Investing Strategies in Light of the Market Volatility

Patience is not a skill or an inherent ability. It’s a practice, one that does not necessarily develop with age or wisdom.

Successful investing takes patience because as you extend your investment horizon, your chances of success increase.

You can’t expect good results in the short-term, but you can expect excellent results 10-20 years out if you invest regularly and don’t sell when the sky appears to be falling.

During recent market volatility, investors were excited to jump right into the market when it was down just 5% to 10% from its all-time high. Our brains have been wired to buy any stock market weakness for the past 11 years.

Any investor who started in the last ten years knows no other response.

On Twitter, I witnessed retail investors hurrying out of bonds to buy stocks without much attention to the overriding problem with the market right now.

Stock prices are a reflection of a company’s ability to earn a future profit. Investors often forget that toward the end of a bull market.

Right now, corporate earnings for several vital industries can no longer be estimated accurately as a result of the COVID-19 virus outbreak and pending remediation. So there’s no footing in the market.

If that wasn’t bad enough, the Saudis decided to inject an oversupply of oil into the markets for political reasons, causing the price of crude to plummet. Lower oil prices affect everyone, sometimes negatively.

These two significant external forces have disrupted stock price discovery.

Until there is a better understanding of the disease, and companies begin reporting earnings in the coming quarters, we should have no expectations of calm or upward price mobility.

On the plus sign, volatility causes overselling. When stocks oversell, it’s an opportunity for long-term investors.

I’m not an expert, and I’m often very wrong about the stocks. But in the current environment, I’m exercising more patience than usual.

Here’s what’s on my mind and how I’m investing in light of the market volatility.

Table of Contents

Certain Uncertainty

If there’s one thing we know for certain about the stock market is that it hates uncertainty. That’s why the COVID-19 virus is causing such a stir. Its effect on the global economy cannot yet be measured. Not even close.

We won’t know its exact effect until several quarters of company earnings and global GDP numbers.

China’s manufacturing and supply chains, airlines, cruise lines, hotels, and energy companies, are all suffering disruptions. Trying to understand the extent of the damage is impossible at this point.

An acquaintance of mine works for a large hotel and conference center. He said Q1 revenue could be down $50 million — for one hotel!

What we do know is that several companies from a mix of industries promptly pre-announced impact to bottom lines. And since stock prices are ultimately a reflection of company earnings, decreased earnings will lower the performance of the stock market.

By how much, we won’t know for a while.

Of course, the market does whatever the hell it wants most of the time. Amid the uncertainty, investors must revert to fundamentals, which is earnings.

Market analysts judge earnings a few different ways:

- Quarterly earnings and year-over-year growth

- Trailing twelve-month (TTM) earnings

- Estimated forward twelve-month earnings

- Price to earnings (PE ratio = stock price/earnings per share)

- Price to earnings growth (PEG ratio = PE ratio/earnings growth rate)

The stock market generally trades based on forward/estimated earnings, not trailing twelve-month.

The chaos brought on by the COVID-19 virus is quickly decreasing company earnings. With oil prices crashing, the entire energy sector is in total disorder too.

This is a recipe for extended market fluctuations.

Once earnings settle, the markets could tumble even further when investors can finally assess the damage.

And Let’s Not Forget the Yield Curve Inversion

A yield curve inversion has preceded all nine recessions since the 1950s. It’s one of the most-watched economic indicators, but it’s quickly forgotten after it happens.

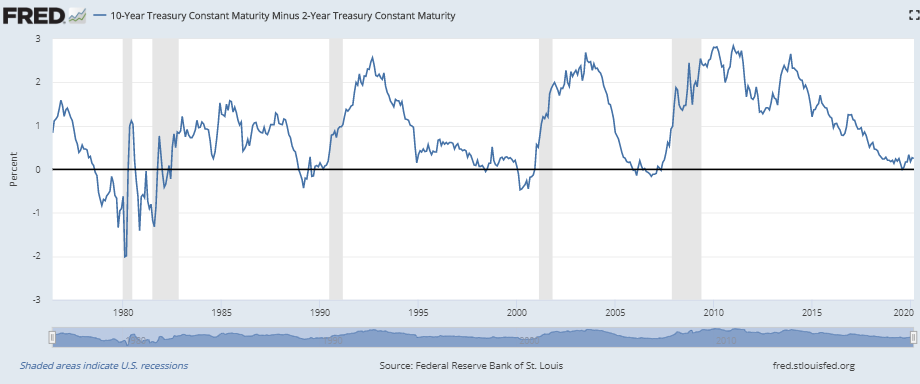

A yield curve inversion is when the yield of the 10-year U.S. Treasury Bond falls below the yield of the 2-year U.S. Treasury Bond.

