Individual Stocks vs. Index Funds – Why I Own Both

Though opinions vary on individual stocks vs. index funds, my own investments reflect a blend of both, from dividend and growth stocks to index funds, ETFs, and managed mutual funds.

Though opinions vary on individual stocks vs. index funds, my own investments reflect a blend of both, from dividend and growth stocks to index funds, ETFs, and managed mutual funds.

My uncle gave me one share of Chevron for my 20th birthday in 1995, and I built an individual stock portfolio from there.

A retirement mutual fund portfolio spawned from my first job in 1998, and I contributed to employer tax-advantaged accounts until I left my corporate career in 2022.

As I approach my 50th birthday, I’ve been thinking about what I want my total portfolio to look like in 10, 20, and 30 years.

Its current state is not the future state.

For years, I bought individual stocks to build investment income via the dividend growth investing strategy. I targeted high-quality companies with a long history of paying and increasing dividends.

Unlike market fluctuations, dividend income is predictable. I like predictable, stable income streams. That’s what attracted me to dividend growth stocks for so long.

However, it requires picking stocks, and it is challenging to beat the market indexes over extended periods.

Most actively managed equity mutual fund managers can’t beat the market indexes. So why bother trying?

For most people, buying individual stocks:

- Is a lot of work

- For inferior returns compared to index funds

- With greater risk

When you’re unwilling to put in the research time, the risk of underperformance increases.

A decade ago, I’d spend many hours a week researching stocks. Stocks were an escape from a career I didn’t love.

But what I’ve found since leaving my corporate career is that I no longer want to spend time researching stocks. I prefer to work on my business, spend time with family and friends, and travel.

Yet, I still own a substantial number of individual stocks. So, I’m slowly simplifying my portfolio to reduce individual stock holdings and move money into mutual funds and ETFs.

Due to tax planning, the transition to an ideal portfolio state will take a decade or more.

Table of Contents

The Current State

Mrs. RBD and I have two Fidelity Roth IRAs, two Fidelity Traditional IRAs, a SEP IRA, a former employer-sponsored account, and two taxable brokerage accounts.

These accounts primarily hold equity index funds and ETFs but also individual stocks, bond funds, and a couple of managed mutual funds.

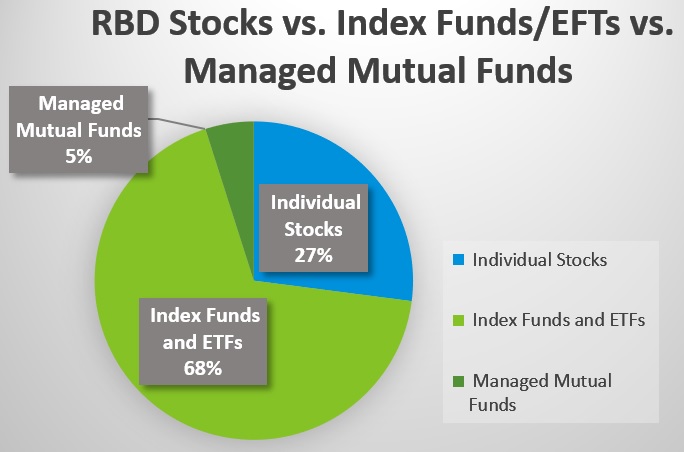

In 2018, I analyzed all our accounts to determine the allocation of individual stocks vs. index funds + ETFs, and managed mutual funds.

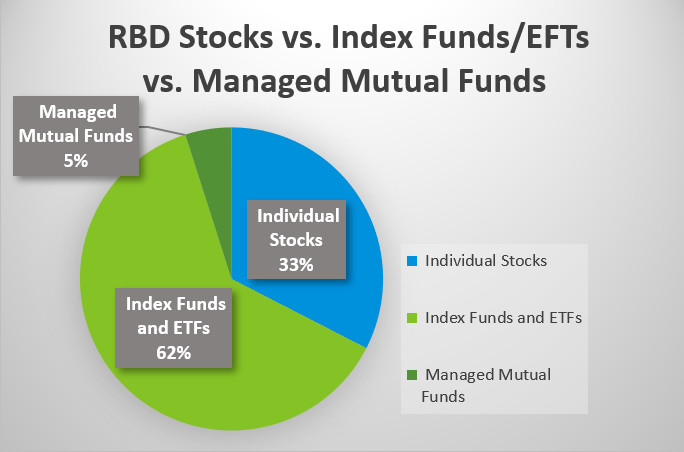

In October 2024, I analyzed our portfolio again. Here’s what I learned:

March 2018

October 2024

Since 2018, our individual stock holdings have increased as a percentage of our total portfolio, from 27% in 2018 to 33% in 2024.

