she has gone back to work part-time. The money helps, but it’s not nearly enough to support us alone, and there’s no healthcare benefit.

She is not a risk taker and was uncomfortable with me leaving full-time work at first.

I wanted to talk about it all the time. But the conversations became repetitive, and she started ignoring the topic when she could.

That came across as unsupportive.

She was always supportive of my side business and willing to listen to full-time career frustrations.

But figuring out the healthcare situation worried her, especially since our son’s diagnosis.

We’ve always talked about financial independence numbers. But it took some explaining how we’d pay for things without my salary.

To smooth the transition, we agreed to keep our healthcare the same for 12-18 months. And if the career change doesn’t work out, I will return to my old career.

Once she understood how we’d manage our healthcare and monthly expenses, she became more comfortable with the idea of changing careers.

She’s now fully onboard (as long as I don’t talk her ear off about it).

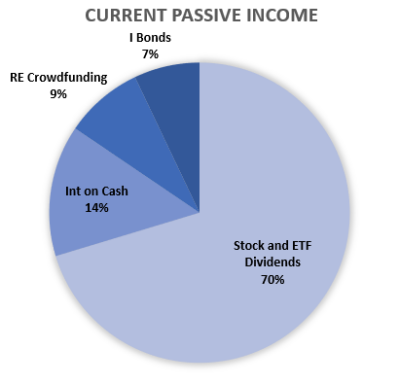

3. Build Passive Income

Passive investment income streams provide consistent cash flow when you’re not working for money.

I had a passbook savings account when I was 10 years old, which paid me interest just for leaving my money there. That blew my mind.

Then in 1995, my Uncle gifted me one share of Chevron stock, and I started building a dividend stock portfolio from there.

But passive income streams take time and money to build into anything significant.

Our stock and ETF investments in non-retirement accounts now pay about $1,100 per month. That’s not enough to cover our household expenses, but it covers big chunks.

We earn another $500 from interest on cash savings, real estate crowdfunding, and Treasury I Bonds.

This income is taxable. But we anticipate our taxable income will be much lower in 2023, lowering our overall tax burden.

We’ll receive tax-free dividends and capital gains if we earn less than $89,250 in 2023 (more on taxes below).

We don’t intend to sell any investments as I transition to self-employment. But that is always an option.

These passive income numbers do not reflect our retirement accounts, which I consider off-limits until age 59 1/2.

Here’s a rough breakdown of our passive income sources:

Use the surplus from your day job income to invest in passive income streams. It will take time, but passive income can cover expenses in retirement and while you transition to a new career.

4. Stash Cash in the Bank

A liquid cash balance is critical for any life transition.

Cash is a buffer to maintain your basic current lifestyle without an income.

I am only comfortable changing careers with more than sufficient cash in the bank.

We have at least a year’s worth of living expenses in a high-yield savings account.

Our cash on hand spiked when we sold our rental property in 2019. We’ve maintained a healthy buffer ever since.

We have plenty of money invested elsewhere, so I don’t mind the cash missing out on market returns.

It also allows us to look at new investment opportunities for more passive income. I’m looking at farmland, more crowdfunded real estate, and other alternative investments in 2023.

Cash in the bank buys flexibility and options.

Transitioning to self-employment will require we draw down some of our savings. The amount depends on my business’s success and our commitment to controlling spending.

Willingness to spend cash savings is imperative.

5. Choose a Fixed Mortgage Rate

We saw record-low mortgage rates during the past decade. Hopefully, most of you refinanced below 4% at a 30 or 15-year fixed rate.

Variable rates may be necessary to get a lower payment for homebuyers today, which could lead to some uncertainty five to ten years from now if rates stay elevated.

But fixed interest rates give you better visibility.

We’ve refinanced six times since I bought my first property in 2006.

The last refinance was in September 2020.

We got a 20-year fixed mortgage rate for our home at 2.75%.

Our high-yield savings account pays more than that now, risk-free.

We’re achieving a sort of risk-free arbitrage just by paying the minimum mortgage payment.

30-year fixed mortgage rates are now close to 7%.

This is why extra mortgage payments were not optimal when rates were so low for so long.