During a healthy economic expansion, you usually see a left to right upward slant on the yield curve.

On August 15th, 2019, the 10-year fell below the 2-year (click to see a chart of the yield curve).

A yield curve inversion doesn’t guarantee an economic calamity is imminent, but it suggests strongly that a recession is around the corner.

According to research by Ben Carlson, for the last five recessions, the average lag time between the inversion and the beginning of the recession was 16.2 months.

It’s been about seven months since the inversion, and it takes two quarters of negative GDP growth to declare the beginning of a recession. So we seem to be headed in that direction if we’re not there already.

COVID-19 was the trigger mechanism for an early arrival of what was already likely to happen.

If indeed we are in or headed for a recession, there’s still no predicting where or when the stock market will bottom.

Here’s a chart of the spread between the 2-year and 10-year bonds. The inversion occurs when the blue line dips below the black line. The gray vertical lines indicate recession periods.

Cravings

When the stock market quickly falls as we’ve seen in the past few weeks, I feel like my kids on Halloween night — they want to eat every piece of candy right then and there.

My reflexive impulses want me to deploy all of my cash when the market falls by 10%. This works during a multi-year bull market.

But when the fundamentals of the economy change dramatically, patience is essential.

In the past, I’ve acted on buy reflexes far too soon.

During the dot-com fiasco, I bought internet stocks after the bubble popped because I believed in the future of the online world. Thankfully, I didn’t have much money because valuations were absurd.

I lost money.

In 2006, when the real estate bubble finally burst, I bought my first home, thinking “nice – the bubble finally popped, time to buy!” I bought after the pop, but before the major financial crisis.

I lost money and freedom.

It took another 3-4 years for prices to shake out in the real estate market. Had I been more patient, I’d have avoided a serious financial mistake.

Much like 2006, I’m itching to buy stocks at a discount today. Since selling the condo last year, I’m flush with cash. I’ve held the sale proceeds in a high yield savings account, conservatively waiting until I fully understood the tax consequences

That part is done. Taxes paid. The condo is out of my life.

As of Monday morning this week, I had about 12% cash in five retirement accounts, including Mrs. RBD’s IRA contributions from last year, a new SEP IRA contribution from my online business income, and a bit of cash on hand for opportunities like this.

Now that stocks are down about 19% as I write this (Tuesday night), my fingertips are eager to place buy orders in both my dividend growth portfolio and various retirement accounts.

So I’ve started to nibble on stocks and index funds. However, I’ve resisted the urge to make large purchases, saving the bulk of my cash for what lies ahead.

How I’m Investing During the Downturn

One of the keys to investing in a down market is avoiding emotional responses to the market. It’s difficult because the volatility messes with our brains.

You can remove emotional responses through regular automated investing and using preset market levels to initiate purchases.

Most of the investing I do is through automatic contributions to my employer plan.

But I am also placing buy orders on index funds when the indices hit certain levels.

Some might call this timing the market, which is a potty phrase in the personal finance space. However, I have cash on hand meant for opportunities, which are more plentiful today than a month ago.

I’m not a trader, so I do my best to ignore what’s happening during the trading day. Plus I have a real job, and often can’t see what’s going on.

So I rely mostly on end-of-day mutual fund orders and stock limit orders for non-automated purchases.

Here are the four ways I’m investing today:

- Automated bi-weekly 403(b) contributions

- Automated bi-weekly M1 Finance pie contributions purchases

- Level-based index fund IRA purchases

- Individual dividend stock limit orders

Plus a bonus idea.

Automated bi-weekly 403(b) contributions

Nothing new here. I’m always investing through my employer-sponsored 403(b). I contribute the maximum allowed, and my employer matches about 10% (crazy good).

These contributions usually hit my Fidelity account on payday, every other Friday. I’ve chosen two index funds for all contributions: The Fidelity Total Stock Market Index (FSKAX) and the Fidelity Global ex U.S. Index Fund (FSGGX).

