M1 Finance Review 2024: A Top Broker for Long-Term Investors

This M1 Finance review was last updated on 01/01/2024.

We recently witnessed significant disruption in the online brokerage industry — a waterfall of competitive positioning and change. Nearly all online brokers are now commission-free

Robinhood was the original disruptor who started this whole thing and amassed a few million accounts. Then M1 Finance predicted the rest of the brokers would drop commissions when it eliminated all stock trading fees for investors.

Soon after, Webull copied the Robinhood app-only model. Now the three smaller commission-free brokerages got what was coming to them, a competitive landscape that puts the small-time investors like you and me in the driver’s seat.

While the big brokerage houses scramble to diversify their revenue sources, M1 Finance has reinvented its platform to be more than just an online broker. It’s now operating as a bank and lender too.

To cover all the new features, I’ve updated my M1 Finance review to included all-new screenshots, updated views of my portfolio, and added more details on M1 Spend and M1 Borrow.

The company has become a one-stop shop for consumer finances.

Table of Contents

M1 Finance Review 2024

I’ve invested on the M1 Finance platform since November 2017. M1 Finance is my favorite brokerage for beginner investors because it’s more intuitive than the traditional brokerage model.

It’s the best broker for dividend reinvestment.

That’s because instead of building your portfolio brick by brick, one stock or fund at a time, you design your ideal portfolio first, then fund it over time according to your design specifications. You can make adjustments on the fly.

The platform is designed for long-term investors, not traders. We should all have a long-term mindset, and M1 Finance helps to keep us focused on our overall portfolio instead of individual holdings.

It’s the perfect place to dollar-cost average (DCA) into both individual stocks and index ETFs because automation is built into the platform.

M1 Finance almost single-handedly rendered DRIP investing (dividend reinvestment plans) obsolete. If you still have DRIPs with a transfer agent such as Computershare, it’s long overdue to transfer them out.

You can start investing with M1 Finance with just $100 dollars. It’s available for both desktop and mobile app.

For the record, my primary brokerage is Fidelity because that’s where my employer-sponsored accounts are and where my retirement accounts have been for two decades. I’m comfortable there and have no plans to transfer those accounts to M1 Finance.

I use M1 Finance to replace the DRIP investing that I did for 20+ years.

Utilize employer-sponsored plans first. Open a separate account if you don’t have an employer plan, or don’t like the brokerage. If eligible, use an IRA or Roth IRA before investing after-tax dollars in stocks or ETFs.

This M1 Finance review is broken up into three main sections: M1 Invest, M1 Spend, and M1 Borrow. At the end, I’ll also share some updated screenshots from the smartphone app.

M1 Finance Invest Review

A Note about Dollar-Cost Averaging

Dollar-cost averaging is when you invest small amounts of money into an investment on a consistent basis. I believe this is the best strategy for beginner investors because it’s an easy way to get started (often the biggest challenge).

When I was getting started investing, I didn’t have a lot of money. Sometimes, I only had $25 or $50 to invest. I used the Chevron DRIP program to DCA back in the day.

Newbies sometimes think it’s not worth investing such small amounts. But it is worth it. And this whole commission-free cascade makes it simple and inexpensive to do.

Notably, there’s been some recent studies supporting dollar-cost averaging compared to a “buy the dip” strategy.

However, there’s a longer-standing opinion popular in the FIRE space that advocates against dollar-cost averaging. Bear in mind, the criticism against DCA is about dollar-cost averaging a lump sum over time vs. immediately investing the lump sum. If you have a lump sum, it’s best to invest it all.

Dollar-cost averaging, for this discussion, is when you invest consistently from your monthly excess cash flow, not from a lump sum. M1 Finance and most brokers make this easy by enabling regular draws from your bank account.

For the past several months now, I’ve had an automatic bank account draw of $500 that goes directly into my M1 Finance portfolio, in addition to the reinvested dividends. More on that later.

How M1 Finance Works (Easy as…)

M1 Finance was started in 2012 by a 25-year-old Stanford graduate named Brian Barnes. He couldn’t invest the way he wanted to on existing platforms. So he created his own and assembled a team of experienced securities industry executives to launch it.

Instead of a traditional brokerage where investors buy and sell and pay a commission for each trade, M1 Finance has you create “Pies”. A Pie is simply a group of individual stocks or ETFs. They use pie charts to display the portfolios.

With Pies, you choose your investments as “slices”, then allocate a percentage of your total portfolio toward each slice.

When you deposit cash into your account, the platform automatically allocates your money based on how you’ve set up your Pie.

Here’s a brief introduction video:

Customizing Your Pie

You can build your own portfolio from scratch, adding as many stocks or ETFs as you like. Or create several sub-Pies if you choose, and add those to your main Pie portfolio.

When you add a stock or ETF to your Pie, you choose what percentage you would like each slice to be.

When you deposit money to your account, it’s used to purchase the stocks and ETFs that balance the percentage allocations set in the Pie.

