Financial Confidence is the New Financial Independence

The FIRE movement made the rounds in national news for a few years and still gets a head nod here and there.

The FIRE movement made the rounds in national news for a few years and still gets a head nod here and there.

The early retirement (RE) part of FIRE always received more criticism because it’s the goal when someone doesn’t like their career choice and wants to escape.

In hindsight, this was me.

Both financially and in terms of professional fulfillment, you’re better off finding a career from which you don’t want to retire.

Financial independence (FI) is harder to argue against. Building enough wealth to enable bold life choices and financial freedom is a healthy goal.

Get there by earning more, spending less, and investing the surplus.

The main criticisms of financial independence are its accessibility and how long it takes to achieve it.

Starting from zero, it takes at least a decade to reach a minimum level of FI, and realistically longer — especially lower-wage earners, who may never achieve it.

But there’s another way to look at wealth and money. One that’s accessible to everyone, doesn’t take as long, and still adheres to the foundational principles of FIRE.

Instead of focusing on financial independence, strive first to strengthen your financial confidence.

Table of Contents

What is Financial Confidence?

Financial confidence is clarity in managing your finances and making informed decisions on the path to achieving long-term financial goals.

It’s a blend of knowledge, emotional resilience, and planning. It empowers people to navigate financial challenges and seize opportunities without stress or hesitation.

Furthermore, it’s the belief in your ability to manage, save, and invest your money without fear or uncertainty, using available tools to help track finances and inform decisions today and throughout our lifetimes.

There are several benefits to building financial confidence:

- Achieve it more rapidly than financial independence.

- More confidence reduces financial stress and anxiety.

- Better financial footing improves relationships.

- Strengthens capabilities to handle uncertainty.

- Encourages continuous learning.

- Leads to financial independence and wealth.

The most significant advantage of financial confidence over financial independence is its available to everyone who is willing to learn and inject financial discipline into their lives.

We can pursue higher-level long-term goals and meaningful wealth with confidence as a foundation. Financial confidence is the first step toward financial independence.

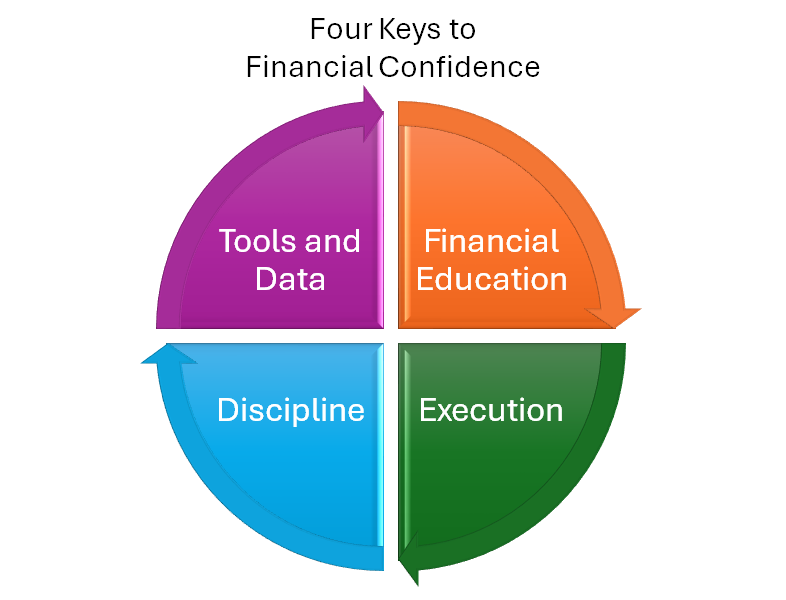

Four Keys to Financial Confidence

Financial confidence is more challenging to define than financial independence.

Financial confidence is more challenging to define than financial independence.

Confidence should not be confused with arrogance. High-income earners or trust fund beneficiaries may be confident because they are or feel wealthy. That’s not what I’m talking about in this article.

Financial confidence is for everyone. It’s about maintaining control over your finances and emotions and eliminating fear and trepidation with knowledge.

Those who have it stay disciplined and use data for decision-making so they can grow wealth and handle adversity or uncertainty when it inevitably arrives.

Here are four keys to unlock financial confidence.

Financial Education

The more you learn and study about money, the more confidently you can manage it. I take this for granted because I was a student of finance from an early age, earned a Finance degree, and continue to learn and teach it today.

The more you learn and study about money, the more confidently you can manage it. I take this for granted because I was a student of finance from an early age, earned a Finance degree, and continue to learn and teach it today.

Parents who teach kids about money raise more responsible adults. But not everyone has the luxury of financially savvy parents.

Financial education in our schools has improved over the past two decades, but it’s insufficient.

External groups like Junior Achievement and Scouting organizations supplement the education system with real-life skills that are not prioritized in public middle and high schools.

But into adulthood, financial education rests solely on the individual.

Financial educators share their knowledge in books, blogs, business news, community college courses, online courses, or wherever people consume information. Education resources are abundant if we can focus amid life’s infiltrating distractions.

Financial education is the foundation of financial confidence, empowering us to execute critical decisions about our wealth.

Execution

Money-smart people sometimes know what they’re supposed to do but hesitate to act on what they’ve learned.

Money-smart people sometimes know what they’re supposed to do but hesitate to act on what they’ve learned.

For example, a financially savvy person may know they should be investing more in the stock market but don’t increase their employer contributions for fear of a market crash.

