Personal Basic Income: How to Create a Perpetual Paycheck

Maybe you’ve heard of universal basic income (UBI).

Maybe you’ve heard of universal basic income (UBI).

UBI is a type of social program administered by governments to provide basic income for citizens — ideally, enough money to cover basic expenses or meet poverty level income.

Universal basic income became a popular topic in the political discussion during the 2020 U.S. presidential election, promoted by candidate Andrew Yang.

But it wasn’t a new concept. Several countries and localities have tried such programs to varying degrees of success.

Alaska has had a UBI program since 1982. Several more programs started during the past few years.

Business leaders like Mark Zuckerberg have expressed interest in it, saying that UBI would give people a cushion to take risks and provide a “freedom to fail”.

Knowing the U.S political landscape, it’s unlikely that one of these programs will ever become a federal law. Stimulus payments and tax breaks are likely the most we’ll ever see from the federal government.

But you can use the concept of UBI to create your own personal basic income (PBI), using investments to build multiple income streams that will ultimately serve as basic income.

Many of you already earn PBI. If not, you can start growing your PBI today.

If you persist, you’ll eventually earn enough to cover some or all of your living expenses.

Table of Contents

Why Creating Personal Basic Income is Important

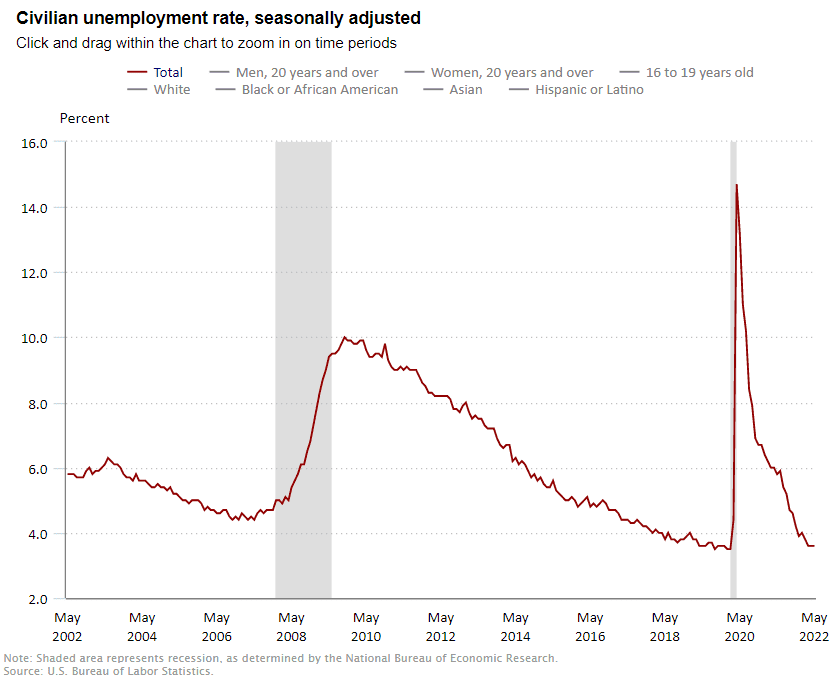

Right now, unemployment is at historic lows.

When the economy is strong, most people forget how bad it can get.

But unemployment can crush long-term financial planning goals.

Remember 2020? How about 2007-2009?

The low employment rate of today likely won’t last as we’re in a rising interest rate environment.

Building personal basic income is a hedge against unemployment. You may feel secure in your job, but you can still lose it.

For those of us who have experienced sudden unemployment, having other income sources provides some security and peace of mind.

When I lost my job in October 2017, I earned about $750 of personal basic income (or passive investment income).

That wasn’t enough to cover our mortgage or COBRA healthcare expenses.

But it covered utility payments and groceries for my family of five.

Our emergency savings covered the rest while I built my business income and identified my next employer.

Another benefit of PBI is that it can be used to build wealth when you don’t need it.

Our family PBI is now almost double what it was in 2017 (now ~$1,500). But since we don’t need it right now, we reinvest that investment income into more income-producing investments, growing our PBI and wealth.

Our PBI isn’t where it is because we’re rich or have big salaries. It’s there because we’ve been building it for a couple of decades.

Who Can Build Personal Basic Income?

Anybody who can save $10 per month can create PBI.

It’s true. Putting $10 in a high yield savings account paying 1% earns you $0.10 of PBI per year.

That’s almost nothing — it’s easy to be discouraged by the math.

But $10 is a starting point.

To build meaningful PBI, you need a lot more than $10 per month and a second critical component — patience (years, decades).