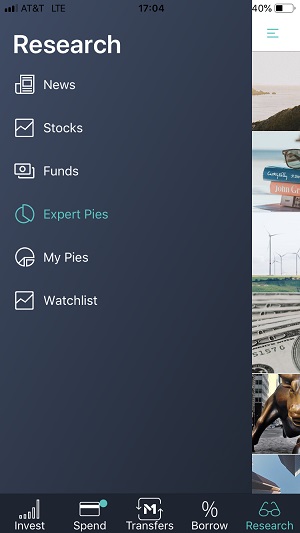

The Discover tab empowers you to search and filter to find the right stocks or ETFs (more than 1900 ETFs available at the time of writing). Or choose from Expert Pies crafted to meet particular goals or investment themes, including income earning, socially responsible, and industry or sector following portfolios.

Chose your perfect strategy and modify it any time you wish.

To keep costs low, M1 Finance utilizes batch trading, meaning that all its trades are executed in a big batch transaction once a day. The company told me that customers frequently request a second trading window and M1 working to add it to the functionality.

Fractional shares are OK. Because of the batch processing, this is not a platform for day traders.

M1 Finance is not a robo-advisor. However, the platform intelligently rebalances your portfolio every time you deposit money. Or you can rebalance your portfolio at any time with the click of a button. You can add or remove investments as you please.

There’s also a built-in Tax Minimization feature which chooses the highest cost share lots when you decide to reduce a holding from the Pie (sell), ideal for tax-loss harvesting.

Learn More How M1 Finance Works

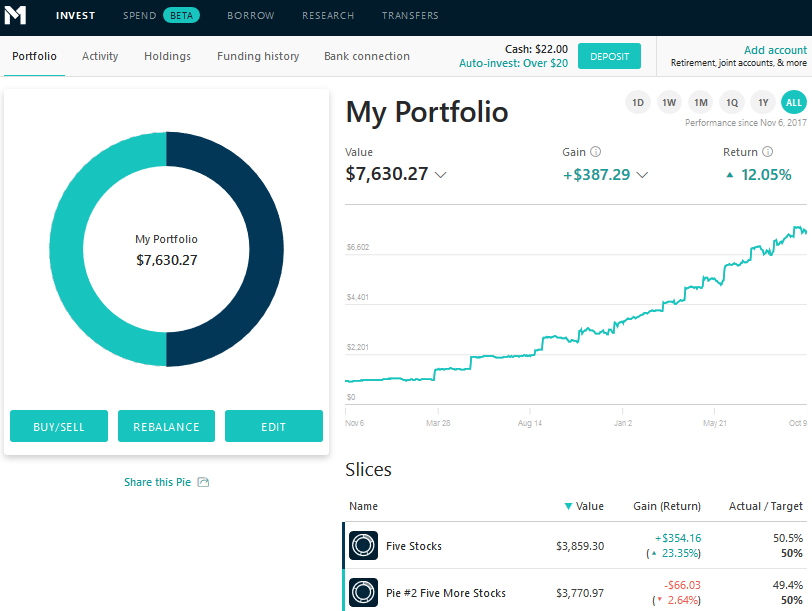

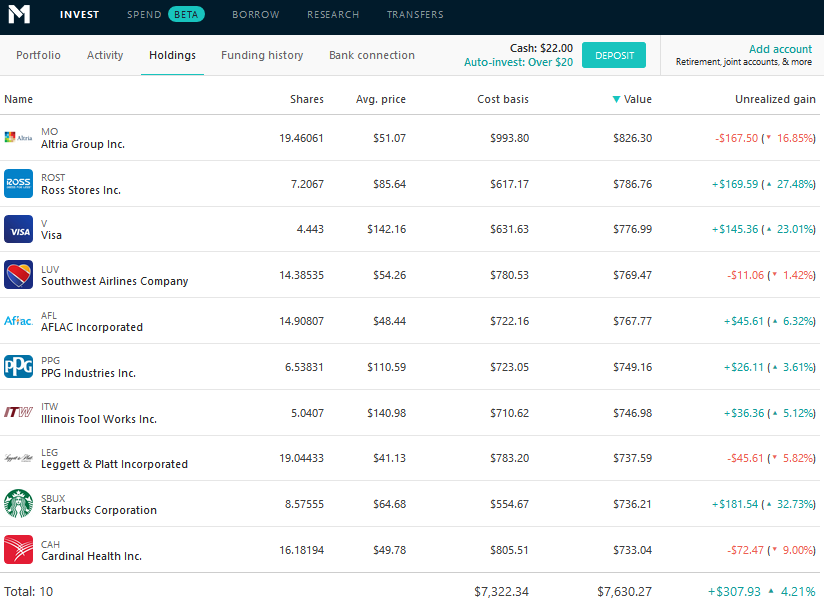

My M1 Finance Review Portfolio

M1 Finance uses pie visualizations to help investors better understand their investing strategy. I’ve created two separate Pies of five stocks each. Each Pie is 50% of my total portfolio. Each “slice” of each Pie is 20% of the Pie.

