7 Streams of Income Beyond a Salary

Doing taxes is never fun. But each year, I find that our income has become more diversified than the previous. We now earn more than 7 streams of income — not counting my salary.

A salary is great if you don’t mind full-time work. But it can become an unhealthy addiction.

You can break the addiction by spending below what you earn and investing what’s leftover.

The assets accumulated and income generated from investments give you flexibility and, eventually, the option to stop working.

We’ve earned 7 streams of income or more since before I was unemployed in 2017.

Our income streams have changed since then. We sold our investment property, Mrs. RBD is doing part-time work, and a few passive income-producing assets are different.

But the strategy remains the same — build multiple income streams for security, wealth, and options — brick by brick.

Even wealthy business owners and high-income professionals (doctors, lawyers) diversify their investments and income streams.

Low-to-average income folks often do not because it takes excess cash to build passive investment income.

However, online platforms have dramatically improved investing inclusivity by lowering minimum investment amounts to $1 to $10 with little to no fees, which is incredible compared to a decade ago.

But it still takes knowledge and confidence to begin investing.

Now that inflation is closer to 10% rather than 2%, many passive income streams are less desirable.

Hopefully, that changes as the Fed raises rates to tame inflation. But patient investors can accumulate assets now, building income streams with yields below inflation.

Eventually, it will flip.

The best way to fight inflation today is to earn more money — raises, gigs, and side businesses. If you’re worried about inflation, prioritize extra earned income.

It may be challenging to find investments returning greater than inflation over the next few years.

Here’s a list of 7 streams of income to consider.

Table of Contents

1. Real Estate Crowdfunding Income

Real estate is a reliable asset class and a tubular way to surf the inflation wave.

Many of you probably own a home, so you’re covered there. Some of you may own one or multiple rental properties.

Rentals are still my favorite form of long-term semi-passive income, even though I don’t own any directly. The threefold benefits of income, property value appreciation, and tax advantages are hard to beat.

Go for it if you can find profitable rentals and stomach managing them or hiring a manager. Managing a rental property can sometimes be a pain (I managed one for eight years).

About five years ago, I started investing in real estate crowdfunding to get more exposure to real estate without the hassle of managing rentals.

It’s paid off.

I now own a small portion of 125 commercial and multi-family residential properties through a D.C.-based investing platform called Fundrise.

I’ve tried a few other crowdfunding sites, including PeerStreet and the now-defunct RealtyShares.

But I prefer Fundrise to those platforms for a few reasons:

- $10 minimum investment

- Easy to diversify

- Available to all U.S. investors (non-accredited)

- Customize your portfolio for dividends or growth

It doesn’t hurt that my total investment return has been 13.2% since early 2017.

My $24,000+ account yields about 4%, paying me about $900 per year. The yields fluctuate, so the income is less predictable than fixed interest or dividend growth stocks.

I’m reinvesting the dividends and adding $500 more to the account every month (here’s how I’m investing each month).

That income is taxable, so it’s better to invest through an IRA if you can. Max out tax-advantaged accounts first.

Fundrise has recently added larger funds ($1 billion limits), making it easier to diversify and liquidate holdings.

Check out my Fundrise review for more. Hopefully, I’ll write an update on my five-year Fundrise returns later this year.

I’m also diversifying my real estate holdings with a new investment on the EquityMultiple crowdfunding platform. A multi-family mixed-use property became available in a neighborhood I know very well.

It’s a five-year illiquid investment with a solid yield and potential for 15%+ total return. Read my EquityMultiple review to learn more about the platform.

Please note: This is a testimonial in partnership with Fundrise. We earn a commission from partner links on RetireBeforeDad.com. All opinions are my own.

Read more: 24 Small Investment Ideas to Cultivate Wealth

2. Municipal Bond Interest

Municipal bonds are one of the passive investments I’ve liked that now lag far behind inflation.

Municipal bonds are securities that government entities use to raise money for operations and capital-intensive projects.

For example, the large county I live in issues municipal bonds to build infrastructure and public-use buildings such as recreation centers.

Investors lend money at a fixed interest rate, and the municipality pays back the debt over an established duration.

Municipal bond yields are tax-exempt, making them a good choice for non-retirement accounts (and useless in retirement accounts).

I started buying them in my taxable accounts to reduce volatility and tax burden.

These bonds are low-risk and easy to buy through a broker.

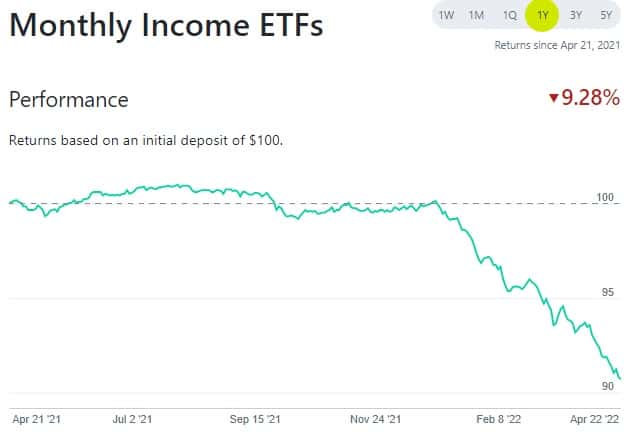

I prefer to own a diversified pool of municipal bonds through an ETF such as Vanguard’s VTEB, Blackrock’s MUB, and the SPDR HYMB, which pay monthly dividends. Each fund owns more than bond 1,500 holdings.

