11 Financial Goals to Set Any Time of the Year

Are you thinking about what financial goals to set this year?

According to a motivational flyer in my office, 71% of Americans make resolutions, but only 8% succeed.

Put me in that 8%.

This year, I’d like to lose about 15 pounds. I also ate a lot of chocolate last week.

With setting financial goals, I do much better.

Most worthwhile financial goals take more than a year to achieve. Declaring a financial goal as a New Years’ resolution is great, but don’t limit yourself to goal setting once a year. Think about making progress with money every day.

I participated in an Experian Twitter chat late last year. One of the questions they asked was, what are your financial goals for 2020?

My financial goals are mostly the same every year. 1) Max out all retirement accounts, 2) grow my side business income (this blog), 3) increase my passive income, and 4) simplify my finances.

These aren’t exactly S.M.A.R.T. goals because I don’t associate specific numbers to my financial goals anymore.

My near-term goals are more like guideposts on the way towards my ultimate goal. They keep me on the hiking trail, but the distance between each trail marker varies.

You have to be careful with financial goals because you can’t control important variables, such as market returns. For example, if you set a financial goal to increase your net worth by XX% and you own stocks, the market will determine your success, not you.

This article focuses on financial goals all within your control.

I’ll start with my four main goals and why I’ve chosen them. Then give seven other examples of financial goals to set and ideas that may fit your situation.

Even if you fail at New Year’s resolutions, you can set these financial goals on any timeline, year-round.

Table of Contents

1. Max Out All Tax-Advantaged Accounts

Maxing out retirement accounts may not have much impact year-to-year, but it packs a punch over the long-term.

Tax-advantaged accounts have the dual benefit of reducing taxes and growing your wealth tax-deferred or tax-free. It’s hard to find a better deal from the government.

For the 2019 tax year, we plan to max out:

- My employer 403(b) and 401(a) + received a 10% match

- Mrs. RBD’s spousal IRA

- Our three kids’ state 529 plans

- My eligible SEP-IRA contributions, and hopefully…

- My Roth IRA (though it’s starting to look like the capital gains from the condo sale will prohibit a contribution)

We’ve maxed out almost all of these items for the past few years. But it’s kind of crazy, the more money I make from my business, the more we can reduce our taxable income.

Last year, we received a qualified business income deduction for the first time. This year we plan to utilize a SEP IRA to reduce our taxes even more.

I’ve always known about the SEP-IRA, but I figured my side business income wasn’t large enough for the hassle. However, I had a CPA help with the taxation of the condo sale, and she insisted on opening one.

The SEP-IRA will significantly reduce our tax burden from the condo sale while further building our retirement accounts.

Set a financial goal to max out at least one of your retirement accounts this year. Next year, add another.

Read more: Should You Max Out Your 401(k) in 2020?

2. Earn a Free Flight (or Three)

I’ve loved travel since my high school Latin class trip to Italy in 1993.

But today, I’m the sole earner for our family of five, and my in-laws live across the country. Buying five airline tickets to fly anywhere is too expensive without using travel miles to defray the cost.

In 2017, our entire family flew from D.C. to San Francisco, costing us almost no cash. We paid using 125,000 United MileagePlus points.

This summer, my wife and kids went back to California again, for free.

That’s nine round-trip flights within two years, and we still have 100,000 points saved for our next vacation.

Acquiring airline miles and flexible travel rewards is the key.

We acquired our rewards by earning both welcome bonuses and rewards through everyday spending.

When you sign up for a new card, credit card companies offer bonuses if you spend a certain amount over the following three months. Then every dollar you spend, you get more travel rewards and sometimes extra points on travel and restaurants.

All the free travel we’ve earned came from just three credit cards, spending no more than our typical monthly budget. They are:

- Chase Sapphire Preferred with My Chase Plan option

- Chase United Explorer Card, and

- Chase Ink Business Preferred.

3. Grow Active Income as a Financial Goal

We all want to earn more money. But have you set a goal to earn more?

I work hard at my corporate job. The harder I work, the more I get paid.

But not dramatically. Salaried work will get you an annual raise and maybe a bonus here or there, but it won’t make you wealthy without years of diligent saving and investing.

I received a modest raise from my company this year, above the company average by about 1%. Plus, I earned a small bonus right around the holidays for a project that went well. So I can’t complain too much.

But most jobs don’t deliver the kind of income growth that entrepreneurship can.

That’s why I focus my active income goal more on side business income, the money I earn from this blog. My website is a low-to-mid-tier personal finance blog in terms of traffic and popularity. I’ve learned to make a decent income after six years of publishing content.

Every year, I try to earn more by writing more articles and increasing my presence on the internet, which ultimately increases my income.

Most aspects of my business success are under my control. The harder I work and the better stuff I write, the more I earn, though some things are out of my control (e.g., Google’s Algorithms).

Focus your efforts wherever you can earn the most. Follow the path of least resistance. If your career starts to plateau, it might be time to go off on your own or start something on the side.