Each month, save a little more. At 1% yield:

- $100 of savings is $1.00 of PBI per year

- $1,000 of savings is $10.00 of PBI per year

- $10,000 of savings is $100 of PBI per year

- $100,000 of savings is $1,000 of PBI per year

- $120,000 of cash savings earning 1% pays $1,200 per year or $100 per month.

Of course, you can earn more than 1% by investing in stocks, real estate, or other assets (and you better these days because inflation is much higher than 1%).

$120,000 earning 6% pays $7,200 per year, or $600 per month.

$120,000 earning 10% pays $12,000 per year, or $1,000 per month.

That’s enough to cover groceries, gas, utilities, and more.

And as you build savings momentum, your active income (salary, job income, etc.) will likely grow. As long as you keep your spending in control, you should be able to put more active income toward growing your PBI.

Those small numbers you started with eventually begin compounding into more significant numbers.

It starts with the habit of saving and investing your excess cash each month. Then be patient.

How to Create a Personal Perpetual Paycheck

OK, so you can save a few bucks a month and are willing to invest for the long haul. So how do you turn cash into a personal paycheck?

Building PBI entails saving excess cash flow from your primary income source, then investing it into income-producing assets. To grow it, reinvest proceeds from previous investments into additional investments.

Here’s a list of assets that work well for building personal basic income in order of simplicity, with links to articles and resources where you can learn more.

High Yield Savings

Bank savings accounts are risk-free and better than checking accounts.

Even though high yield savings accounts aren’t nearly enough to counter today’s inflation, it’s the most accessible place to start earning that 1% on the first $10 of savings.

High yield savings is the minimum. Always keep cash that you aren’t actively spending or investing in a high-yield savings account.

Recommended:

- Raisin

- Compare High-Yield Savings Accounts

Stocks, ETFs, Index Funds

Stocks are my favorite way to invest in creating personal basic income because it’s easy to get started, measure, and grow. Returns outpace cash savings by a lot (if you’re patient).

I’ve invested in dividend-paying stocks since 1995, and they make up the majority of my taxable PBI.

Individual stocks are OK if you have the time and knowledge to research them, but it’s even easier to own stock ETFs, which give you instant diversification.

Most pay a conservative yield and will likely appreciate over long investment horizons.

The Vanguard Total Stock Market Index ETF (VTI) is my favorite. FSKAX (Fidelity) and VTSAX (Vanguard) are mutual funds akin to VTI, which work similarly if you have accounts with those brokers.

There are many other options out there to create income streams with mutual funds and ETFs, with higher yields than total market funds.

I only invest in taxable accounts after I’ve maxed out all tax-advantaged accounts (403(b), IRA, etc.). That’s because Uncle Sam taxes dividend income at 15% for most of us.

You can avoid taxes on dividends by utilizing the Roth IRA or traditional IRAs. But withdrawing from IRAs for PBI can trigger penalties unless you are over age 59 1/2.

Read more:

- Monthly Dividend Stocks

- How to Invest in Dividend Stocks

- Individual Stocks vs. Index Funds

- FSKAX vs. VTSAX

Here’s a list of my favorite brokers for dividend investing. M1 Finance is at the top.

Bonds

Bond yields have stayed low for more than a decade. Young investors often don’t see a point in investing in them.

But as you age and as interest rates increase bond yields, it makes sense to introduce them to your portfolio to diversify and reduce risk.

Income seekers can look to bonds to build PBI.

There are many types of bonds, but most retail investors are interested in three kinds:

- Government Bonds

- Municipal Bonds

- Corporate Bonds

U.S. Government I Bonds track inflation. When inflation is high, I Bonds provide a risk-free return at about the inflation rate.

I’m using I Bonds to boost my PBI for now, and I may hold them until my kids go to college. The interest on I Bonds is deferred until redemption and tax-free if used for education expenses.

Read more: 7 Streams of Income Beyond a Salary

Municipal Bonds are my favorite type of bond because they provide tax-free income in non-retirement accounts (there is no advantage to buying them in retirement accounts). Plus, they are easy to purchase through ETFs.

Muni bonds are low-risk debt securities that help to fund infrastructure projects and operations for local governments and other regional jurisdictions.

I prefer to use ETFs for municipal bonds and own three different funds in my portfolio. Interest on muni bonds is tax-free, so you can collect dividends and pay no taxes, increasing your net return and reducing your overall dividend tax bill.

Read more: Are Municipal Bond ETFs Right for Your Portfolio?

Companies borrow money to invest in real estate, people, and growth opportunities. These debts show up on corporate balance sheets.

Investment banks help companies issue and sell corporate bonds, which often go to institutional investors such as pension funds, mutual funds, hedge funds, and wealthy individual investors.