I own all three in a monthly dividend income M1 Finance Pie. Due to inflation fears and market volatility, it’s down almost 10% — but doing much better than growth stocks and the broader market.

Lower prices mean higher yields.

I expect yields to increase on muni bonds as municipal borrowing becomes more expensive as the Fed Funds rate increases in 2022.

But it may take time for the gap between muni-bond yields and inflation to narrow.

For now, you’re going to lose against inflation. But just about everything is losing to inflation.

Have low expectations for total return. But if you’re keen on building low-risk tax-exempt interest and expect to hold for many years, these may meet your investment objectives.

Muni bond ETF dividends act and feel like stock dividends. But rest assured, they are a different asset class. Yet, just as easy to own.

Read more: Are Municipal Bond ETFs Right for your Portfolio?

3. Gig Income

The gig economy is the way to go for anyone who wants to ramp up extra income to fight inflation.

It’s not for everyone (hence, seven items on this list, not just one).

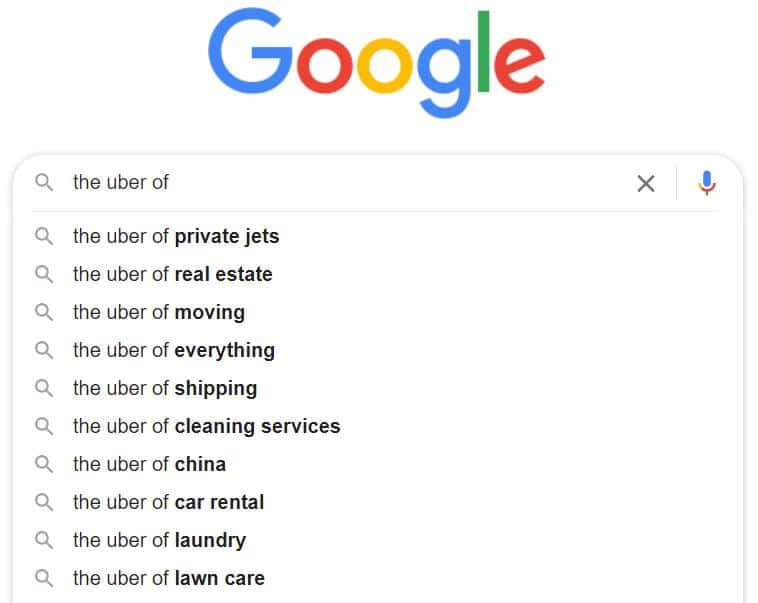

Uber drivers get a lot of credit for being the most visible side gig. But you don’t need to be an Uber driver to make gig money.

All kinds of industries have replicated the business model.

Google “the uber of” and Google suggests a few gig ideas. There are many more.

Figure out what skills you have and wouldn’t mind doing on the side.

Then give it a test drive. Gigs provide a low barrier to entry and small commitments to get started.

Platforms such as Upwork and Fiverr are marketplaces where people with digital skills (including writing) can showcase their abilities and get short-term gigs.

Aspiring freelancers and gig workers can join niche-specific Facebook groups or online forums for tips and gigs. I’m in a finance writing group and see short-term jobs often.

You have marketable skills, and there are opportunities to earn that fit your background.

If you want the extra income enough, make time for it.

Earning more is the best way to beat 8% inflation.

4. (Side) Business Income

Blogging has been a good side business for me. But it took a few years to write enough content and get website traffic that enabled me to earn money.

Gigs are good for earning money fast.

But side businesses have three outstanding benefits:

- Earn more (eventually) — No ceiling compared to salary or gig work.

- Passion-driven — Most salaried careers are not.

- Career offramp — Step away from a less enjoyable job.

I know what you’re thinking.

All these Twitter bros and Facebook moms are telling you the same thing — if you “take control of your life (and buy my eBook/online course)”, you can be your own boss and become rich too!

So I’m here to tell you — you can earn more, and you don’t need to buy an online course. But you must commit with confidence.

I’ve made more money from my online business than I ever thought possible. And it’s fun.

But money didn’t happen overnight. I wrote weekly blog posts for five years and launched a second website before I started making a steady income from my business.

I also started a very low-cost side business (blogs), which requires little upfront investment and no employees.

I didn’t open a restaurant or buy $200,000 worth of beer-making equipment.

The beauty of low-cost side businesses is you can test the waters while still working a full-time job. You can start a business with a few hundred dollars.

Once validated, you can take the business full-time or keep it as a side business to supplement your primary income.

That’s what I’ve done. I still have my full-time job (for now), which provides a salary and healthcare.

Then my business income is gravy on top. I love that. My writing income is the largest of my non-salary 7 streams of income.

