How to Prepare for the Next Crisis While Times are Good

Crises come around every so often — personal crises, family crises, national crises, political crises, market crises, and global.

The events are often predictable, but their timing is not.

Scientists predicted a virus such as COVID-19 could infect humans and cause severe health and economic consequences.

But no one knew the specific date, where it would start, or how the virus would spread and impact our world.

It’s hard to know what the next crisis in our lives will be. However, we can envision several scenarios that could push our personal lives into a crisis (illness, death, job loss, accident, a tree falls onto our house, etc.).

The next could be around the corner or years away.

The same is true for financial crises.

The Next Financial Crisis

We generally know what will happen when the next financial crisis arrives — the markets will tank.

It would be nice to be able to predict when or its cause. But no one can predict a crisis with precision.

The stock market reacts in real-time. Once investors collectively realize a crisis is at hand, the market falls fast. There’s little time to react when it happens.

The housing market is far less liquid, and crises are less frequent. Prices take time to adjust.

I learned this lesson the hard way during the last crisis, buying a condo after the local bubble started to pop (2006) but before the real damage (2009).

Discounted real estate opportunities remained for years afterward (see chart below).

Once the dust settles from market turmoil, there are often opportunities for long-term profits.

But you can’t sit around waiting for prices to fall. Markets rise more often than not, so you can’t afford to miss out on a decade of returns sitting on the sidelines.

Furthermore, it’s unwise to sell assets in preparation for a crisis because you can’t predict when it will happen.

Always be investing new money.

The key to positioning for the next crisis is first to ensure it doesn’t cripple you, then be ready to act on opportunities that may arise.

Preparing for the next crisis is a four-step process:

- Reduce Personal Financial Risk

- Build Cash Savings

- Identify Ideal Assets

- Continue as Normal (Wait)

If you’re serious about finding opportunities in crises, the time to start preparing is now.

Four Steps to Prepare for a Crisis

Never let a good crisis go to waste. — Winston Churchill

The housing crisis that started in 2007 presented many opportunities for those prepared.

I was not one of those people.

I overpaid for my condo at the front end of the financial crisis and spent the next few years with my pants around my ankles.

People like me couldn’t capitalize. Investors stretched thin with too much debt couldn’t capitalize either.

Those prepared bought discounted stocks and real estate investments that have risen in value ever since.

The four steps I’ve identified to prepare for the next crisis apply to the stock market, the housing market, alternatives, and even micro-markets in your community. This article focuses on stocks and real estate.

Here are the four steps with some detail. Think of these as good habits to always have in place instead of overnight action items.

1. Reduce Personal Financial Risk

The greater population always seems to be surprised when a financial crisis hits. Few prepare even though the next crisis is inevitable.

Merriam-Webster defines a crisis like this:

1) a difficult or dangerous situation that needs serious attention. 2) an unstable or crucial time or state of affairs in which a decisive change is impending — especially one with the distinct possibility of a highly undesirable outcome.

In finance, highly undesirable outcomes include losing money, losing a job, defaulting on debts, bankruptcy, and foreclosure.

Don’t ever leave yourself vulnerable to the unexpected. Expect the unexpected.

You can reduce personal risk in many ways:

- Maintain adequate insurance

- Regularly fund a savings account

- Pay off high-interest debts

- Keep debt payments low relative to income

- Save a lot more than you earn

- Invest conservatively

As income and wealth grow, debt often grows. We see this during prosperous times.

For example, if someone gets a raise then buys a larger home, they’ll have a larger mortgage payment.

That’s probably okay as long as they remain employed and employable in a healthy job market.

But if they lose their job, don’t have adequate savings, and can’t find a new job that pays a similar amount, the joblessness could create a new personal crisis — debt or mortgage default.

Broader crises can kickstart cascading asset prices and tightening labor markets.

Recent data from the Federal Reserve confirms debt is rising faster than wealth. In Q2 2021, household net worth rose by 4.3% over Q1, while household debt rose about 8%.

In part, this is due to very low interest rates and the current favorable markets. But as individual income grows, people are more comfortable with more debt.

When your wealth grows, you should aim to reduce your debts, not increase them. Reducing debt is important to be adaptable when uncertainty arises.

Avoid the temptation to borrow more as your wealth and income grow. If you borrow to invest in real estate, maintain a sizable cash hoard and keep your loan-to-value ratios conservative.

2. Build Cash Saving

You can’t take advantage of market imbalances without liquid cash.

Cash enables fast action. To rely on stocks, real estate equity, or crypto assets in a time of crisis is a gamble.

The last thing long-term investors should want to do is sell assets in a crisis.

Building cash savings is about more than an emergency fund worth three to six months of expenses.