This was surprising, as I’ve already started transitioning away from individual stocks.

I can think of a few reasons why my individual stock holdings have increased.

First, I aggressively bought individual stocks from 2018 into 2022. But I was also maxing out retirement accounts during that period, putting more money to work in index funds than individual stocks.

So why is there a greater allocation toward individual stocks?

During that time, our retirement accounts evolved from a 100/0 stock/bond ratio to 90/10. That decreased the index fund performance against the individual stock holdings.

I also bought small cap, mid cap, large caps, REITs, and international and emerging market index funds. Those have all underperformed domestic large-cap stocks. Most of my individual stock holdings are domestic large caps, which have risen with the tide.

I also dabbled in growth stocks. A few holdings took off since 2018, including Apple (AAPL), The Trade Desk (TTD), Meta (META), CrowdStrike (CRWD), and Costco (COST). I still own them all.

I bought plenty of losers, too! But these holdings surely contributed to the current imbalance.

Reasons to Buy Individual Stocks vs. Index Funds

I’m pro index fund, and I prefer them today over individual stocks.

So if you’re all in there, that’s great. The case for only investing in a handful of index funds and ETFs is very strong.

In my case, decisions I made years ago mean I’ll continue to hold individual stocks for years, and I’m OK with that.

The beauty of index investing is it requires very little research. Simply choose a few low-cost index funds with broad holdings and continually invest in them for the long term. Ride out the market fluctuations and don’t sell when it declines.

The low-cost nature and ease of investing in them has driven cash to Vanguard and Blackrock (iShares), now the two largest U.S. money managers.

However, investing in individual stocks still has advantages and is a valid strategy. Here are a few benefits.

Create a Portfolio of Reliable Income

This is why I spent years buying individual stocks. Owning dividend growth stocks is a way to build a predictable and sustainable income stream that is primarily passive after the initial research.

Choose stocks that historically pay and grow their dividends to earn income greater than the inflation rate. The key is to buy companies that are well-managed, have a competitive advantage, and are immune to economic cycles.

Index funds pay dividends, too, but the yields are low, and payment amounts are inconsistent. Some low-cost funds and ETFs focus on dividend-paying companies, and I like those too.

Just know that the comfort of perpetual income of dividend stocks may increase your taxable income and lower returns.

Own Only the Companies you Like

I have never owned two popular dividend growth stocks: McDonald’s (MCD) and Walmart (WMT). I don’t own them because I prefer to eat and shop elsewhere.

I’ll go to Target (TGT) or Costco (COST) any day over Walmart. If I don’t like the shopping experience, I should not own the stock (though I do own it indirectly through funds).

Investing in stocks individually allows you to choose the companies you like or don’t like. This is helpful for people loyal to a certain brand or invest based on their values (environment, religion, etc.).

Be careful of bias. You may have preferred shopping at Sears, but the stock was lousy.

Don’t Own the Companies You Don’t Like

Total U.S. market index funds own stock in all the publicly traded companies in the U.S. That includes the so-called vice stocks such as cigarettes, gambling, alcohol, and firearms stocks.

If you buy your stocks individually, you can avoid the companies you don’t want to own.

This topic has come to light in the aftermath of several school shootings. Some investors don’t want to own firearms stocks or those that negatively impact the environment more than other companies.

Potential to Outperform the Market

Investing only in index funds will underperform the markets by the expense ratio on your funds. For most investors, that is a very acceptable return.

By buying individual stocks on top of index funds, you’re likely to reduce returns and increase risk over several years.

However, you leave open the potential to beat the markets. But you’re unlikely to crush market returns with a diversified portfolio of dividend stocks.

I’m an advocate for using a small percentage of your portfolio (5% to 10%) for speculation to attempt to increase returns.

Speculative investments can be invested in growth stocks, options contracts, crypto-currencies, IPOs, venture capital, a business, or whatever floats your boat.

Taking bigger risks gives you the potential to outperform, something you are guaranteed not to get from indexing.

Young people, in particular, can afford to lose and may benefit from making a risky investment. This is especially worthwhile if you have some kind of advantage, such as a background in a certain profession or discipline that would make you privy to industry trends or a growing technology.

If you’re going to speculate, investing money or time into real estate or starting a business is a more controllable endeavor than picking stocks.

The mechanics of investing in stocks are simple and tempting, but picking the next Nvidia ten years before it explodes requires more luck than hard work.

Bet on yourself before betting on someone else.

Slightly Lower Cost

Depending on how you assemble your portfolios, you can save on fees through individual stock investing.

Individual stocks have no fees.

On the other hand, index funds and ETFs carry a recurring annual fee known as the expense ratio. The lowest-cost funds have an expense ratio of around 0.03%.

