How to Manage Excess Cash Flow

In personal finance, excess cash flow is the money that’s left over in your checking account at the end of each month. Your success with money is heavily dependent on creating and doing smart things with it.

If you don’t have any excess cash flow, you may need to change shit up.

Each of my quarterly updates is about what I’ve done with excess cash flow for the previous three months. With this money, I build income streams to increase the amount of investment income I earn passively.

Eventually, after years of investing and compounding, my investment income will cover my essential living expenses so I can live life without the constraints of time or money.

Here at RBD, we also teach that you should invest first, and invest often. You can invest via employer-sponsored retirement savings, college savings, and invest whatever is leftover at the end of the month into taxable accounts.

Most of us have a checking account from which we pay bills and save. But for the past decade, many have ignored the use of money market accounts because the rates were so low.

Online high yield savings accounts are paying less than half a percent. Since ACH electronic transfers between banks are free, you can earn extra money from interest on your cash savings with a few clicks.

This article lays out how I manage my excess cash flow each month using both my checking and money market account.

Below, I’ve also included a visual diagram of how the money flows.

The Checking Utility

A checking account is the most useful utility for managing your budget and finances. Money comes in, money goes out.

Checking accounts allow for unlimited transactions both ways.

They are great for writing checks, paying bills electronically, and transferring money. And they often free as long as you meet the stated minimums.

However, with savings and money market accounts, you are limited by law to six withdrawals per month.

Like most of you, my checking account has dozens of transactions per month. My paycheck is deposited to it twice a month, then I use it to pay utility bills, our credit card, preschool tuition, and our mortgage.

I always start and end the month with the same amount of cash… $2,000.

Then at the end of the month, I take the end balance and minus $2,000. That equals my excess cash flow for the month.

The $2,000 stays in the checking account for the next month, and I transfer the excess cash flow to my money market account. From there, I invest.

If I end the month below $2,000, that means I spent (and invested) more than I earned. In that case, I transfer from savings back into checking to equal $2,000 to start the month again (this sucks when it happens, but doesn’t much anymore).

Why $2,000? Because that’s enough to cover any expenses before my first paycheck and keep the account minimum to avoid fees.

Your number may be different. Just keep it away from zero.

New Money Market Account

I use my money market account as my general savings/emergency fund, car savings fund, and vacation fund. While my money is parked there, it earns 1.85% (as of 08/20/18). That’s better than a lot of dividend stocks and risk-free.

I’m only allowed six transfers out of the account per month, so I still use checking as my primary cash flow management account. I use the six withdrawals to move money back to my checking when needed or to transfer funds to my investment accounts (usually Fidelity or M1 Finance)

My savings was previously separated into four accounts (the three above, plus one for my condo rental) with Capital One 360 (formerly ING Direct). But I’ve recently left Capital One 360 for a number of reasons, most of all the stagnant interest rate.

I’ve since moved my money to a high-yield savings account, and I have two money market accounts now instead of four to simplify things and eliminate a few tax forms. The main one is a joint account for all of our personal savings goals combined. Then a separate account for the condo rental (reserves and security deposit).

Switching to a higher-paying bank yielding greater than 2.00% nearly doubles the amount of interest I’m earning every month which will give me a needed boost in my next quarterly income report.

The higher rate is more important to me now because I’m planning to increase our emergency and vacation fund this year. I’m also building a new car fund with $200 per month to be tapped in four years when our oldest car turns 10.

Click here to compare high-yield savings and money market accounts.