Maybe you’ve set a goal to finally start a business or blog of your own this year. Here are some tips to get started.

4. Grow Passive Income

Passive income is money earned from investments instead of hours worked. I’ve spent a lot of time over the years researching and tracking investments and the future income they produce.

That’s because I want to fund my lifestyle with investment income so I can retire early without relying solely on investment withdrawals.

This strategy reduces the risk of running out of money in retirement and makes it more likely I can pay for long-term aging-related costs and leave a financial legacy to my family.

Of all the passive income ideas I’ve investigated over the past decade, my two favorites continue to be real estate crowdfunding and dividend stocks.

Both investments require small amounts of capital to get started ($500 or less), and I believe that starting small is far better than not starting at all. Plus, both assets appreciate, produce income, are easy to diversify (residential, commercial, farmland, etc.), and scale with your wealth.

With the onset of real estate crowdfunding and the ability to buy turnkey real estate for traditional real estate investing, it’s easier to begin investing in real estate now more than ever.

What’s best about passive income investing is that your income doesn’t fluctuate like the stock market. Dividends and real estate cash flow are relatively predictable and usually increase over time. The one downside is taxation, which you can avoid by utilizing retirement accounts.

Read more: 20+ Passive Income Ideas

5. Simplify Your Finances

I made a substantial push to simplify my finances in 2019 in alignment with our efforts to complete an estate plan. Creating an estate plan makes you think about what’s most important.

It also entails reviewing financial accounts and the consequences if one partner dies.

Having too many accounts can make the execution of an estate more time-consuming and difficult. I don’t want to leave a mess behind for my wife, so I closed several redundant savings, credit cards, and brokerage accounts.

To me, it wasn’t a mess. I’m very much in tune with our financial stuff. But it would have been unnecessarily stressful for Mrs. RBD.

Estate planning isn’t the only reason to simplify. Reducing financial complexity decreases the amount of time you need to spend managing your money, leaving more time for leisure.

I’ve been tracking our passive investment income monthly since 2003. This year, I’ll only run the numbers every quarter. The process takes up too much of my time.

6. Finish your Estate Plan

According to a survey on my website, 41% of readers that have kids do not have an estate plan.

Very soon would be a great time to get this done.

Start by securing a life insurance policy if you don’t have one already. We bought two policies shortly after marriage and had to go through all the health checks. I also have a policy through my employer.

It’s easier now to get life insurance quotes online on various websites.

Once the life insurance policy is in place, pair your estate planning with #4 above. Start simplifying your financial life immediately.

Soon after, ask friends for referrals to find a local attorney that can step you through all the essential documents. Find someone with the patience to explain all the details. Shop around to make sure the price is right.

We finished our estate plan through an employer benefit for cheap. But before that, an attorney quoted us $1,250 for Wills, Durable Power of Attorney, a Living Trust, and Advance Medical Directive, which seemed like a reasonable price in our area.

Read more: Estate Plan or Vasectomy — What’s Worse?

7. Pay off Debt Financial Goals

I’ve set multiple debt payoff goals over the years. But none of them were time-bound. Each time the target date was as soon as possible.

A discovery I made in pursuing debt payoff goals was that I’d always finish paying off the debt faster than I planned.

That’s because I was willing to draw down money in high-interest savings accounts to pay it off sooner. That left my emergency savings a bit thin. But paid off debts feel great.

If you have high-interest consumer debt, or if a particular payment is suffocating your monthly cash flow, you must eliminate the debt. The sacrifice is worth it.

I believe you won’t even begin to achieve financial success and freedom until all of your credit card, personal loans, and car debt is history.

The mortgage can wait, but I won’t stop you if you set a financial goal to pay it off or lower your mortgage payment.

Paying off debt is a rewarding endeavor. Once it’s gone, you have more cash flow at the end of each month.

Use excess cash flow to pay off other debts (snowball) or to create additional income streams.

One thing I love about debt is that paying it off is a measurable risk-free return. Most debts have a fixed interest rate. So if you put $500 toward a credit card debt on which you pay 15%, you’ll save on interest the same amount you would earn if you made 15% on a stock in one year.

For those with oppressive debt, setting a payoff goal may have the highest return on your money. Plus, you gain momentum to tackle the next goal.

8. Save an Emergency Fund

The famous next “baby step” after paying off debt is to fund an emergency fund with three-to-six months of expenses.

I lost my full-time job in October 2017 with about $19,000 of cash in our savings account. Our savings, combined with income from my side business, and lowering our expenses, carried our family through four months of unemployment.

I never received unemployment benefits.

Looking back on the experience, I don’t think that $19,000 was a big enough emergency fund. It was plenty big for that jobless period. But the economy was strong, my side income was growing, and I still had investments I could have fallen back on.

However, during the 2008-2009 recession, unemployment periods lasted a lot longer, and stock prices crumbled.