Savings beyond your emergency needs is called an opportunity fund.

For a long time, I was a proponent of a minimalistic emergency savings fund, investing every spare penny I had. However, when I sold my rental condo in 2019, I deposited the cash proceeds into savings, where it remains.

Our high yield savings account is now much higher than a standard conservative emergency fund. And even though the “smart advice” would say it’s far too much cash, it’s still a small percentage of our net worth.

The savings makes us less susceptible to personal crises, and we’re poised to be opportunistic when turmoil returns to financial markets.

Inflation and currency risks remain. But even an inflationary crisis will require cash to purchase distressed assets.

3. Identify Ideal Assets

Always be investing, but also always be thinking about your next elephant.

In 2019, Warren Buffett talked about buying an elephant-sized company. With so much cash on hand, Berkshire Hathaway wants to find large acquisitions that meet their standards of high-quality, well-managed, cash-flow generating businesses.

But when prices are too high, the company remains patient and holds cash. Berkshire Hathaway holds about $150 billion in cash right now.

During the depths of the 2009 financial crisis, Buffett bought large stakes in Goldman Sachs, Bank of America, Mars, and Dow Chemical at rock bottom prices.

He could because he was patient and had billions in cash when the shit hit the fan.

What’s your next elephant?

It can be any income-producing asset.

My ideal asset is a single or multi-family rental property near my home that produces a decent cash-on-cash return.

A property meeting my target investment criteria does not exist today.

But if uncertainty were to disrupt our local housing market, there may be opportunities. If that happens, I’m ready to buy.

I’m also comfortable knowing the right property at the right price may never become available (or I’m too lazy to find it).

One stock investing strategy is to prioritize your favorite stocks and set “doomsday” price targets. When the market falls, deploy your purchase plan.

If you don’t buy individual stocks, set incremental buy orders for your favorite total stock market index ETF (mine is VTI) as the market falls from its peak. Buy at 5% down from the peak, then again when the market is down 10%, 20%, 30%, etc. — or however you like.

Save some “dry powder” for major declines (more than 30%).

This way, you’re not guessing what the bottom will be. You’re buying more stock as the market prices become more favorable.

I bought this way in March 2020, tweeting the thresholds during the COVID-19 stock market correction as the market fell 35% from its peak.

S&P 500 high:

3,393.52 (Feb 19th)Down 5% – 3,223.84 ✔️

Down 10% – 3,054.17 ✔️

Down 15% – 2,884.49 ✔️

Down 20% – 2,714.82 ✔️

Down 25% – 2,545.14 ✔️

Down 30% – 2,375.46 ✔️

Down 35% – 2,205.79 ✔️

Down 40% – 2,036.11

Down 45% – 1,866.44

Down 50% – 1,696.76$SPY #marketcrash2020— Craig Stephens | RBD (@RetireBeforeDad) March 23, 2020

You’re not going to time the market well. But knowing what you want to buy before the discount will help you prepare for discounts.

The point is to have a plan before the next crisis, so you’re ready when opportunities present themselves.

4. Continue as Normal (Wait)

Avoid waiting around for the next crisis or trying to predict it.

We all benefit from market prosperity. Life is better when the economy is stable, and stock and housing markets are growing.

Uncertainty from the next financial crisis will have serious consequences and repercussions. Hopefully, they won’t hit us directly.

But people will suffer.

Don’t hope for a crisis so you can get a good deal and make more money.

However, crises happen.

You can become a victim of the next crisis or position yourself to thrive in the recovery.

Invest month-to-month as though a crisis will never occur.

But on the personal finance side, reduce risk and increase your cash over time as if a crisis will occur. Cash is financial security.

As writer Morgan Housel put it, save like a pessimist, invest like an optimist.

Build and refine good financial habits every day to be more adaptable during uncertainty.

The Next Stock Market Crash

Big opportunities come infrequently. When it’s raining gold, reach for a bucket, not a thimble. — Warren Buffett

There will be another market crash.

Don’t sell stocks when it happens. Buy stocks.

Crises vary in severity.

In March of 2009, during the housing and financial crisis, the S&P 500 bottomed down 56.8% from its peak (October 2007).

In March of 2020, at the onset of COVID-19, the S&P 500 bottomed down 35% from its peak.

Each market crash presented an opportunity to buy stocks cheaper than before, but there was no way to time the market bottom.

Eleven years passed between those two significant market events.

Waiting around to take advantage of the next stock market crash is a loser’s game.

Consistent investing over time is a proven way to build wealth.

Employer plans such as 401(k)s or 403(b)s and IRAs are the most efficient ways to do this. Max them out.

You can also set up recurring investments through your broker. I invest $750 into my M1 Finance account every two weeks and another $500 a month into Fundrise (a real estate investing platform).