My investment horizon is at least 15 years, so I can afford the risk of being 100% in equities for this account. I use my IRA for bond exposure.

Automated bi-weekly M1 Finance pie contributions purchases

I also have an automated fund transfer set to contribute $1,000 to my M1 Finance account every other Wednesday. I have three equally-weighted pies, each with five stocks.

Whenever I deposit new funds or receive dividends, the platform automatically buys the stocks which have fallen the most, taking me back to my target allocation (currently 6.66% per stock). I call this strategy diversified dollar-cost averaging. It’s similar to single-stock DRIPs, but with more stocks.

I bumped the deposit amount up to $1,000 from $500 last week to take advantage of the downturn.

Read my M1 Finance review to learn how the platform is different than traditional brokers. My dividend portfolio and other investments are visible on my portfolio page (M1 stocks marked with an asterisk).

Level-based index fund IRA purchases

Between the two of us, Mrs. RBD and I have five IRAs — a traditional and Roth each, plus my new SEP IRA. She is fully invested in domestic and foreign stocks and bonds. My accounts still have some cash to invest.

I’ve kept some cash on the sidelines waiting for an opportunity to buy at a discount. This cash is from last year’s contributions (Roth) and this year’s SEP IRA contribution, which I just deposited last week.

I also reallocated 5% of stock index funds in my IRA to a money market fund late last year after watching the market increase by 30% in 2019. There are no tax consequences for this maneuver in an IRA.

With the yield curve inversion and an economy unworthy of 30% market moves, I thought it to be prudent to exercise some caution.

What I like about mutual funds is they aren’t traded during the market session. So when you place an order, it won’t execute until after the close.

Using mutual funds, I avoid the constant price movements during the day. I look at the market levels in the final trading hour of the day and place orders if the market is looking to close down.

I’ve noted the S&P 500 all-time high. Then whenever the market falls another 5%, I put more cash to work. I started with a small fund purchase at the 10% level, and I’ve increased my investment amounts when the market hit 15% and 20%.

This allows me to participate in today’s discounted prices while holding out for tomorrow’s lower prices.

I’m sharing S&P 500 price thresholds on Twitter when they happen.

S&P 500 all-time high:

3,393.52 (Feb 19th)

Down 5% – 3,223.84 ✔️

Down 10% – 3,054.17 ✔️

Down 15% – 2,884.49 ✔️

Down 20% – 2,714.82 ✔️

Down 25% – 2,545.14

Down 30% – 2,375.46$SPY #COVID19 #marketcrash #bearmarket

— Retire Before Dad (@RetireBeforeDad) March 11, 2020

Ideally, on the day when the market bottoms, I’ll invest the last bit of cash. Of course, there’s 0% chance of that happening.

The bottoming process could last for months (years?), with several sharp swings, peaks, and valleys. Here’s an article from 3/12/2020 suggesting an “L” or “U” shaped recovery.

That’s why I’ve only invested about 15% of my retirement cash so far. I’m being patient this time around. I expect if we get to a 30%-35% decrease from all-time highs, my patience will start wearing thin.

I’m investing this money for the next 15-30 years, so I don’t need to be a hero and attempt to nail the bottom, which is impossible anyways.

If stocks continue to fall and I’m out of cash in retirement accounts, I have the option to convert bonds over to stocks. About 10% of my retirement accounts are allocated to bond index funds.

If the market has already bottomed, so be it. I’ve invested at a discount and can still look for more opportunities.

Individual dividend stock limit orders

Finally, as the market falls, I’m cautiously adding to my primary dividend growth stock portfolio. Now that I’ve paid depreciation recapture taxes on my condo and set aside a very generous emergency fund, I still have cash left over to invest.

I invest in individual dividend growth companies to increase the amount of income my portfolio generates. My priority is to add to stocks that I already own and still like.

For example, I bought ten shares of Disney (DIS) this week. It’s a stock I like, priced significantly lower today compared to last Fall. Disney is a diversified company I want to own for the rest of my life, even though it will suffer from reductions in travel and cruising.

Now that most brokers are commission-free, I tend to add to my portfolio in chunks of $750-$1,000 at a time. I look at smaller-percentage portfolio holdings trading near 52-week lows that still look healthy going into recession.

Then I want to add a small number of new holdings. I start with my Dividend Aristocrats rankings for ideas.