Retail investors can own this debt as well. You can buy individual bonds, but it’s time-consuming and overwhelming.

Lower risk bonds pay lower interest rates and probably won’t default. Higher-risk bonds pay higher rates, but there’s greater default risk.

You can always lose money.

The better option is to buy corporate debt via ETFs. The four biggest funds are VCIT, VCSH, LQD, and IGSB, which vary in duration and investment grade.

Unfortunately, corporate bond interest is not “qualified”, so income is taxed as ordinary income (normal income tax rates instead of the more favorable dividend tax rate that stocks get).

Only invest in corporate debt through retirement accounts. Corporate bonds are a suboptimal option if you’re under 59 1/2 and aiming to build PBI. Go with I Bonds or muni bonds instead.

Crowdfunded Real Estate

If you don’t want to own and manage rental properties, crowdfunded real estate is a simple yet powerful way to own commercial and residential real estate.

Crowdfunding utilizes technology and loosened securities laws to empower investors to pool money to buy high-quality real estate through third-party platforms.

These real estate crowdfunding platforms facilitate purchasing and managing larger properties that would otherwise be uninventable for ordinary investors.

They create a legal structure to protect all stakeholders and take a small fee for the trouble.

Depending on your risk tolerance, you can invest in individual deals (for higher returns) or buy diverse pools of properties (via REITs) to lower risk and enjoy passive PBI. There are also different investment structures, such as debt vs. equity, and various types of properties.

I’ve invested via a handful of crowdfunding platforms over the past five years.

Fundrise is the easiest to get started and diversify. Non-accredited investors can invest with as little as $10 to build personal basic income. My $25,000 portfolio holds small stakes in about 130 properties.

EquityMultiple is the platform where I’ve made my recent investment in a multi-use retail and apartment building — $20,000 in just one riskier (albeit more heavily-vetted) endeavor.

Here’s a detailed guide to consider before selecting a crowdfunding investment platform.

Read more:

Please note: This is a testimonial in partnership with Fundrise. We earn a commission from partner links on RetireBeforeDad.com. All opinions are my own.

Real Estate Rentals

Real estate is arguably the best way to build significant PBI quickly if you can find bargains. Rental properties provide cash flow, appreciation, and tax benefits.

If you can acquire properties at a discount or put enough money down, you can collect enough rent to cover expenses, save for a rainy day, and produce monthly positive cash flow.

Real estate investing doesn’t come easy. Own the wrong property at the wrong time, and it can become a money pit.

Or sign the wrong tenant, and you’ve got headaches galore.

You can avoid the headaches of real estate investing by hiring a property manager (if you can afford it). That requires more money down and reduced cash flow.

But it may be worth the peace of mind.

If you hold onto the right property long enough, it will pay off handsomely.

I owned a rental property for about eight years but sold it (long story). Part of me wishes I still had it to help support my early retirement.

But I moved that equity elsewhere for better yields and more restful sleep.

Read more:

- FIRE with Real Estate

- How I Quit my Career with Out-of-State Rentals

- Roofstock Review

- Investing in Multi-family Rentals

- How to Retire Early with Real Estate

Alternative Assets

In the last decade, it has become easier to invest in alternative assets thanks to crowdfunding legislation passed in 2012.

I’ve highlighted several options for investing in alternatives over the years.

Some of the more interesting include websites, farmland, and diversified alternatives. Not all provide consistent dividends, so perform due diligence to meet your investment objectives.

Farmland investing, for example, usually pays just once a year — other investments pay quarterly or monthly.

Read more:

- How to Invest in Websites

- 13 Proven Ways to Monetize Your Hobbies

- AcreTrader Review — Farmland Investing for Income and Growth

- 8 Alternative Investment Ideas for Asset Diversification

Conclusion

Universal basic income could become more widespread over the coming decades. But don’t hold your breath.

Take matters into your hands and start building personal basic income. Anyone who can spare $10 per month and is willing to invest it for the future can start.

You’ll need to increase that amount and make saving and investing a habit rather than an every-so-often activity. Utilize tax-advantaged accounts first.

Please don’t spend your PBI if you don’t have to — reinvest it for the future!

Eventually, as your active income grows and your savings capabilities increase, you’ll start accumulating assets that pay you significant benefits, helping to provide job-free stability in your life and the freedom to fail.

Use your patiently found freedom to pursue a passion, start a business, or seek adventure while your money works for you.

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

- Dividend Kings — 50+ stocks that have increased dividends for 50+ years.

- Monthly Dividend Stocks — List of 70+ stocks that pay a dividend every month.

- Dividend Champions — 140+ stocks that have increased dividends for 25+ years.