So I own ten stocks, each making up 10% of my total portfolio.

I chose the stocks based upon being long-term dividend growth oriented companies with low volatility. I’m comfortable buying shares at any price. As I dollar-cost average into the stocks, the price doesn’t matter to me as long as these companies remain on solid footing.

My M1 Finance account is an individual account. Other supported account types include Joint, Traditional IRA, Roth IRA, SEP IRA, Custodial, LLCs, Corporations, and Partnerships. M1 Finance accepts transfers from outside individual brokerage accounts, IRAs, and 401(k) rollovers.

Here’s the Portfolio view:

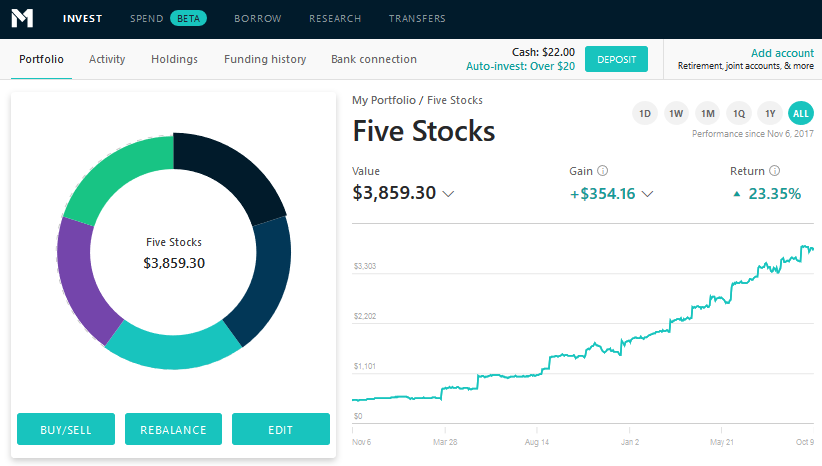

Here’s the first Pie called Five Stocks. This is the original Pie I put together in November 2017, slightly modified since then. Returns are as of 10/09/2019.

Notice how the Altria (MO) stock is down, but still makes up 21.4% of the portfolio. That’s because it’s fallen since I put it in my portfolio, and therefore, the algorithm purchased more of it every month. This recent month, the stock has recovered, raising its allocation in my portfolio.

The next time I make a purchase, the algorithm will buy more SBUX and CAH and probably very little MO. It’s always buying the stocks that will balance your portfolio as allocated.

Returns in this view are “money-weighted“, which takes into account all individual cash flows in and out of a portfolio. The Holdings view below shows returns before dividends based on the cost basis and current prices.

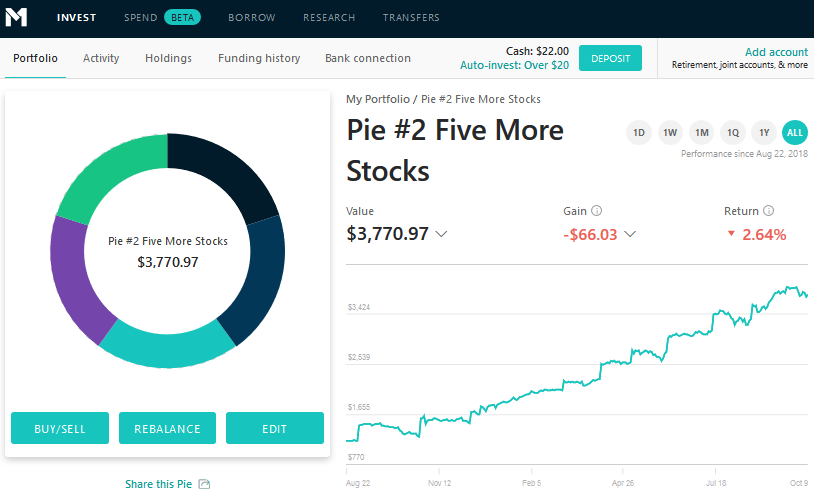

Here’s the second Pie I call Pie #2 Five More Stocks. I started this portfolio in August 2018, and it’s down since then, though not significantly.

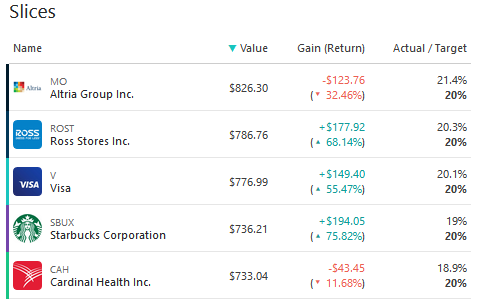

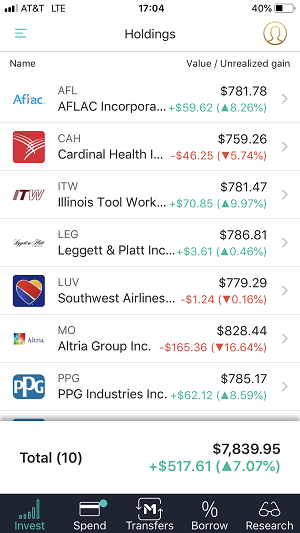

Below is a more familiar-looking Holdings view. Here you can see the number of shares of each holding, the average price, total cost basis, current value, and gain or loss.