But if I don’t put in the hours, the income slows. It takes time and brainpower.

Some days I don’t have enough.

You have to want it bad enough to put in the extra hours to succeed.

5. Stock Dividend Income

In a dividend growth stock portfolio, I aim to buy high-quality companies to produce a predictable cash flow stream that increases each year above the normal inflation rate (through dividend increases). I’ve invested this way since 1995.

These companies have a history of consistent earnings growth and increased shareholder distributions.

I intend to hold these stocks for the rest of my life. Dividend income is my primary investment objective for that portion of my overall portfolio.

I consider my dividend stock portfolio my baseline income stream instead of my salary. I earn more than $1,000 per month from dividends without working.

It’s also my favorite of the 7 streams of income because I can take action that moves the needle every day.

That number is easily measurable and will grow over time if I don’t sell the stocks and choose stocks not vulnerable to dividend cuts.

This is a supplemental investment strategy.

The bulk of my wealth is mostly in index funds in retirement accounts (IRAs, 403(b)). When I reach retirement age, I intend to only draw down retirement accounts after spending dividend income.

My dividend stock portfolio hovers around 60 stocks. I rarely add new holdings to this portfolio, but I add money to my existing holdings every month.

Read more: How to Invest in Dividend Stocks

6. Alternative Asset Investment Income

Financial innovation, technology, and loosened regulations have opened new opportunities to invest in alternative assets previously unavailable to ordinary investors.

Some investable assets are nothing new, but there are new ways to access them.

For example, at Masterworks, you can buy ownership of fine artwork. At AcreTrader, you can passively own small pieces of farmland.

Many alternative investments produce reliable income streams with total returns and risk levels in line with or better than long-term stock market returns.

If you’re adventurous, the bursting economy around cryptocurrencies, decentralized finance, NFTs, and web3 is a candy store for alternative asset investors.

Beyond crypto-trading, cryptocurrency owners use their crypto assets to earn high-yield interest on holdings. Interest rates vary by coin, but yields are generally higher than even the best bank savings rates.

This page at Gemini explains it better than I can. However, this area of DeFi is getting more scrutiny from regulators. BlockFi, another crypto platform, had to shut its U.S. offering down.

I don’t understand the crypto/DeFi products well enough to recommend them. DeFi is still the wild west, so be careful if you invest any capital.

But other alternatives are a great addition to your portfolio. Buy what you understand.

7. I Bond Income

The U.S. Government issues a savings bond called Series I. It’s a near risk-free savings product that pays interest to fight against inflation.

The interest rate is derived from a combination of a fixed rate that doesn’t change and an inflation rate set twice a year.

Here is the latest interest rates from TreasuryDirect.gov.

The variable rate fluctuates with inflation, hence the recent increase.

Since the U.S. Government issues and backs these bonds, these are essentially risk-free investments.

There’s a blog called TIPS Watch that does a nice job of explaining the recent increase.

A few things to keep in mind:

- There’s a $10,000 maximum investment per person per year.

- The rate fluctuates as inflation rises and falls, potentially making these more or less desirable in the future.

- The bonds pay semi-annual interest payments (paid 6 and 12 months after purchase).

- This investment is taxable as ordinary income, but not until you cash out the bonds (making them tax-deferred). Interest automatically reinvests.

- These are Illiquid for one year. If you redeem I-bonds before five years, you will forfeit three months of interest.

I intend to let the investment ride for as long as the interest remains competitive compared to bank savings.

I may use these bonds to fund my children’s college education one day, as they may be redeemed tax-free for qualified education expenses for taxpayers under certain income thresholds (see IRS Form 8815).

Go to TreasuryDirect.gov to begin investing.

Conclusion — 7 Streams of Income Beyond a Salary

We all want more flexibility, but financial obligations often prevent us from achieving our ideal lifestyles.

COVID, in a way, gave us more freedom from our careers than we had before.

Now that companies are clawing people back from home offices, you might be looking for a more permanent escape.

Reducing financial obligations (debt, recurring payments) can start the untethering process.

However, you can only reduce obligations so far. If you’re like me, other people depend on you for healthcare and financial security.

You can’t just walk away from them.

Some costs don’t go away (food, shelter, etc.), and there are costs we don’t want to give up because they make our lives better (travel, entertainment, kid’s activities).

By spending less than you earn and saving and investing what’s leftover, you can gain security and flexibility.

The nest egg accumulated is your wealth, keeping you and your family more secure as it grows. The income generated from your wealth gives you the flexibility to transition to your ideal lifestyle if you haven’t achieved it yet.

The 7 income streams outlined above may help you trek that path.

Disclosure: This is a sponsored promotion for the AcreTrader platform. RBD may have investments in companies represented on the AcreTrader platform. This informational post is by no means a promotion, solicitation, or recommendation of any specific investment.

Photo credit: pixel2013 via Pixabay

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

- Dividend Kings — 50+ stocks that have increased dividends for 50+ years.

- Monthly Dividend Stocks — List of 70+ stocks that pay a dividend every month.

- Dividend Champions — 140+ stocks that have increased dividends for 25+ years.