Or they know they should complete an estate plan but aren’t sure where to start, so it remains a perpetual to-do list item.

They know that a lump sum of cash in a low-yield checking account would be better invested elsewhere, but selecting the right brokerage, ETF, or high-yield savings account is an overwhelming roadblock.

Retirees acknowledge they can afford to spend more freely in retirement but cannot let go of their frugal ways.

Financial knowledge is only useful if you execute what you’ve learned. Contribute more, finish the estate plan, buy the ETF, and enjoy what you’ve earned. But avoid the behavior pitfalls that can derail your previous smart money moves.

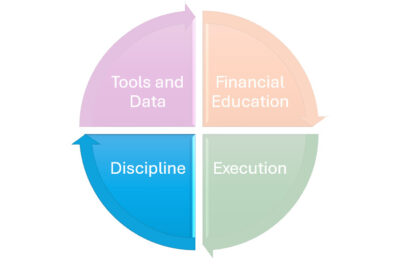

Discipline

All the knowledge on the internet cannot overcome the lack of financial discipline.

All the knowledge on the internet cannot overcome the lack of financial discipline.

I recently communicated with a new reader who said he was “smart at math but historically dumb with money”.

His “dumb with money” problem led to credit card debt and high interest payments, even though he understands the putrid consequences behind paying 29% on an impulse purchase.

High income doesn’t guarantee wealth, just as low income isn’t a life sentence for poverty.

Even the ultra-wealthy go bankrupt because of arrogant spending or unthoughtful borrowing. Who can resist the temptation of a private yacht once you’ve finally made it?

Keeping what you earn and growing and preserving assets builds long-term financial stability and wealth.

Behavioral reactions to market fluctuations, poor spending habits, or boneheaded purchases can unravel years of good decisions or the advantages of a high income.

Financial tools and data can help us maintain discipline as we navigate economic changes and market volatility.

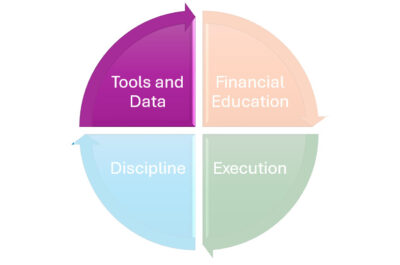

Tools and Data

We should all strive to run our household financials like a business, building a strong balance sheet, diversifying income sources, and maintaining healthy cash flows.

We should all strive to run our household financials like a business, building a strong balance sheet, diversifying income sources, and maintaining healthy cash flows.

Since data informs decisions in business, we should also use it to make daily decisions about our family finances.

Financial data comes in many forms, like bank and credit card statements and online access to brokerage accounts.

Spreadsheets are the rawest and most customizable tools.

But too often, Frankenstein spreadsheets become a time suck when we could be using our efforts to extract valuable insights from better, existing tools.

I still use spreadsheets, but I’m gravitating toward exclusively using software tools to make data-driven decisions. These provide structured input and output formats relevant to everyone’s needs and aligned with tax laws and financial planning standards.

Here are the tools I’m using and recommending now:

- Boldin (review) — Boldin calls itself the “financial confidence platform” and was the inspiration for the title of this blog post. It’s powerful DIY financial planning software to get smart about your money today and into the future. It recently rebranded from NewRetirement. Try it free for 14 days.

- ProjectionLab (review) — A DIY financial planning platform that takes inputs and projects forward-looking visualizations to help us plan and decide.

- Lunch Money — A simple desktop budgeting app that is better than Mint ever was, without all the ads. The first month is free.

- Empower — Free net worth calculator and portfolio tracking account aggregator. Still recommended, but past its glory days.

The first three on this list are paid products offering full-functioning free trials of varying lengths.

Boldin and ProjectionLab are similar tools with familiar visualizations. Boldin is a more linear experience, while ProjectionLab has a more modern look and freestyle approach. Boldin lets you connect to external accounts, while ProjectionLab relies on manual inputs (which some may prefer).

Unfortunately, the “freemium” models deployed by the now-defunct Mint.com and still used by Empower are masked as lead generators. Mint went under, and Empower has become frustrating to use, proving that free is not always a sustainable model.

Most consumers are accustomed to paying for services like newspaper subscriptions to get a cleaner experience without becoming the product themselves.

Financial tools have gone in that direction, too. I prefer to pay a small amount per year to get extraordinary value out of financial tools.

The products above cost $9-$12 per month, or $108-$144 annually, which is about the cost of a fancy dinner with a spouse or friend. But these provide tremendous feedback and data to help drive financial decisions about spending, investing, and drawing down retirement assets.

Use financial tools and data to guide you and deepen your financial know-how.

Conclusion

Financial confidence is the new financial independence.

While financial independence remains a desirable goal, it can seem distant or unattainable for many. It can also be elusive and come and go as the market fluctuates.

On the other hand, financial confidence is an achievable state of mind for anyone willing to learn, implement best practices, and continuously refine their knowledge. Though personal finance can be humbling, tools can help you stay sane and balanced along the way at a fraction of the cost of professional advice.

It empowers individuals to make informed decisions, handle financial challenges with clarity, and ultimately build a path toward financial independence and sustainable wealth.

Featured photo via DepositPhotos used under license.

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

- Dividend Kings — 50+ stocks that have increased dividends for 50+ years.

- Monthly Dividend Stocks — List of 70+ stocks that pay a dividend every month.

- Dividend Champions — 140+ stocks that have increased dividends for 25+ years.