What Happens When You Deposit More Funds?

With M1 Finance, you can add new funds ad hoc or automatically on a set schedule. This is perfect for dollar-cost averaging, and they’ve made it super easy. Schedule new deposits weekly or monthly on any day.

Automatic rebalancing is built into the platform.

Every time new money is deposited into the account either through new deposits or dividends, the platform will direct those funds appropriately into underweighted slices. This brings the underperforming slices up to the set allocation levels of the Pie.

As the size of each slice changes over time due to normal market drift, the investments remain properly balanced through this automation process.

You can always modify the Pie allocations or add new stocks or remove slices.

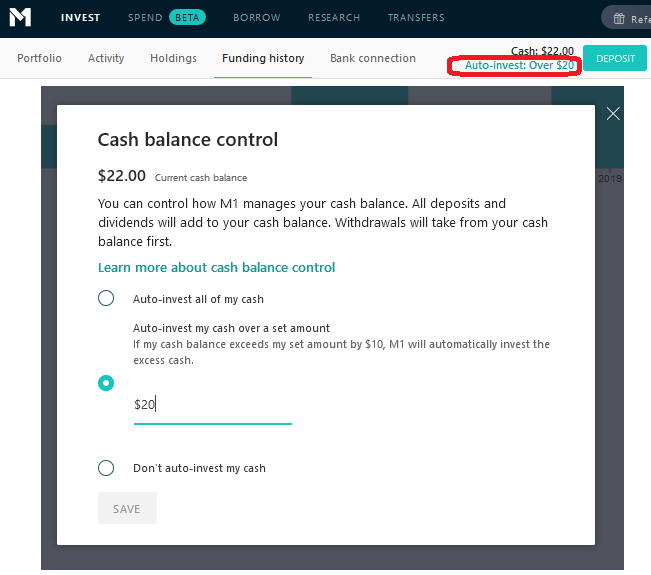

You must hit a minimum threshold of $25 in cash before the next batch purchase. This number increased from $10 in 2020 to lower company costs. I prefer the higher threshold because it means fewer transactions.

For example, if you receive a $5 dividend, it will sit idle until you receive another $20 or more in dividends or deposits. Once it hits $25, the purchase is made according to your allocation.

There are a few options to manage your cash, including a setting to turn off automatic investments. Or, you can set a minimum amount before auto-investing. Do this here:

I’ve set mine to $0. So once my cash balance hits $25, it invests $25, leaving $0. I’d prefer to be able to control the $25 number. I’d like to wait until the $100 threshold to invest my idle cash. But this adjustment doesn’t exist.

Depositing new money does not completely rebalance your Pies. If you keep adding money, no sales will take place. A sale will only occur on a full rebalance or when you remove a holding from a pie.

To initiate a manual rebalance the portfolio, you simply click the Rebalance button then confirm. You can rebalance at the Portfolio level or Pie level. Please keep in mind that any time you rebalance a Pie or your portfolio, you will generally be initiating a series of buy and sell transactions. Usually, every security sale has a tax effect, which may be a gain or a loss.

I don’t recommend rebalancing unless you are making drastic changes to your portfolio. Adding new funds will automatically rebalance over time.

Can You Buy or Sell Individual Holdings on the M1 Finance Platform?

As of April 25th, 2018, yes, M1 Finance customers can now buy and sell individual securities within your portfolio or add money to specific Pie.

You can choose to buy or sell an individual stock or pie piece outside of your regular allocation. They’ve designed this feature to be smooth and easy. Just click the button and make your selection.

After you’ve bought or sold an individual position or Pie, subsequent deposits will be allocated to your portfolio’s percentages in the normal way. So if you add $1,000 to an individual stock, the other holdings in the Pie or Portfolio may take a while to catch up. New deposits are always put toward bringing the portfolio back to the selected allocations.

What Happens When You Remove a Holding or Withdraw Funds?

When you eliminate a holding from your Pie, the system sells the security during the daily batch processing. You’ll see the slice of the Pie go away. But in the background, the platform makes a normal sale where the cost basis and proceeds are reported to the IRS.

The M1 Finance platform has also built in a Tax Minimization algorithm to your account. Here’s how it works.

The system uses a lot allocation strategy when selling securities to help reduce the amount owed on taxes… automatically.