I’m OK with paying off a mortgage early under the right circumstances (a lump-sum payoff if possible).

Instead, the low mortgage rate makes our house payment easy to handle and predictable as I transition and beyond. There’s no urge to pay it off or move.

6. Eliminate Other Debts

Saying you’re “debt free except for the mortgage” ignores the massive bank obligation. It matters.

But it’s comforting not to have any consumer debts.

I’ve never had credit card debt.

We eliminated car payments from our lives in late 2016. I have no regrets about that.

If one of our cars poops out while I’m transitioning to self-employment, that would be a major headache. But we have the cash to repair or buy another if needed.

Now, we can focus solely on living expenses instead of debt service payments.

Easy access to debt is a perpetual test of self-control.

Resist the urge to borrow to master your finances and preserve flexibility as you consider career alternatives.

7. Invest for the Long-Term

From 1928 to 2021, the S&P 500 averaged above 10% total annual returns (including dividends).

Looking at rolling averages:

- Stocks have averaged positive returns for each 10-year period during the last 93 years

- Over the past 75 years, the lowest 15-year average return for stocks was 5.5%

More than half of our assets are in retirement accounts, most of which are in low-cost index funds. Roughly 90% stocks, 10% bonds.

We won’t touch that money for at least 12 years.

20+ years of consistent tax-deferred investing through my employer plans has given our family a solid foundation of retirement savings.

If we do nothing and earn conservative 5% returns over the next 14 years, that nest egg will double on top of whatever else we invest in the next decade.

We’ve saved enough already for that to be a meaningful amount — enough to retire comfortably.

Long-term thinking is your superpower when it comes to stock market investing.

Day-to-day stock market fluctuations are inconsequential.

Past performance is not indicative of future returns. However, chances of success increase if you are patient and unwavering.

I sleep well knowing there is a high likelihood that our wealth will substantially grow if we simply don’t touch our retirement investments.

But the stock market will not be my savior in the near term if my new career fails.

8. Prioritize Healthcare Continuity

In the U.S., healthcare is tied to employment. This creates a mental block when thinking about changing careers.

How can we continue receiving excellent affordable healthcare without an employer plan?

Healthcare has always been available outside of employment. The plans are so overwhelming that people don’t want to leave the comfort and ease of the golden handcuffs.

Thankfully, there are some government programs to maintain healthcare continuity and serve those without employer-sponsored health insurance.

The Consolidated Omnibus Budget Reconciliation Act of 1985 (COBRA) mandates that employers continue to offer the same health insurance plan for 18 months after an employee leaves the company on good terms. Employees must pay the full insurance premiums.

We used COBRA when I lost my other job back in 2017. It worked fine, except the administrator wasn’t transparent, so I worried about our plan’s stability.

My latest employer uses a legitimate third party that supports online payments and account viewing, so I’m more comfortable with COBRA this time.

COBRA is expensive. That’s because good employers have excellent plans that cost a lot.

I’m willing to pay extra to continue our existing healthcare plan. We use our healthcare frequently and hit our deductible quickly because of the cost of diabetes devices.

Without COBRA, it would have been harder to convince my spouse to leave my career.

Another helpful tool is from Affordable Care Act (ACA), enacted in March 2010. Though this law took some political heat for a decade, it helps people like me find suitable healthcare plans without an employer.

When we transition from COBRA in 12-18 months, I’ll look to ACA, direct health insurer plans, and health insurance agents to find the best plan.

Solid healthcare coverage gives me the confidence to take a career risk without putting my family’s health at risk.

9. Understand the Tax Code

I’m not a CPA or tax attorney, so take this next part with a grain of salt.

The public lacks confidence in the government and rarely cites the IRS as helpful.

But the U.S. tax code favors people with low incomes and small businesses.

So if you change careers for lower pay, you’ll pay fewer taxes and keep more of what you earn.

Business expenses reduce income in the eyes of the IRS.

Employers reap most of these benefits instead of employees.

I will benefit more from the tax code now that I am self-employed.

The most significant tax deduction will be for our health insurance premiums.

Health insurance premiums for individuals and their dependents are a deductible expense for the self-employed.

