Seek Adventure While Your Money Works for You

After two years of COVID-19 apprehension, our family is going on a real vacation — airplanes, amusements, and sit-down restaurants.

Planning for upcoming trips reminds me of the kind of retirement travel that I’m ultimately working toward — month-long+ excursions on and off the beaten path — and how I’m getting closer to that kind of travel again now that our kids are more independent.

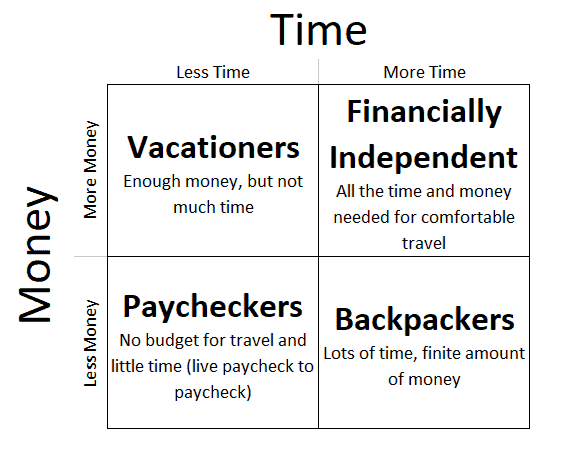

I originally published this article in May 2017. Rereading and updating it made me realize how I’m still solidly embedded in the top left quadrant (see below) and how reaching financial independence doesn’t automatically make it easy to travel within the constraints of raising a family.

Adventure is dirt cheap. You don’t need fancy mountaineering gear to explore new hiking trails, discover corners of your hometown, or find an off-the-path beach in Mexico.

One-way flights are half price.

Adventure can be a new job, burgeoning side business, early-stage romance, or anything that gets you out of your everyday routine.

International travel is the ultimate adventure because it removes you from your comfort zone and places you where streets are unfamiliar, the culture unknown, the food distinctive, and the language sometimes baffling.

Life begins at the end of your comfort zone. — Neale Donald Walsch

2001-2002 was a formative period of my life when I traveled the world for 14 months. My 18-country trip cost me about $10,000.

That’s $714 per month or $24 per day.

Today (2022), I make more than $1,250 per month from passive investment income, not including retirement accounts.

That’s plenty more than my monthly budget back then.

I traveled when the dollar was stronger and costs were lower. But today, it’s still inexpensive to travel in many countries if lush comfort isn’t a priority.

If I didn’t have a family to support, I could travel the world on passive income (without drawing down assets) for the rest of my life.

My 26-year-old self would be envious.

Time, Money, and Travel

Over the years, several close friends have planned extensive trips (~3 weeks or more) after grad school or between jobs. Each time, I tell them the same thing.

You will need more time and less money than you think. – RBD

When they return, they regret not traveling longer. It happens every time.

As your time away increases, the cost per day decreases. If you’re going to spend all that money on a flight anyway, why not extend the trip?

Usually, it’s because of work or FOMO.

The one-week vacation, popularized as a side note to the 9-to-5 job and the American Dream, is expensive per day.

One week is enough time to travel long distances and incur the costs to do so, but not long enough to lower the cost per day or return fully satisfied.

It’s hard to truly detach yourself from work and relax in just one week. There’s all that packing and travel time, then returning on a Saturday and going back to work on Monday is the worst.

As the length of your trip increases, you experience more work separation and appreciation for your destination.

Better vacation values come to light.

You see this with Airbnb. The costs to turn over a unit is high, so renters incentivize visitors to stay longer, often at a discount.

Or with resorts and tours, the longer the trips, the lower the cost per day.

One of the realities that has set in as parents of three kids is that family can be quite restrictive for travel.

Kids go to school. That leaves summer, a two-week winter break, and a one-week spring break.

Most kids have early summer activities they don’t want to miss, leaving a part of July and half of August (kids go back to school early these days).

Booking hotel rooms is a bigger challenge. Most rooms can accommodate four people. Five limits options.

My 10-year-old son has diabetes. That introduces another element of packing and planning that I could never imagine as a single twenty-something riding motorbikes helmetless in Vietnam, Cambodia, and Thailand.

I wrote a blog post (long, long ago) describing how time and money relate to different types of travelers. The “holy grail” of travel is financial independence. One of the core reasons I save money and pursue early retirement is to travel beyond the weeklong getaway.

Even though we’ve hit financial independence, our kids are in school most of the year. So unless we get extreme with homeschooling, we won’t be backpacking the world anytime soon.

Even though we’ve hit financial independence, our kids are in school most of the year. So unless we get extreme with homeschooling, we won’t be backpacking the world anytime soon.

Health is another element that’s become more apparent since I originally wrote this blog post.