When you request a withdrawal from your account, the algorithm knows which securities to sell based on your allocation percentages. Then instead of using the normal FIFO (first in, first out) order of sale, the algorithm prioritizes the sale of lots like this:

- Lots that do not result in a tax liability

- Lots that result in long-term gains.

- Lots that result in short-term gains.

This helps to minimize your tax liability when removing a holding or withdrawing money. But this should not be confused with tax-loss harvesting that you’ll find at brokers that call themselves robo-advisors.

One thing to keep in mind with an investing platform like this is the more active you are, and the more changes you initiate, the more consequences you’ll have at tax time.

For example, if you create a Pie with 50 Dividend Aristocrats in 2018 and remove half of them in 2019, you’ll need to report 25 sell transactions on your tax return. This is OK, but it can cause a bit of extra work for you at tax time. Just watch out how big and complicated you make your Pies, and avoid large rebalances to reduce tax time headaches.

M1 Finance Borrow

On June 18th, 2019, M1 Finance introduced a new featured called M1 Borrow. M1 Borrow is a margin account, which means you can borrow money from the broker against your account balance. Most margin accounts are used to invest in more stocks to ‘leverage’ your investment portfolio. But the money can be used for anything.

Margin accounts involve an additional layer of risk, so do not borrow and invest without understanding the terms.

However, M1 Finance is marketing the M1 Borrow account as a cheap place to borrow money. It is compared to a credit card.

Only accounts with assets totaling $5,000 are eligible for M1 Borrow. Portfolios must also be sufficiently diversified. Eligible investors don’t need to apply to use the feature.

For the record, I do no use margin myself and don’t recommend it for investors. But some sophisticated investors may want to take advantage of the very low rate.

The idea on this platform, is to offer a cheaper alternative to credit card debt. So if you are in need of short-term cash, this is definitely a better alternative. Or you can just sell a stock.

Just don’t make a habit of paying margin against your dividend stock account. You’ll be treading water.

M1 Finance Spend

M1 Finance spend is live. It’s a debit card that is fully integrated with your M1 Finance brokerage account. You can make transfers between accounts instantly, and earn interest on your money. M1 Spend accounts are FDIC insured and accept direct deposits.

M1 Spend offers two types of accounts. M1 Spend Standard, and M1 Spend Plus.

M1 Standard

M1 Standard is free to use. It’s integrated with your brokerage account, has a debit card, and can handle all of your banking needs. However, it offers very few perks. There is no minimum account balance.

M1 Plus

M1 Plus has been removed from the M1 platform. All uses default to the former extra perks that Plus members received. Here’s what the company said in an email:

We’ve decided to end our M1 Plus membership program. Our premium features will no longer require membership and will instead be available to everyone who builds and manages their wealth on M1. Starting May 15, a $3 monthly platform fee will apply to clients with less than $10,000 in M1 assets or without an active Personal Loan. Each billing cycle will last 30 days—meeting platform requirements* at least one day during each cycle will ensure this fee is waived for you.

The annual fee is now $36 or $3/month for members with less than $10,000 in M1 assets.

M1 should reconsider this fee. Customers with less than $10,000 are the one that should not be charged a fee at all. This will not encourage them to move more assets to the platform.

It will encourage them to leave the platform for Robinhood or never join.

M1 Finance Review 2024 — The Mobile App

M1 Finance is completely accessible both through a PC desktop and mobile app. The company built both sides from the start, unlike other fintech brokers like Robinhood and Webull.

When you sign up for M1 Finance from your phone, you’ll be immediately directed to the app stores.

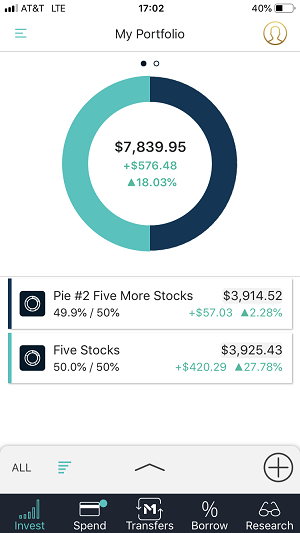

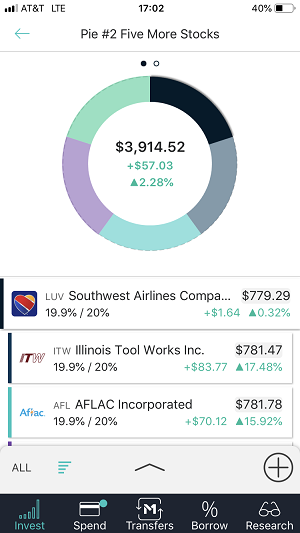

The user experience is very similar on a mobile device. Here are some screen-shots to get acquainted with the app. These screenshots are taken from my personal account in October 2019.