I use basic charts and metrics to find an entry point and set a limit order that closes at the end of each day. I look at the most recent low price and try to pick up shares below there. I sometimes use simple moving averages and Bollinger bands as reference points.

If the stock doesn’t hit the limit order during the day, it’s automatically canceled when the market closes.

Again, it’s nearly impossible to buy any stock or fund at the bottom. But this strategy forces me to demand a better price, and remain disciplined by letting the orders cancel. If I don’t buy the stock, so be it.

This strategy works for me and my comfort level with the current volatility, but it involves more emotion and risk. There’s always the temptation to catch the falling knife. Only invest this way if you’re comfortable and prepared to regret some investments!

Bonus

If you’re not comfortable with the stock market right now, you can always invest in alternative assets or outside of the market. But keep in mind, the stock market always recovers. When it falls like this, it’s usually a long-term opportunity.

Concerns

I haven’t sold any stocks or funds since the S&P 500 high on February 19th. I sold one stock on 3/12. I will hold all of my index mutual funds, but might sell some individual stock holdings.

That’s because I’m in this for the long-haul. If I can identify a stock that is either headed for bankruptcy or a severe dividend cut, I’d like to sell ahead of time. But this is extremely difficult.

I’m diversified with more than 50 individual stocks. If any company loses significant value or cuts the dividend, it won’t destroy my entire portfolio or passive income strategy.

Aside from staying in business, my primary concern with owning individual stocks is the company’s ability to pay and maintain its dividend. The nature of my investment strategy is to value annual dividend growth and total return.

Markets fluctuate wildly. Dividends are more stable and predictable.

Travel and energy are the two most apparent risk areas right now. More industries may become vulnerable as the economy sorts itself out.

Travel

I own one airline stock, Southwest (LUV). It’s a 97% domestic airline, so there isn’t much risk due to China and Europe. But its earnings will suffer.

The stock is down 28% from its 52-week high, which isn’t that bad so far. The company only pays a $0.72 dividend for a 1.58% yield. Most importantly, the dividend payout ratio is around 16%, which is a low risk.

Southwest will have a few problematic quarters and may freeze its dividend growth, but I intend to continue to buy through my M1 Finance account. Southwest is less than 1% of my total portfolio and dividend production.

I don’t own any hotel or cruise line stocks (aside from Disney) but may consider some well after the dust settles.

Energy

I’m much more concerned about energy stocks. Oil prices fell nearly 30% on Monday this week. This price move immediately impacts domestic oil producers and equipment makers.

Chevron is one of my largest holdings. I’ve owned it since 1995. It’s the one stock that I admit I have an emotional connection.

My uncle gave me my first share for my 20th birthday, and it’s been growing and paying me dividends ever since. Chevron is a behemoth with deep pockets and a long-term commitment to paying and increasing its dividend.

But if oil prices remain low, the company may eventually need to cut the dividend. In the past, they’ve borrowed money to pay the dividend. I prefer they didn’t.

With interest rates being so low right now, I won’t be surprised if that happens again to get them through the dip in prices.

If the company cuts the dividend, I’ll likely continue to hold. Cutting would help sure up cash flow and get them through a difficult time. There’s also the possibility the Saudi’s cut a deal with OPEC and oil prices start to rise again.

Chevron makes up 3.5% of my portfolio and produces about 6% of my dividend income.

Another company I’m worried about is Helmerich & Payne (HP). This mid-cap company specializes in land oil drilling equipment and operations. Oil prices need to stay above a certain level for domestic drillers and frackers to make a profit.

The stock price has cratered, falling nearly 70% from its 52-week high. The yield has shot up to 13.5%, indicating a likely dividend cut in the future. This company is a dividend champion, with a 47-year dividend increase streak on the line. The balance sheet is relatively strong, with almost as much cash as it has debt.

It makes up about 1% of my portfolio now, and 3.5% of dividend income.

I may have been too patient with this stock. It’s not too late to sell — stocks can always go to zero.

Update: I sold HP Thursday morning.

Disclosure: Long all stocks and funds mentioned in this article

Photo via DepositPhotos used under license

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

- Dividend Kings — 50+ stocks that have increased dividends for 50+ years.

- Monthly Dividend Stocks — List of 70+ stocks that pay a dividend every month.

- Dividend Champions — 140+ stocks that have increased dividends for 25+ years.