That means, however expensive my COBRA insurance premiums are — and they’re not cheap — they will reduce our adjusted gross income (AGI), reducing our taxable income.

For example, if I pay $2,000 per month for health insurance for our family, the expense will reduce my taxable income by $24,000 (1040, Schedule 1, Self-employed health insurance deduction).

Furthermore, I have a SEP IRA for my business that I’ve contributed to over the past few years.

The SEP IRA allows self-employed persons to contribute up to 25% of adjusted net earnings, up to $66,000 in 2023.

Adjusted net earnings is a little confusing (this website explains it), so let’s call it 20% for this example.

If my business has profits of $100,000, I can contribute about $20,000 to the SEP IRA and reduce my taxable income to $80,000.

Add the health care premium deduction ($24,000), the standard deduction ($27,700 for 2023), and $100,000 in business profit becomes $28,300 of taxable income.

Business Profit $100,000

Health Care Premiums $24,000

SEP IRA Deduction $20,000

Standard Deduction $27,700

Taxable Income $28,300

We’ll also benefit from the Qualified Business Income Deduction and the Child Tax Credit.

Taxes may work in your favor or ease the transition if you change careers. Research your situation or talk to a CPA.

10. Retain Previous Experience in your Back Pocket

You can’t teach a recent college grad experience.

That gives mid-career employees an advantage in certain jobs.

It may also be true that you can’t teach an old dog new tricks.

But most skill sets don’t go away.

COBOL is a coding language that’s been around since the 1960s. It still takes part in calculating 95% of bank card transactions.

Colleges don’t teach it anymore, and no 22-year-old software engineer wants to touch it.

Someone with a COBOL background could leave their programming career to try something new. They can always go back to programming if the new gig doesn’t work out.

Certain fields move faster and require continuous training. But many soft skill sets — such as management, sales, teaching, communication, financial analysis, and customer service — never lose their value.

I spent 20 years consulting for a complex government organization and understand its information systems more intimately than most employees. My knowledge won’t disappear.

That’s a 20-year head start over any other potential hire. My previous employee understands this and will welcome me back any time.

I also left without burning bridges. My previous employer encouraged risk-taking, so nearly everyone I spoke to enthusiastically supported my new endeavor.

Not everyone will have that luxury. But no matter how catastrophic a career change may be, you can almost always return to a previous career.

11. Accept that Failure is an Option

Changing careers isn’t an action movie plot where failure is not an option.

When you envision what failure looks like, you can mitigate risks to prevent it.

I had to be OK with failure as a viable outcome before pivoting.

I used to think that failure was embarrassing or a sign of weakness. That view would influence decisions and hold me back.

I’ve modified my mindset to accept that failure is possible. But failing is better than not trying.

At some point, the fear of not changing careers began to outweigh the fear of failure.

That’s when I knew to move forward.

Analyze your situation to identify blind spots. Talk to friends and family to play out scenarios you hadn’t thought about.

We are not invincible. But a pragmatic approach that considers multiple negative outcomes will help steer away from failure.

12. Minimize Regret

Regret should be a more powerful motivator than failure.

Jeff Bezos, the founder of Amazon, famously said this about taking risks:

I think that’s probably true for all kinds of risks in life, not just for starting a business. Life is full of different risks. And I think that, when you think about the things that you will regret when you’re 80, they’re almost always the things that you did not do. They’re acts of omission. Very rarely are you going to regret something that you did that failed and didn’t work or whatever.

This quote from Bezos motivated me to leave my career and become a full-time writer.

The quote led me to an interview with Bezos recorded in 2008.

Bezos describes his decision to leave a lucrative Wall Street job to start Amazon through his Regret Minimization Framework.

I don’t aspire to a career or business anything like Bezos and Amazon.

But years from now, I would regret not changing careers when another option was at my fingertips.

Consider your situation using the regret minimalization framework to find clarity in your desire to change careers.

Featured photo via DepositPhotos used under license. The author is long CVX stock.

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

- Dividend Kings — 50+ stocks that have increased dividends for 50+ years.

- Monthly Dividend Stocks — List of 70+ stocks that pay a dividend every month.

- Dividend Champions — 140+ stocks that have increased dividends for 25+ years.