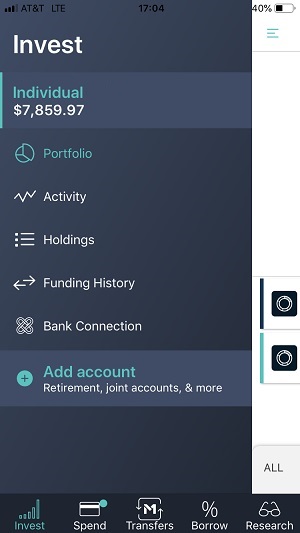

First, are the main Portfolio view and one of my sub-pie views:

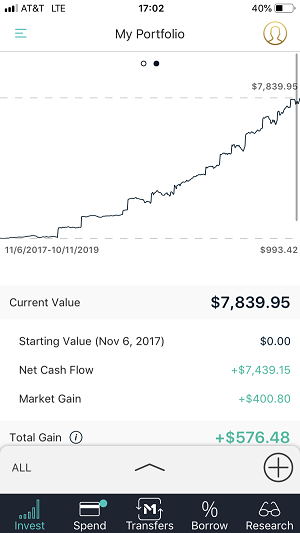

Below is the line chart view of the Portfolio growth over time (including deposits), followed by the Invest Menu view:

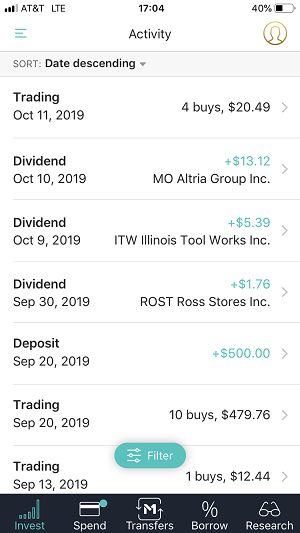

From the Invest Menu, tapping Activity takes you to the following view. Here you have any trades, deposits, and dividend payments. I asked M1 Finance many times to improve this view and they finally made some changes to make the dividend payments more clear with the date, amount, and company.

Also below is the Holdings view.

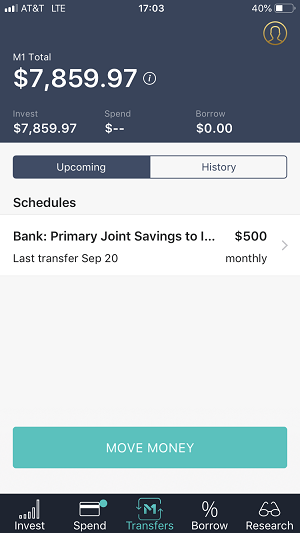

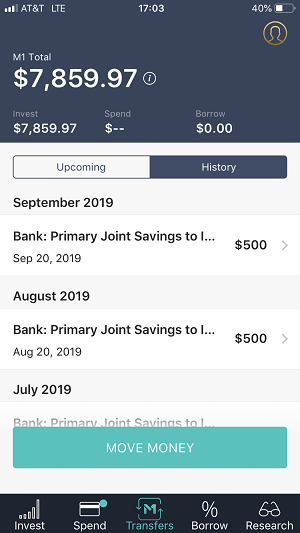

Switch to the Transfers tab on the bottom of the app to see money coming into and out of the account. I have a monthly draw from my savings account into my M1 Finance account. There’s also the history view of previous transfers. Tap the line to see more details.

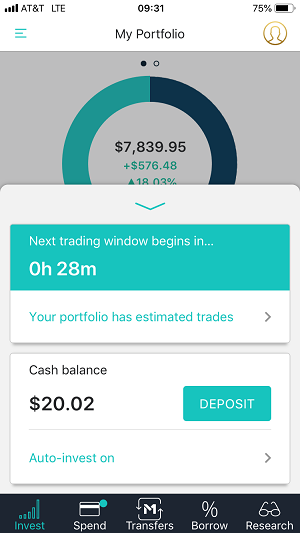

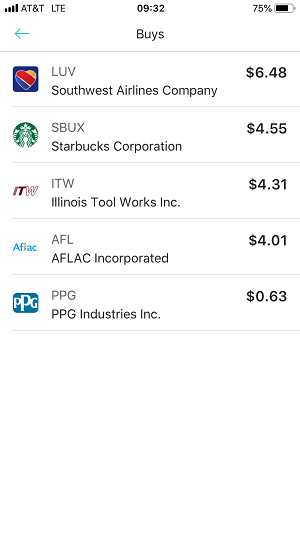

At the bottom of the Portfolio screen is an upward-pointing arrow. Tap it to deal with your cash balance. You can see I have a $20.02 cash balance, and I just changed my settings to invest all of my cash. That means, the $20 balance will be invested in the next trading window, 28 minutes from the time I took this screenshot.

Tap the estimated trades message to see the expected trades at the next window. You can see where my $20.02 is slated to be invested.