You may feel immune to the next recession, but there’s nothing wrong with cash in the bank to safeguard your financial security. Set aside enough cash savings to cover your living expenses, and don’t be afraid to go beyond that.

If not an emergency fund, think of cash in the bank as your opportunity fund, and be ready to pounce on investments if prices fall out of whack.

9. Spend Less than the Same Month Last Year

I track our family expenses in a simple spreadsheet using pivot tables. Once set up, it’s easy to know how much you spend each month.

Here’s one goal that you can set year-round.

At the start of each new month, take note of last year’s spending and create a budget to spend less. If you can beat each month by just a little bit, you will spend less for the entire year.

Spending got a bit out of hand for our family this year. We took an unforgettable vacation, but I’d rather forget how much it cost. Our kids also aged into some more expensive extracurricular activities.

The higher annual spending has hurt our progress toward financial independence calculation, but it allows us to improve this year, every month. So this is a goal I’m going to work on throughout 2020.

10. Diversify your Investments

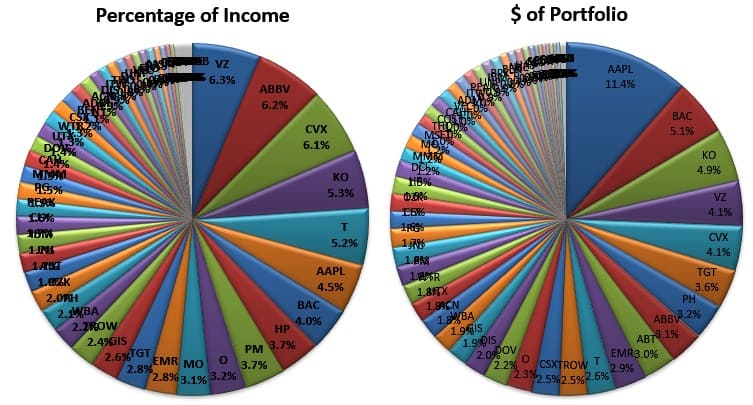

A few years back, when I was aggressively building my taxable dividend portfolio, I noticed that about 38% of my dividend income came from just four stocks of 33 in my portfolio.

The top four stocks made up 34% of my portfolio’s total dollar value.

This happened because I had owned a few stocks for two decades. Plus, my Apple stock appreciated considerably, taking up a large percentage of my portfolio.

My unbalanced portfolio increased my investment risk, so I set a goal to reduce my income reliance on those four stocks and to decrease Apple’s share of my total assets.

To achieve this goal without selling Apple or my top dividend stocks, I had to buy new stocks and more shares of stocks I already owned.

No problem, so I thought. But the large holdings continued to appreciate and increase dividends.

Since discovering the significant portfolio imbalance, I’ve maintained pie charts showing the largest holdings and dividend payers in my portfolio.

The first is my stock holdings by the percentage of dividend income. The second is the percent of total dollar value each stock makes up in my taxable dividend stock portfolio.

Today, the top four dividend-paying stocks pay me about 24% of my total income.

The four largest holdings now make up 25% of my portfolio, in large part due to Apple’s continued appreciation over the years. Apple is now 11% of my portfolio. No other holding is more than 5.1%. These pies do not include my retirement accounts.

So I’ve made significant improvements, but I’ve still got work to do. This goal has become part of my everyday portfolio planning, but it’s challenging to set actual levels of achievement due to an always unpredictable market.

11. Buy X Number of Rental Properties

I’ve heard of several real estate investors who set goals to buy X number of rental properties in one year, or a novice trying to invest in their first rental.

Getting good at buying rental properties takes knowledge and experience. Read books, study the properties and tactics of other successful investors, and ask experienced investors for advice.

I don’t miss my old rental property. However, I do miss the extra income stream. The cash from the sale of my rental is now sitting in a bank account earning interest. Having so much cash on hand feels like I’m missing out on stock market returns.

But I’m also positioned for an opportunity. Though I haven’t set a goal to purchase a rental property, another rental property is not out of the question. If a recession were to drop prices and bargains emerge, I’d look for deals.

The next time around, I’ll know what I’m doing. I may consider buying a turnkey property from a online platform such as Roofstock.

What kinds of financial goals are you considering this year? Do you set goals every year? Are you part of the 8% of people that succeed?

Photo via DepositPhotos used under license.

* The compliance department of RBD’s affiliate partner, Bestow, would like you to know the following: the opinions and ideas expressed in the article are those of the author(s) and are not promoted or endorsed by Bestow or North American.

Craig is a former IT professional who left his 19-year career to be a full-time finance writer. A DIY investor since 1995, he started Retire Before Dad in 2013 as a creative outlet to share his investment portfolios. Craig studied Finance at Michigan State University and lives in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

- Dividend Kings — 50+ stocks that have increased dividends for 50+ years.

- Monthly Dividend Stocks — List of 70+ stocks that pay a dividend every month.

- Dividend Champions — 140+ stocks that have increased dividends for 25+ years.