If you put $10,000 in a fund, the annual fee taken out will be about $3. As the fund value increases, so do the fees. You also may pay trading fees if you buy an index fund or ETF through an account that doesn’t provide free trades.

Stock ETF dividends are treated the same as individual stocks.

Mutual funds typically distribute capital gains more than ETFs, so aim to own them only in tax-advantaged accounts.

We’re talking small amounts here for beginners, so expense ratios are not a major ding on indexing. But low fees are one of the main arguments for index funds, and buying individual stocks is actually cheaper, especially as the numbers grow.

But the lower cost of buying and owning individual stocks can quickly be eroded by subpar returns.

Arguments Against Buying Individual Stocks

Yes, there are quite a few arguments against buying individual stocks. I’ll start with the obvious.

You are Unlikely to Beat the Market

It’s not impossible to beat the market as an individual investor. But it takes some skill and luck. Luck tends to run dry as investment horizons expand.

The time investment required to spend on research to beat the market year after year would probably detract from the quality of your life.

You can still try to pick a winning growth stock through speculation. Just keep your expectations low. You probably won’t win over the long term unless you pick one or two big winners and hold them for many years.

Emotional Bias

Emotions are the weakness of investors. Investing in stocks is the perfect forum for emotional bias. I like shopping at Costco, and the one near me is always busy.

Should that mean I buy the stock too? For me, it did play a part in my decision. I enjoy shopping there, but I researched the fundamentals and valuation, too.

Understanding bias and constantly playing devil’s advocate against yourself is crucial for investing in individual stocks. It can be tiresome.

Sometimes, bias is impossible to avoid because it’s subliminal. A pure index fund strategy, through thick and thin, avoids any ill-placed bias that could harm your returns.

Higher Risk

Since there’s no way you’ll individually own as many stocks that are in a broad total market index fund, your individual stock portfolio is at greater risk of volatility.

Severe declines due to a bankruptcy, a Lehman Brothers-style catastrophe, or something unknown today would have a greater impact on your portfolio as a percentage of the total portfolio compared to a broad index fund.

Not Good at Picking Stocks

If you have no experience and haven’t read any books on investing in stocks, you won’t choose good stocks.

Following the advice of an adviser could help you, but the fees will offset gains. Alternatively, you can heed the advice of TV personalities or subscribe to a stock newsletter, but if you don’t know what you’re doing, it will eventually catch up to you.

I recommend a few stock newsletters for those who already own individual stocks and need to keep tabs on them or are looking for alpha via growth stocks.

Don’t Have the Time

Simply put, if you don’t have the time to research and select stocks, don’t invest in individual stocks. Without research, you will not perform well. Go with index funds instead.

Taxes on Dividends

Index funds, ETFs, and some individual stocks pay dividends. When paid a dividend, that money is taxed. Most dividends are qualified, meaning they are taxed at the long-term capital gains rate of 15% for most people.

If you’re allergic to taxes, use a traditional IRA or Roth for your dividend investing. Or buy non-dividend paying stocks in a taxable account.

For tax efficiency, ETFs are a better option in a taxable account than mutual funds because they pay out fewer capital gains.

Still, ETFs usually pay a dividend, which is subject to tax in a non-retirement account.

Even if You can Beat the Market, it may not be Worth the Time

The S&P 500 was up 26.29% in 2023, including dividends. If you spent countless hours researching stocks and your returns beat the market by 2%, was the time worth it?

If you are going for total return, trying to squeak out an extra percent or two will take up a lot of your time that could be better spent enjoying yourself.

Conclusion — Individual Stocks vs. Index Funds

This blog started primarily as a stock investing website. Now, I write more about broader investing and personal finance themes. I enjoy writing about these topics more than stock analysis, and they appeal to a wider audience, bringing more readers to RBD.

Mutual funds have been at the core of my retirement savings since I started my career in 1998. At Fidelity, I have all the funds and ETFs I need to create an age-appropriate portfolio using the minus-your-age rule of thumb.

However, individual stocks will remain a part of my strategy for years, even as I reduce my holdings and simplify my portfolio. I enjoy the dividend income, but I recognize I’ll want to spend less and less time researching stocks as I age.

Instead, I can utilize dividend ETFs to lower my risk while continuing to earn dividends. Or convert stocks to low-dividend ETFs to reduce my tax burden and likely increase long-term returns.

What’s your opinion on individual stocks vs. index funds?

Photo credit: PublicDomainPictures via Pixabay

Disclosure: Long all investments mentioned in this article.

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

- Dividend Kings — 50+ stocks that have increased dividends for 50+ years.

- Monthly Dividend Stocks — List of 70+ stocks that pay a dividend every month.

- Dividend Champions — 140+ stocks that have increased dividends for 25+ years.