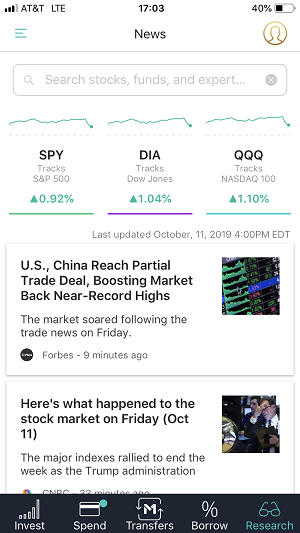

The research tab on the bottom is very strong for a mobile app. You can look at news, research stocks and funds, or browse expert pies for ideas.

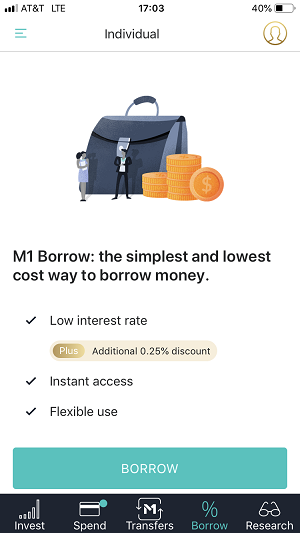

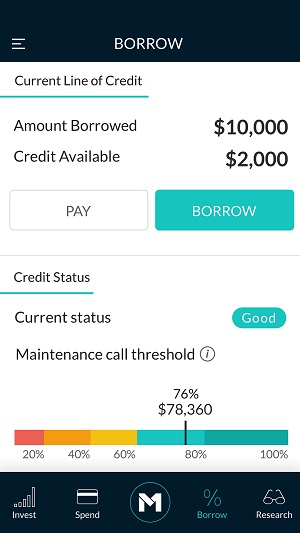

Finally, when you tap the Borrow, the app takes you to where you can sign up for the services. I’m currently not eligible for Borrow because I do not have a $10,000 minimum balance. But the second picture is a screen view of what borrowing looks like.

M1 Finance Review 2024 Cons

Before recently, I would have told you that the fee structure was the biggest con. They used to charge 0.25% on accounts with assets of $1,000-$100,000 and 0.15% for accounts with assets over $100,000. Accounts with less than $1,000 were free.

Now that’s in the past. M1 Finance is FREE.

The biggest con now is that it takes a little bit of time to acclimate to Pie investing. Experienced investors may not like this kind of interaction. You can’t simply buy and sell stocks like you can at a traditional online brokerage. DRIP (dividend reinvestment plan) investors or former Loyal3 customers will feel more at home, but with far more capabilities.

Also, the once-a-day batch trading process does not allow for real-time pricing. As I mentioned, this platform isn’t for frequent traders. There are no market or limit orders — just batch sales and purchases. So you won’t know what price you get until the trades are complete.

M1 Plus members get a second trading window.

After about two years of issuing complaints about the activity log, the M1 Finance development team finally fixed the dividend tracking issue. There is now a sequential activity transaction list that’s easier to read and track dividend payments.

What I love about M1 Finance is they listen to suggestions and make the changes. It helps that I’m a partner, but several suggestions I’ve made have been implemented.

Another issue I have is transfers in from other accounts. Though you essentially get the white glove treatment when you’re transferring in shares, those shares need to go into preset pies. This requirement makes larger transfers more difficult. If you have liquidated your old account, then the transfer is easy.

I’d like to see some options for holding stocks outside of the pies. Perhaps a Pie that is more free-form where you can own whatever you want. This would make transfers in simpler and still give you the power to create the ideal portfolio over time.

How Does M1 Finance Make Money?

Since the product is free for customers, how does M1 Finance make money? According to CEO Brian Barnes, the larger brokers made less than 30% of revenues from trading fees when they had them. That means more than 70% of revenues come from other sources.

A few other sources bring in revenues for M1 Finance. Brokers can lend shares to investors looking to sell shares of a company short. M1 Finance collects a modest fee for lending out shares to short-sellers.

The company also earns interest on cash balances. Over many customers, this amount can be significant and should grow as customers grow and place holds on cash.

Lastly, margin lending is a big opportunity in the future. Investors will be able to borrow from their securities account to help with monthly cash flow needs or for short-term investing purposes.

Since M1 Finance is a new lean company with modern technology, they are free of bloat that can affect a larger organization. The company is taking an incremental approach to growth to gain customers and momentum in a controlled manner.

Conclusion – M1 Finance Review 2024

M1 Finance is for long-term investors, not traders, which makes it very good for both dividend and index investors.

Here’s some cool insight from the Founder Brian Barnes:

After all, personal finance is largely free now. Most people’s personal finances revolve around the checking account and the credit card, which are typically free and often even incentivize use through interest, points, or cash-back. The investing account is the final component of personal finance to go free.

Now that the platform is built, M1 Finance believes they can make plenty of money through the back channels of the securities industry. More from Founder Brian Barnes about making money:

Brokerages make money via lending securities they hold, interest on cash held in a brokerage account, extending credit through margin to customers, and getting paid for distributing certain funds or to transact on various exchanges. These revenue streams are more than enough to support a strong, vibrant company.