As we age, we become less capable of certain types of adventure. We also become less comfortable leaving familiar healthcare services.

If all goes well, I expect we’ll have about a 10-15 year window of flexible, financially independent travel sometime between when our kids are independent and our health becomes restrictive.

That travel window is one of my primary motivators to save and invest. But I’m not waiting for it to get busy planning.

If I Were 26 Again

Age 26 was the perfect time to travel. I’d have traveled even longer knowing what I know today.

Traveling for long periods today is so much easier.

Communication was limited to internet cafes back then. Backpackers didn’t travel with iPhones or laptops. You had to find a reliable internet café and pay for time on a shitty computer with an unfamiliar keyboard to communicate with family.

Facebook didn’t exist. If you didn’t exchange emails with new acquaintances, you’d never find them again.

We had Moleskine journals instead of blogs and weren’t shy about sending postcards.

Now travelers just need WiFi and a smartphone.

Even more empowering, widespread connectivity and lightweight laptops open up the possibility of working remotely via employment and creative entrepreneurship.

Earn a few hundred from passive income and just a few hundred dollars more from an online business or remote work from a site like Fiverr, and you can travel or live abroad perpetually.

Of course, I’m not the first to figure this out. Travel bloggers and Instagrammers scattered worldwide like to tell us.

The WiFi-ready cafes of Chang Mai and Cusco are surely over-flowing with travelers/digital nomads with their noses buried in laptops.

And why not? What better way to spend your 20s than exploring the globe by living off passive income and earning a little extra on the side?

That’s what I’d be doing if I was 26.

Family building, saving for retirement, a real career, and everything else can wait.

We’re Not all 26 Anymore – So Now What?

But I’m not 26. You probably aren’t either. Maybe you have kids and a mortgage, and you’re pursuing financial independence, but it’s still a long road.

Travel will have to wait until retirement. Right?

That was my original plan. Work until I’m 55. Quit. Travel the world with Mrs. RBD while the kids are in college or starting their careers.

But that’s at least another nine years away. I’ll be nine years less healthy. In nine years, today’s undiscovered destinations will be overrun by tourists. Waiting nine years is just too long.

I’ve doubled down (several times now) on my retirement and financial independence goals and accelerated our saving and investing.

It’s part of why I started a side business, to empower the future me and create more options untethered from a full-time career. We’re there, just one last leap.

Even with the kids in school for the next decade-plus, my being untied to a full-time job will open more opportunities to travel.

We aspire to drive cross-country to visit grandparents, ride trains in Europe, and see wild pandas and kangaroos.

People of all ages reject full-time work and design their lives around flexibility, happiness, and adventure instead of material objects and dream homes every day.

But it isn’t easy. It’s a deliberate choice that requires planning and some risk.

Ultimately, my goal is to live life without the constraints of time and money — how I lived when I sought adventure in my 20s.

But adjusted for my age, current priorities, and the human beings now by my side.

Can You Really Build Enough Passive Income to Seek Adventure Perpetually?

Back to the title of this blog post — it’s taken me about 18 years to build more than $1,250 of monthly passive income. Most 20-somethings won’t be able to generate that kind of investment income in a decade.

But people in their 30’s, 40’s, and beyond sure can.

Should you wait to travel until your passive income covers your monthly travel expenses if you’re eager to travel and young?

No, definitely not.

Choose to travel first. Then figure out the details.

What do I mean by that?

If you want to travel, set a goal to travel. Like setting a savings or retirement milestone, motivation will push you to achieve your goal. Pick a date or frame, then make a plan to get there and execute.

The pandemic is nearly over, so it’s time to start planning.

Start building income streams.

Change shit up to improve your cash flow. Invest the savings into income-producing assets, ETFs with a decent yield, or real estate via crowdfunding platforms.

Start small and build.

Eliminate recurring monthly payments.

Automate and simplify your finances to streamline your life.

Earn credit card rewards bonuses to cover major expenses like flights.

Start an online side hustle and become location independent.

Stash cash away. If you can save just $2,400, that’s easily 100 days of adventure, spending $24 per day. It’s possible.

Combine your chunk of cash with a few other income streams.

Maybe work the front desk at a hostel in Santiago for a free bed and eat nothing but empanadas for a month. You’ll be amazed at how far you can stretch your budget.

Maybe you don’t like travel. If so, you probably didn’t make it this far down the page.

Middle-aged like me? Got family? Feel stuck in your day-to-day life?

That doesn’t mean you can’t seek adventure. Go find it.

Photo credit: nuno_lopes via Pixabay CCO Public Domain

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

- Dividend Kings — 50+ stocks that have increased dividends for 50+ years.

- Monthly Dividend Stocks — List of 70+ stocks that pay a dividend every month.

- Dividend Champions — 140+ stocks that have increased dividends for 25+ years.