Investing equal dollar amounts into assets at regular intervals is called dollar-cost averaging.

When the market is high, you’ll buy fewer shares. When the market is low, you’ll buy more shares. Automatically.

While regularly investing, you can still prepare to take advantage of a stock market correction when it arrives.

- Diversify and avoid margin

- Slowly build an opportunity fund

- Buy more shares on the way down (at set increments, 5%, 10%, etc.)

The Next Real Estate or Housing Crisis

Some might call today’s real estate markets a crisis of affordability and housing shortages.

But let’s remember back the last financial crisis back in 2007-2009.

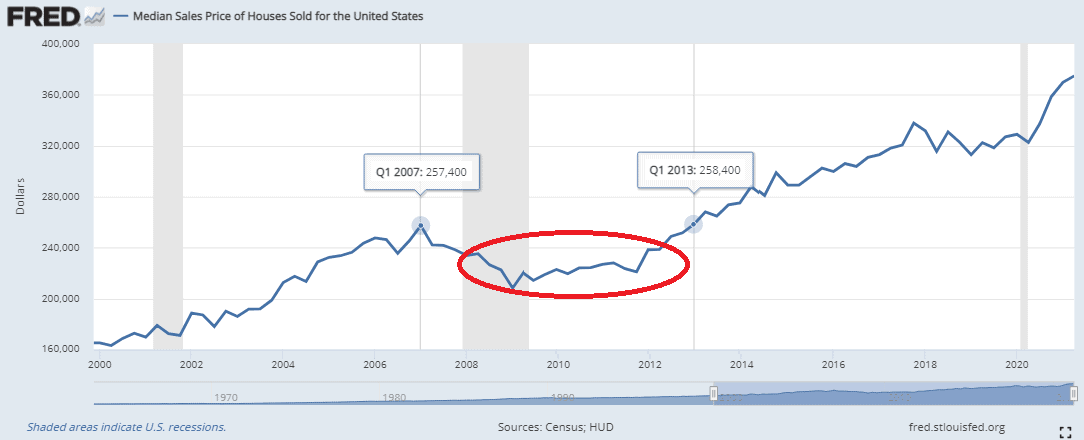

Housing was in a bubble leading up to the peak in Q1 2007. Once things started to go sour, home prices fell and accelerated downward when Lehman Brothers collapsed.

After the crisis, real estate became cheap relative to previous years. Median home sale prices in the U.S. took six years to recover.

Overleveraged investors were forced to sell properties to salvage their businesses. Homeowners who bought during the runup (myself included) were underwater and stuck.

Sloppy lending meant banks took much of the heat, accepting short sales to offload bad loans.

Deep discounts were abundant, especially in high cost of living cities.

People who tended to buy real estate either as an investment or home were already underwater from the crisis and couldn’t buy.

Only deep-pocketed investors and first-time homebuyers could take advantage of the very bottom.

At its worst, my condo lost about 20% of its value by 2009. I was in no position to be opportunistic. I was more likely to short sell.

But I was determined to turn things around. By paying off the second loan, refinancing, and holding onto my job, I pulled my pants up from around my ankles.

By 2011, Mrs. RBD and I rented the condo and bought our first home together, which has appreciated significantly over the past decade.

In a way, we were both victims and beneficiaries of the last housing crisis.

I’m not sitting around waiting for the next stock market or real estate crisis. But when it arrives, I’ll be better prepared.

Photo by Paul Skorupskas via Unsplash

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services right now:

Sure Dividend — A reliable stock newsletter for DIY retirement investors. (review)

Fundrise — Simple real estate and venture capital investing for as little as $10. (review)

NewRetirement — Spreadsheets are insufficient. Get serious about planning for retirement. (review)

M1 Finance — A top online broker for long-term investors and dividend reinvestment. (review)

I lived through Black Monday in 1987, Friday the 13th in 1989, the mini-crash in October 1997, the dot-com bubble of 2000, the 9/11 crash of 2001, the market downturn of 2002, the bear market and financial crisis of 2007-2009, the 2010 flash crash, the 2015-2016 stock market selloff and the 2020 Covid crash. I “lost” a huge portion of my investments in every one of these 11 financial meltdowns. Except I never ever sold a single share of anything and now I’m the wealthiest I’ve ever been. I expect to “lose” money several more times in the future as well.

The next crisis is always only a few year away. Since 2000, we have had the dot-com crash, sub-prime mortgage crisis, and COVID-19. There are have also been a myriad of smaller crises. Always prepare.

Such a timely article, I just wrote a piece of similar sentiment. You break it down just like I would with those 4 steps. I’m glad you brought up the best of both worlds as sitting and waiting for a crash typically just leads to disappointment.