This is also true at M1, and we will make more money from transactions and holding the assets than we would from our fee. The number one driver of M1’s success over time will be the number of users and assets managed. If going free puts M1 in more people’s hands and empowers them to manage more of their money on the platform, the move to free is a win-win.

The company has also added more revenue-producing features such as M1 Spend and M1 Borrow. But the core investing platform will be free going forward. Here’s the full manifesto.

They have long believed that online brokers will be free in a matter of years (this came true in October 2019!). Since they’ve built their platform with this in mind, their cost structure is dramatically lower than the legacy brokerages.

M1 Finance is the future of investing, today.

M1 Finance Review

-

Ease of use - 9/10

9/10

-

Mobile Access - 9.5/10

9.5/10

-

Research Tools - 8.5/10

8.5/10

-

Commissions - 10/10

10/10

-

Investment Selection - 9.5/10

9.5/10

-

Non-Investing Services - 9/10

9/10

-

Margin Rates - 9.5/10

9.5/10

Summary

M1 Finance is a top online brokerage for new investors. The user experience takes some time to get used to, but once you get the hang of it, it’s ideal for long-term investors who like to dollar cost average into stocks and ETFs. The new services, M1 Borrow and M1 Spend, are excellent add-ons for those who like to consolidate financial accounts. M1 Spend Plus currently has an annual fee which will hopefully be reduced as adoption of the service increases.

Thanks for checking out my updated M1 Finance review. I’ll continue to update and modify this review as the platform continues to age and improve. As always, if you have any questions about the platform, please leave your comment below or contact me privately if you prefer. I’m happy to provide more details on anything I missed in this review.

Disclosure: Long VTI, CAH, V, ROST, MO, SBUX, BRK-B

Disclosures: M1 is not a bank. M1 Spend is a wholly-owned operating subsidiary of M1 Holdings Inc. M1 Savings Accounts are furnished by B2 Bank, NA, Member FDIC. RBD is an affiliate partner with M1 Finance. If you open an account via any links in this M1 Finance review, RBD may be compensated. M1 is a technology company offering a range of financial products and services. “M1” refers to M1 Holdings Inc., and its wholly-owned, separate affiliates M1 Finance LLC, M1 Spend LLC, and M1 Digital LLC.

The opinions expressed are solely those of the authors and do not reflect the views of M1. They are for informational purposes only and are not a recommendation of an investment strategy or to buy or sell any security in any account. They are also not research reports and are not intended to serve as the basis for any investment decision. Prior to making any investment decision, you are encouraged to consult your personal investment, legal, and tax advisors.

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services right now:

Sure Dividend — A reliable stock newsletter for DIY retirement investors. (review)

Fundrise — Simple real estate and venture capital investing for as little as $10. (review)

NewRetirement — Spreadsheets are insufficient. Get serious about planning for retirement. (review)

M1 Finance — A top online broker for long-term investors and dividend reinvestment. (review)

Excellent review. M1 Finance is my favorite brokerage so far, although now that the other brokerage have joined the bandwagon, I might have to re-evaluate. I literally just wrote a post about leaving Computershare because I didn’t think it made sense anymore. That’s especially because there is a cost to sell stocks, even if there is no cost to purchase them. In the upcoming days, I will be initiating a transfer of my stocks from Computershare to M1 Finance.

One of the things that M1 Finance offers, that I don’t believe exists at any other brokerage firm, is the automatic rebalancing feature. Because money invested automatically go towards the under-weighted stocks, in effect, M1 Finance forces you to buy low, which is what you’re supposed to do in the first place. Additionally, I wish I had the ability to invest the dividends back into the stocks that produced them, but being forced to reinvst the dividends in the most underweighted stock is not a bad alternative.

So, while I’ll carefully consider the benefits of the other options out there, ultimately, I think I’ll stick with M1 Finance for now. Again, I think this was a great review and I hope M1 Finance business model is sustainable for the long haul.

I am curious what your review of M1 is now that they have announced a $3 a month fee if you dont have a loan balance. Same fee applies to IRA accounts that can not have loans.

I just saw the email after reading this comment. I don’t like that they are charging this fee only for people with accounts under $10,000. In their view, this will encourage people to deposit more money or take a loan. Many investors don’t have that much money to invest. I don’t think they should punish those people. They are unwise to charge this fee because tomorrow’s millionaire investors will choose another broker today.

I started using M1 based on your recommendation in 2018, but with the new fee announcement, I’ll be looking into transferring my funds and closing my M1 account to avoid additional fees.

Thanks for sharing. It is a disappointing announcement. If it is intended to get people with low-dollar accounts to move on purpose, that is bad business. I suspect they think it will encourage customers to transfer more money to M1. I think that will backfire. I’ve reached out to see if I can get M1 to respond to people like you who plan to move on.