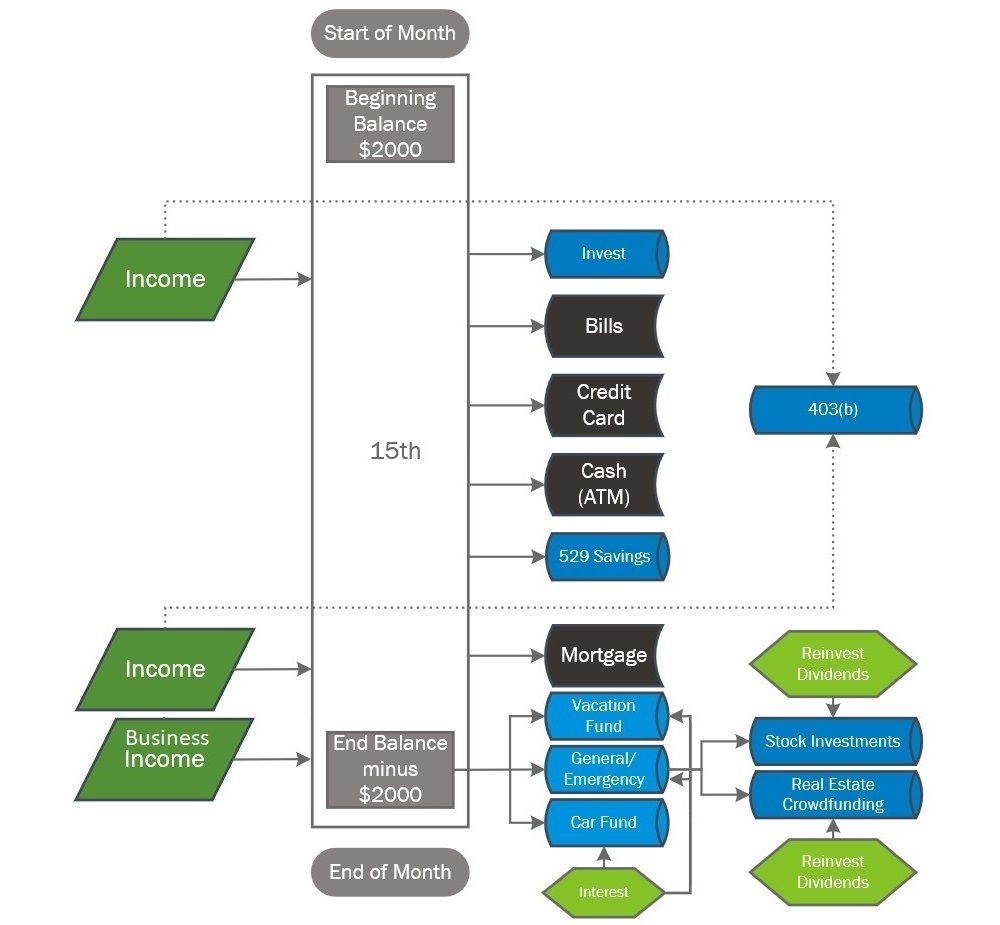

Visualizing Monthly Excess Cash Flow

To better understand how my money flows, I had some fun creating the diagram below. It represents a typical month. Green is income. Black is an expense, and the blues represent savings and investment.

What comes out of the gray box at the bottom is our monthly excess cash flow.

I start each month with $2,000 in the bank. On the left side is my salaried income from my nine-to-five job. Retirement contributions are immediately deposited to my 403(b). I did not depict taxes or miscellaneous withholdings for this diagram.

Throughout the month, I may invest early with available cash, then I pay utility and credit card bills. We also take out cash for miscellaneous spending and invest in our kids’ VA 529 accounts every month.

At the end of the month, I draw from my business income checking account for the month, then an automated payment is made to our mortgage company.

From the month’s end balance, I subtract $2,000 for the next month and transfer what’s leftover to the money market account.

I have a simple Excel worksheet that segments the savings into Vacation, Car, and General Savings funds. I use this to track each amount instead of separate savings accounts.

Any time I make an investment in stocks or real estate crowdfunding, it comes from the General Savings fund. This fund can also be used to pay extra on any student loan or personal debt if you have any.

Interest pays into the money market account, which I proportionally segment into the sub-accounts in my spreadsheet. Dividends from stocks and real estate crowdfunding reinvest.

Conclusion

This monthly cash flow diagram is how I’ve been operating our personal finances for years. Not until this week did I ever think about it visually. Other bloggers have done similar exercises and readers seem to always be interested in how real people manage their money.

This diagram isn’t perfect by any means. Months vary and money doesn’t always flow through to savings or investing as much as I would like.

But overall, I think it’s a good depiction of how I manage money and excess cash flow.

The key is to understand where your money goes. People often complicate their finances and it makes things harder to track.

Simplifying your finances is one way to help. You can also use a free money management tool such as Empower or Mint.com to view all of your money in one place.

Photo credit: StartupStockPhotos via Pixabay

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

- Dividend Kings — 50+ stocks that have increased dividends for 50+ years.

- Monthly Dividend Stocks — List of 70+ stocks that pay a dividend every month.

- Dividend Champions — 140+ stocks that have increased dividends for 25+ years.